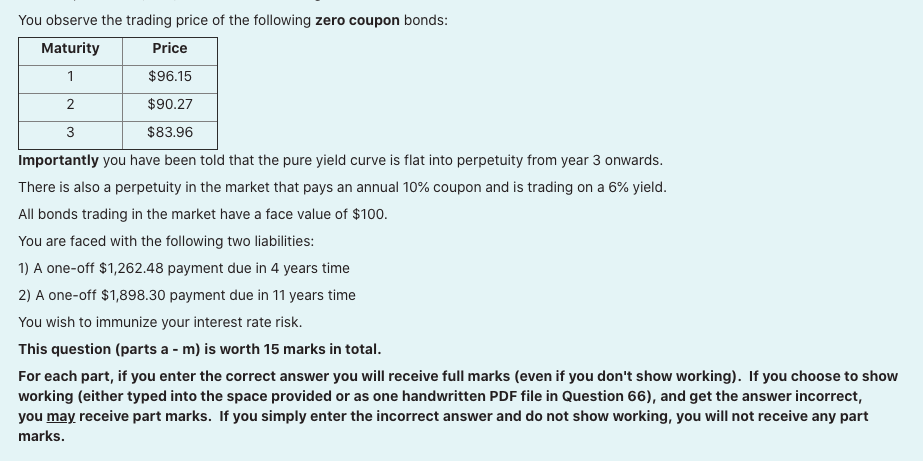

Question: b) What is the 2-year spot rate? (0.5 marks) Enter your answer to 4 decimal places eg if your answer is 6.54% enter as 0.0654.You

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock