Question: Backaround facts: Patrick Pty Ltd (Patrick) is a property developer who purchased a 100-hectare block of land in the western suburbs of Melbourne for $100m

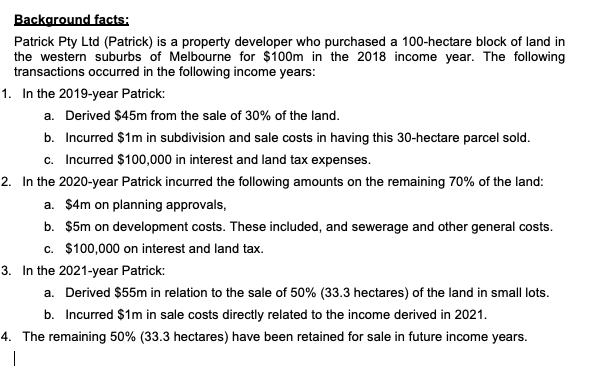

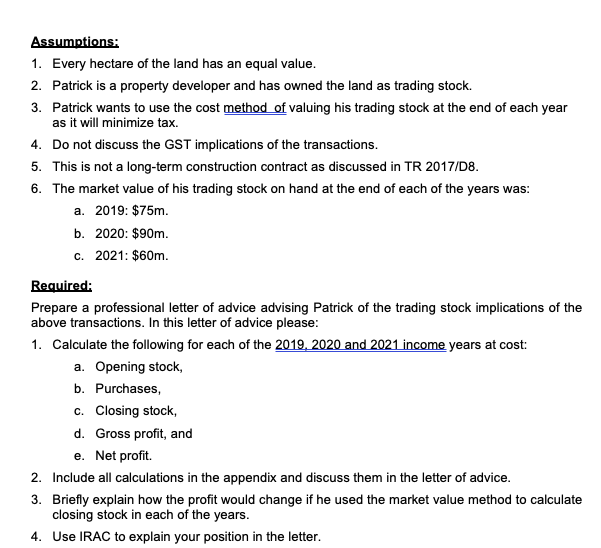

Backaround facts: Patrick Pty Ltd (Patrick) is a property developer who purchased a 100-hectare block of land in the western suburbs of Melbourne for $100m in the 2018 income year. The following transactions occurred in the following income years: 1. In the 2019-year Patrick: a. Derived $45m from the sale of 30% of the land. b. Incurred $1m in subdivision and sale costs in having this 30 -hectare parcel sold. c. Incurred $100,000 in interest and land tax expenses. 2. In the 2020-year Patrick incurred the following amounts on the remaining 70% of the land: a. $4m on planning approvals, b. $5m on development costs. These included, and sewerage and other general costs. c. $100,000 on interest and land tax. 3. In the 2021-year Patrick: a. Derived $55m in relation to the sale of 50% (33.3 hectares) of the land in small lots. b. Incurred $1m in sale costs directly related to the income derived in 2021. 4. The remaining 50% ( 33.3 hectares) have been retained for sale in future income years. 6. The market value of his trading stock on hand at the end of each of the years was: a. 2019: $75m. b. 2020:$90m. c. 2021:$60m. Required: Prepare a professional letter of advice advising Patrick of the trading stock implications of the above transactions. In this letter of advice please: 1. Calculate the following for each of the 2019, 2020 and 2021 income years at cost: a. Opening stock, b. Purchases, c. Closing stock, d. Gross profit, and e. Net profit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts