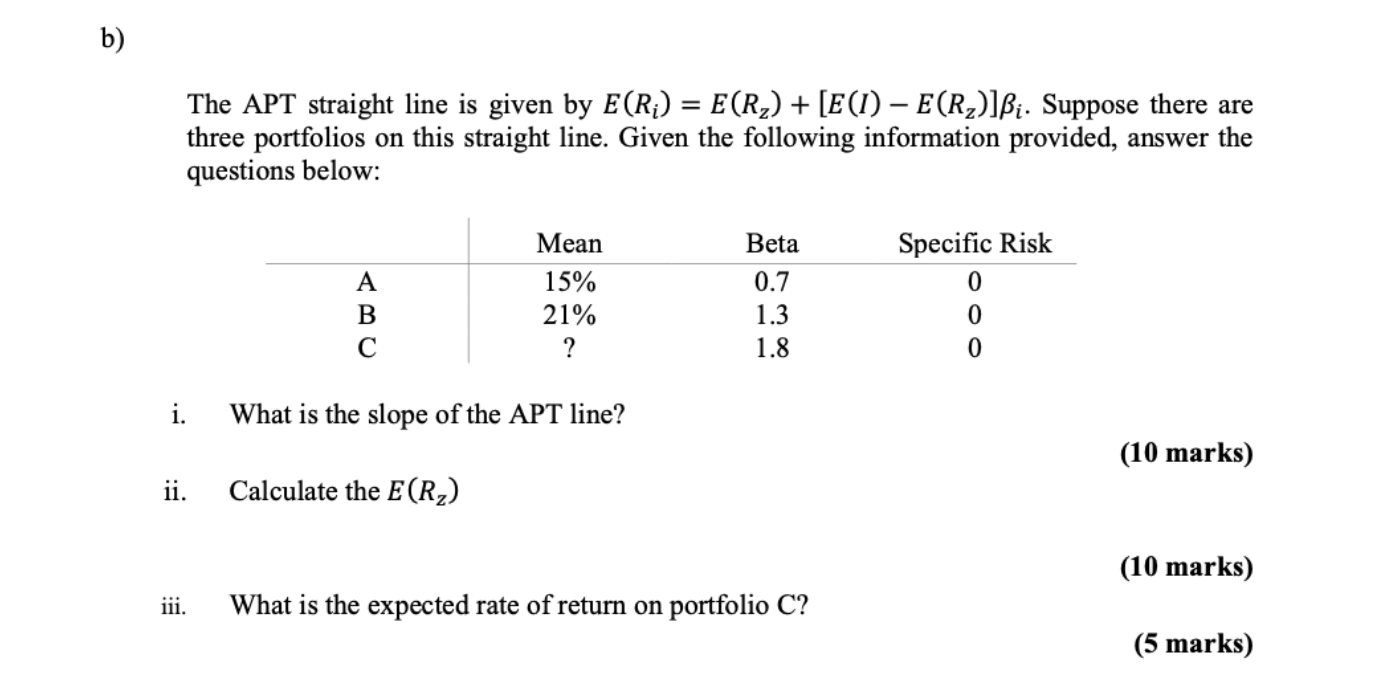

Question: b) The APT straight line is given by E(R;) = E(R) + [E (1) E (R)]. Suppose there are three portfolios on this straight line.

b) The APT straight line is given by E(R;) = E(R) + [E (1) E (R)]. Suppose there are three portfolios on this straight line. Given the following information provided, answer the questions below: Mean Beta Specific Risk A 15% 0.7 0 B 21% 1.3 0 C ? 1.8 0 i. What is the slope of the APT line? (10 marks) ii. Calculate the E (R) (10 marks) iii. What is the expected rate of return on portfolio C

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock