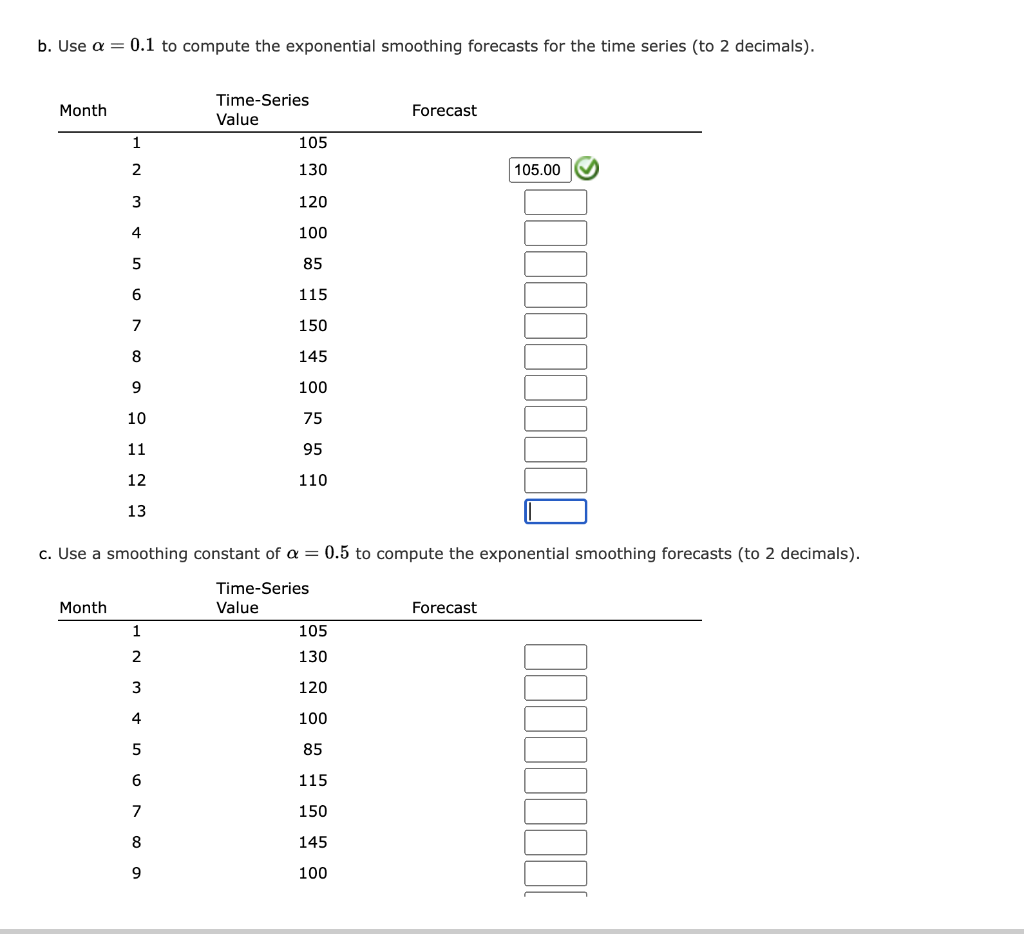

Question: b. Use a = 0.1 to compute the exponential smoothing forecasts for the time series (to 2 decimals). Month Forecast Time-Series Value 105 1 2

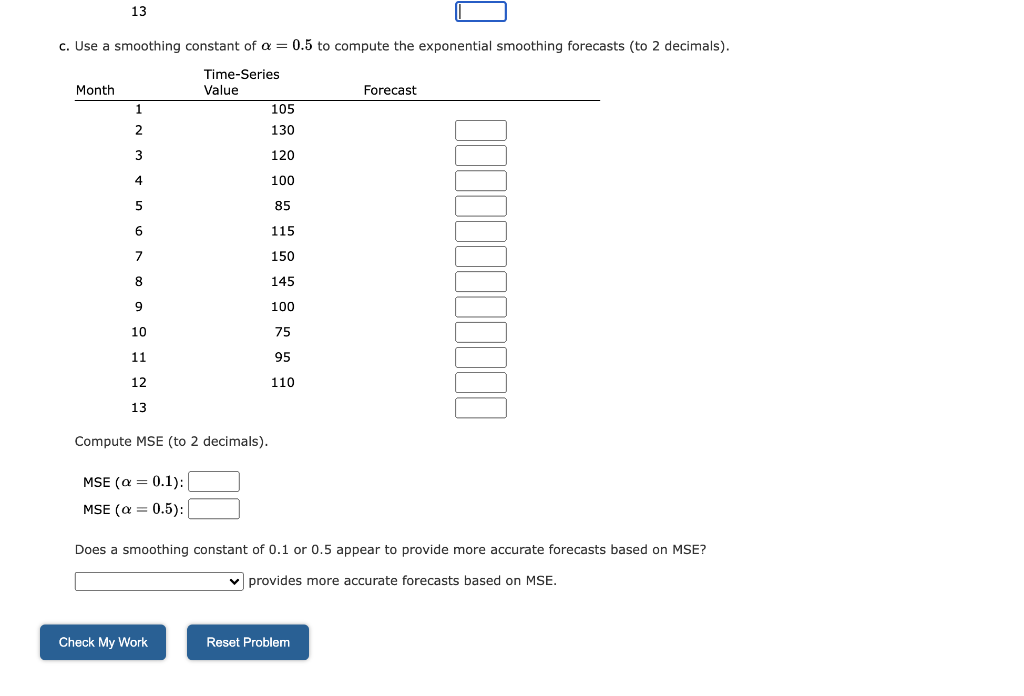

b. Use a = 0.1 to compute the exponential smoothing forecasts for the time series (to 2 decimals). Month Forecast Time-Series Value 105 1 2 130 105.00 3 120 4 100 5 85 6 115 7 150 8 145 9 100 10 75 11 95 12 110 13 c. Use a smoothing constant of a = 0.5 to compute the exponential smoothing forecasts (to 2 decimals). Month Time-Series Value 105 Forecast 1 2 130 3 120 4 100 5 85 6 115 7 150 8 145 9 100 13 D c. Use a smoothing constant of a = 0.5 to compute the exponential smoothing forecasts (to 2 decimals). Month Time-Series Value 105 Forecast 1 2 130 3 120 4 100 5 85 6 115 7 150 8 145 9 100 10 75 11 95 12 110 13 Compute MSE (to 2 decimals). MSE (a=0.1): MSE (a = 0.5): Does a smoothing constant of 0.1 or 0.5 appear to provide more accurate forecasts based on MSE? provides more accurate forecasts based on MSE. Check My Work Reset

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts