Question: b. based on the given information in the previous question, assume that you have OMR10,000 available to invest. if you sell short OMR6,000 of security

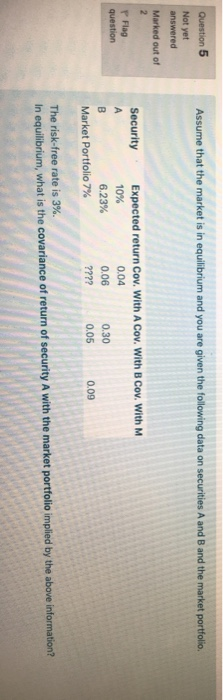

Question 5 Assume that the market is in equilibrium and you are given the following data on securities A and B and the market portfolio Not yet answered Marked out of P Flag question Security Expected return Cov. With A Cov. With B Cov. With M A 10% 0.04 B 6.23% 0.06 0.30 Market Portfolio 7% ???? 0.05 0.09 The risk-free rate is 3%. In equilibrium, what is the covariance of return of security A with the market portfolio implied by the above information? Question 5 Assume that the market is in equilibrium and you are given the following data on securities A and B and the market portfolio Not yet answered Marked out of P Flag question Security Expected return Cov. With A Cov. With B Cov. With M A 10% 0.04 B 6.23% 0.06 0.30 Market Portfolio 7% ???? 0.05 0.09 The risk-free rate is 3%. In equilibrium, what is the covariance of return of security A with the market portfolio implied by the above information

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts