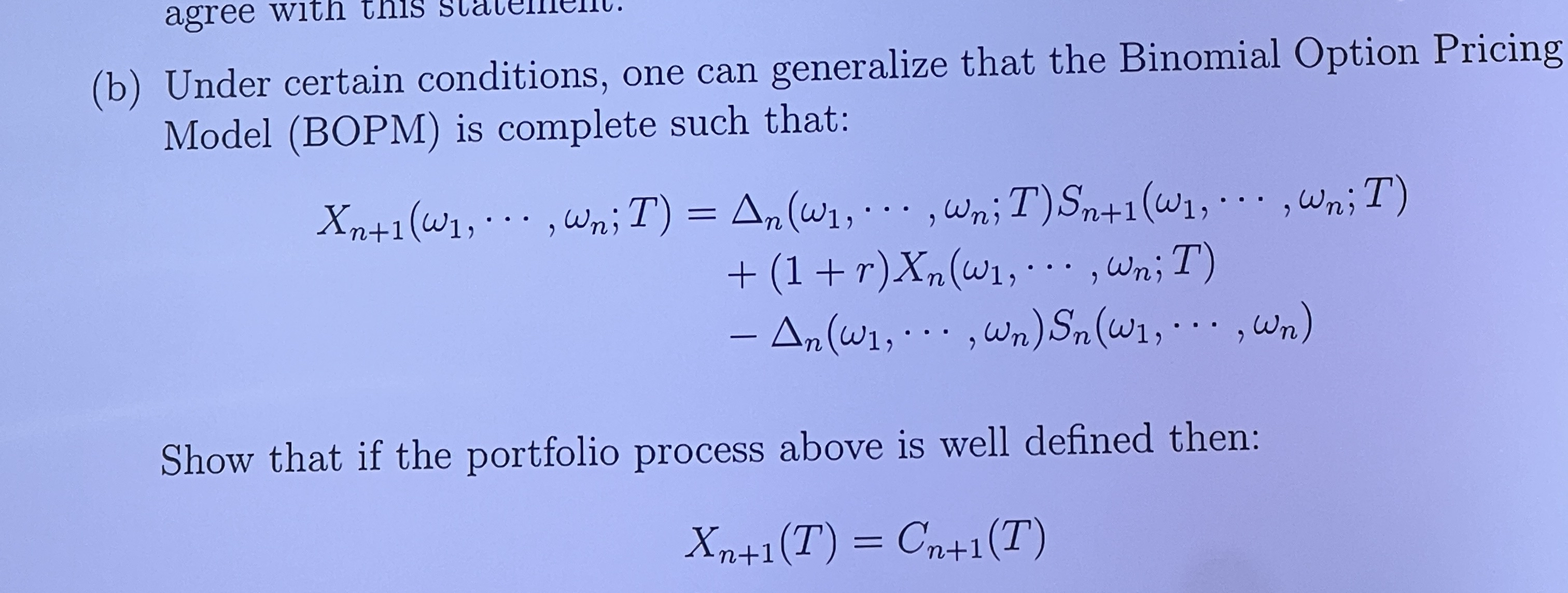

Question: b ) Under certain conditions, one can generalize that the Binomial Option Pricing Model ( BOPM ) is complete such that: x n + 1

b Under certain conditions, one can generalize that the Binomial Option Pricing

Model BOPM is complete such that:

cdots,;cdots,;cdots,;

cdots,;

cdots,cdots,

Show that if the portfolio process above is well defined then:

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock