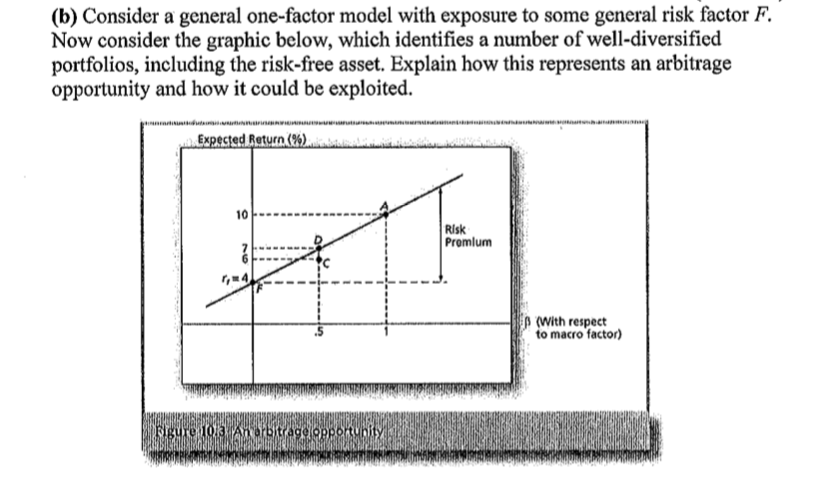

Question: (b) Consider a general one-factor model with exposure to some general risk factor F. Now consider the graphic below, which identifies a number of well-diversified

(b) Consider a general one-factor model with exposure to some general risk factor F. Now consider the graphic below, which identifies a number of well-diversified portfolios, including the risk-free asset. Explain how this represents an arbitrage opportunity and how it could be exploited. Expected. Return (%) 10 Risk Promlum In (with respect to macro factor) gurean arbitrag erportunity

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock