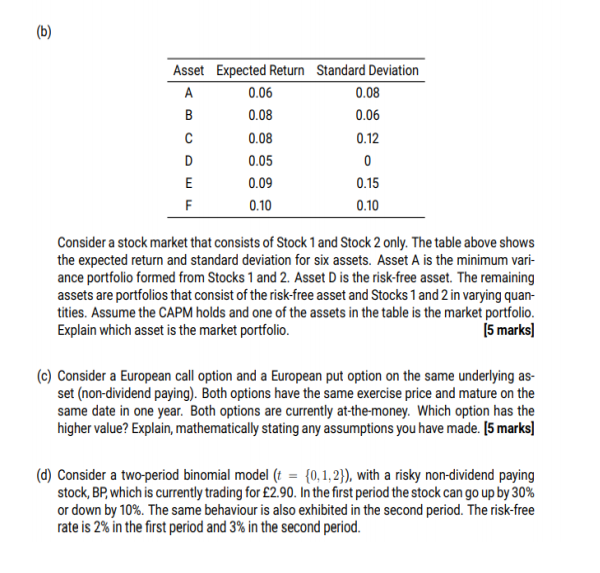

Question: (b) Asset Expected Return Standard Deviation A 0.06 0.08 B 0.08 0.06 0.08 0.12 D 0.05 0 E 0.09 0.15 F 0.10 0.10 Consider a

(b) Asset Expected Return Standard Deviation A 0.06 0.08 B 0.08 0.06 0.08 0.12 D 0.05 0 E 0.09 0.15 F 0.10 0.10 Consider a stock market that consists of Stock 1 and Stock 2 only. The table above shows the expected return and standard deviation for six assets. Asset A is the minimum vari- ance portfolio formed from Stocks 1 and 2. Asset D is the risk-free asset. The remaining assets are portfolios that consist of the risk-free asset and Stocks 1 and 2 in varying quan- tities. Assume the CAPM holds and one of the assets in the table is the market portfolio Explain which asset is the market portfolio. 15 marks] (c) Consider a European call option and a European put option on the same underlying as- set (non-dividend paying). Both options have the same exercise price and mature on the same date in one year. Both options are currently at-the-money. Which option has the higher value? Explain, mathematically stating any assumptions you have made. [5 marks] (d) Consider a two-period binomial model (t = {0,1,2}), with a risky non-dividend paying stock, BP, which is currently trading for 2.90. In the first period the stock can go up by 30% or down by 10%. The same behaviour is also exhibited in the second period. The risk-free rate is 2% in the first period and 3% in the second period

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts