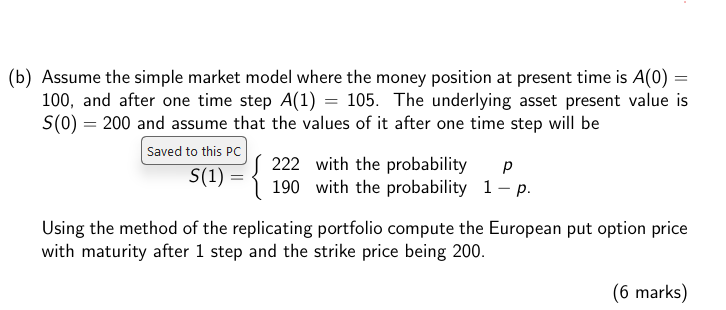

Question: ( b ) Assume the simple market model where the money position a t present time i s A ( 0 ) = 1 0

Assume the simple market model where the money position present time

and after one time step The underlying asset present value

and assume that the values after one time step will

Saved this With the probability

Using the method the replicating portfolio compute the European put option price

with maturity after step and the strike price being

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock