Question: Back CIN4205 Tutorial Work... 1. Compary XYZ shares are currently priced in June at 250c a share. You believe that they are curreatly overvalued and

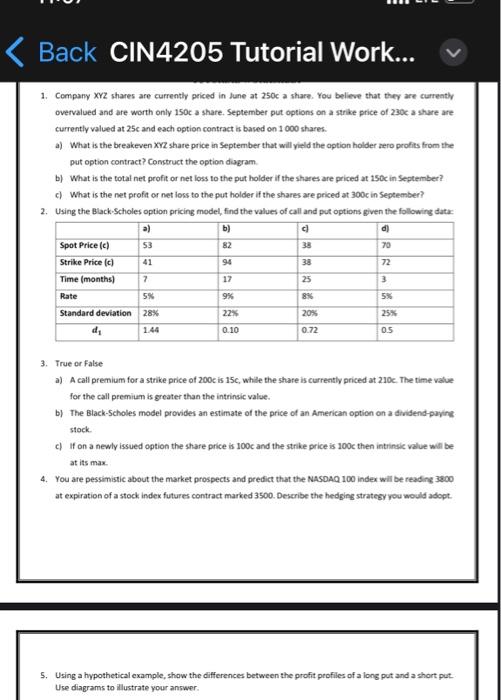

Back CIN4205 Tutorial Work... 1. Compary XYZ shares are currently priced in June at 250c a share. You believe that they are curreatly overvalued and are worth only 150c a share. September put options on a strike price of 230a a share are currently valued at 25c and each option contract is based on 1000 shares. a) What is the breakeven xYZ share price in September that will yield the option holder sero profits from the put option contract? Construct the option diagram. b) What is the total net profit or net loss to the put holder if the shares are priced at 150c in September? c) What is the net profit or net loss to the put holder if the shares are priced at 300c in September? 2. Using the Black-Scholes option pricing model, find the values of call and put options given the following data: 3. True or False a) A call premium for a strike price of 200c is 15c, while the share is currently priced at 210c. The time value for the call premium is greater than the intrinsic value. b) The Black-Scholes model provides an estimate of the price of an American option on a dividend-puyint stock. c) If on a newly issued option the share price is 100c and the strike price is 100c then intrinsic value will be at its max. 4. You are pessimistic about the market prospects and predict that the NASOAQ 100 index will be reading 3800 at expiration of a stock index futures contract marked 3500 . Describe the hedging strategy you would adopt. 5. Using a hypothetical example, show the differences between the profit peofiles of a long put and a short put. Use diagrams to illustrate your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts