Question: B4. Consider the following table, which gives a security analyst's expected return on two stocks for two particular market returns, assuming the T-bill rate is

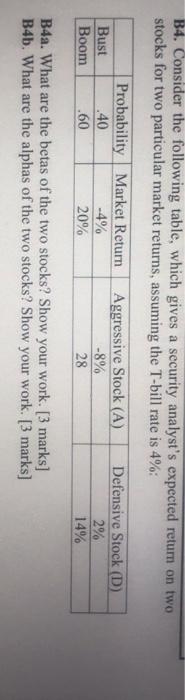

B4. Consider the following table, which gives a security analyst's expected return on two stocks for two particular market returns, assuming the T-bill rate is 4%: Bust Boom Probability Market Return .40 -4% .60 20% Aggressive Stock (A) -8% 28 Defensive Stock (D) 2% 14% B4a. What are the betas of the two stocks? Show your work. [3 marks] B4b. What are the alphas of the two stocks? Show your work. [3 marks]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock