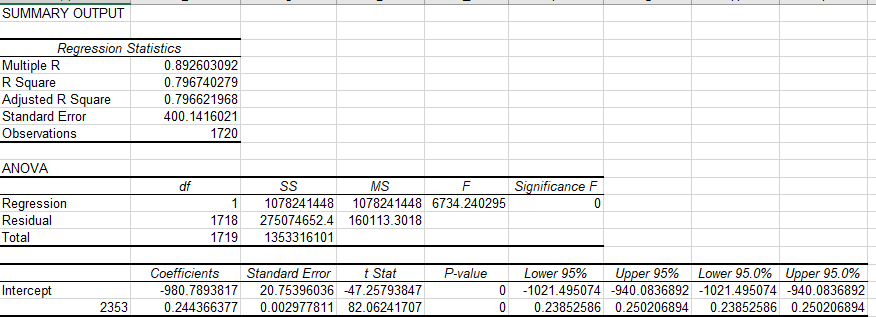

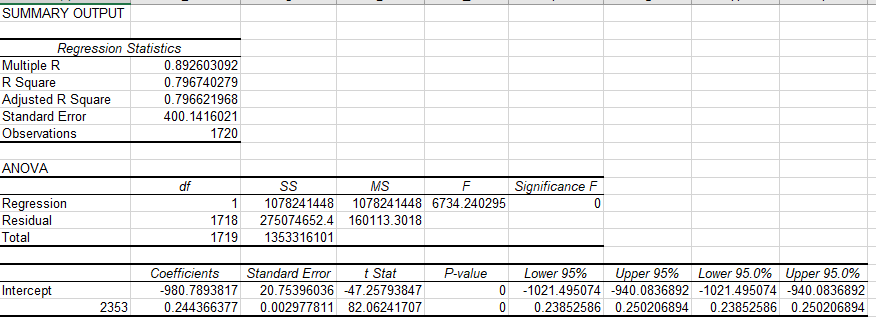

Question: b. Consider (1) the regression equation M = B0 + B1 R; if we focus on the change in reserves thus ignoring the constant term,

b. Consider (1) the regression equation M = B0 + B1 R; if we focus on the change in reserves thus ignoring the constant term, then what is left is M = B1 R. Consider also (2) the equation that we learned in our lesson on multiple deposit expansion: D = R/rrr. Consider finally that deposits and money are the same thing, D=M. Use the regression results from part (a) and these equations to quantify the rrr . Interpret your result.

c. Tell whether ?1 is statistically significant. Explain your answer and show your work.

d. Tell what percentage of the variation in the money supply is accounted for by the variation in bank reserves.

SUMMARY OUTPUT Regression Statistics Multiple R 0.892603092 R Square 0.796740279 Adjusted R Square 0.796621968 Standard Error 400.1416021 Observations 1720 ANOVA df SS MS F Significance F Regression 1 1078241448 1078241448 6734.240295 0 Residual 1718 275074652.4 160113.3018 Total 1719 1353316101 Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0% Intercept 980.7893817 20.75396036 -47.25793847 -1021.495074 -940.0836892 -1021.495074 -940.0836892 2353 0.244366377 0.002977811 82.06241707 0 0.23852586 0.250206894 0.23852586 0.250206894

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts