Question: B2. (15 marks) (a) Crisis-free Bank started its first day of operations with $200 million in capital. It received a total of $200 million in

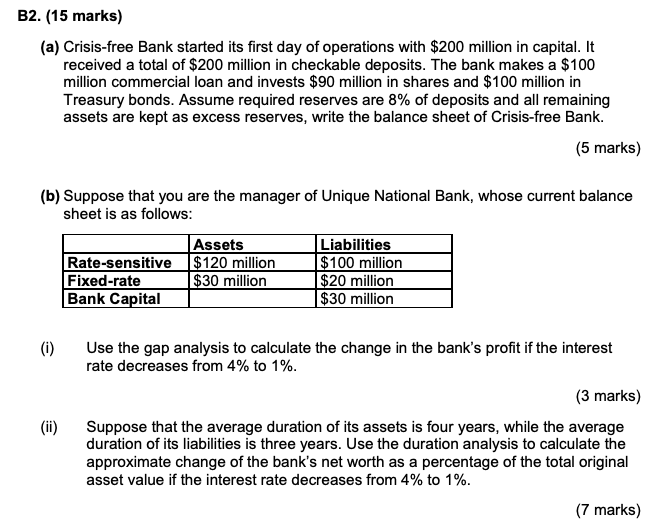

B2. (15 marks) (a) Crisis-free Bank started its first day of operations with $200 million in capital. It received a total of $200 million in checkable deposits. The bank makes a $100 million commercial loan and invests $90 million in shares and $100 million in Treasury bonds. Assume required reserves are 8% of deposits and all remaining assets are kept as excess reserves, write the balance sheet of Crisis-free Bank. (5 marks) (b) Suppose that you are the manager of Unique National Bank, whose current balance sheet is as follows: Rate-sensitive Fixed-rate Bank Capital Assets $120 million $30 million Liabilities $100 million $20 million $30 million (1) (ii) Use the gap analysis to calculate the change in the bank's profit if the interest rate decreases from 4% to 1%. (3 marks) Suppose that the average duration of its assets is four years, while the average duration of its liabilities is three years. Use the duration analysis to calculate the approximate change of the bank's net worth as a percentage of the total original asset value if the interest rate decreases from 4% to 1%. (7 marks) B2. (15 marks) (a) Crisis-free Bank started its first day of operations with $200 million in capital. It received a total of $200 million in checkable deposits. The bank makes a $100 million commercial loan and invests $90 million in shares and $100 million in Treasury bonds. Assume required reserves are 8% of deposits and all remaining assets are kept as excess reserves, write the balance sheet of Crisis-free Bank. (5 marks) (b) Suppose that you are the manager of Unique National Bank, whose current balance sheet is as follows: Rate-sensitive Fixed-rate Bank Capital Assets $120 million $30 million Liabilities $100 million $20 million $30 million (1) (ii) Use the gap analysis to calculate the change in the bank's profit if the interest rate decreases from 4% to 1%. (3 marks) Suppose that the average duration of its assets is four years, while the average duration of its liabilities is three years. Use the duration analysis to calculate the approximate change of the bank's net worth as a percentage of the total original asset value if the interest rate decreases from 4% to 1%. (7 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts