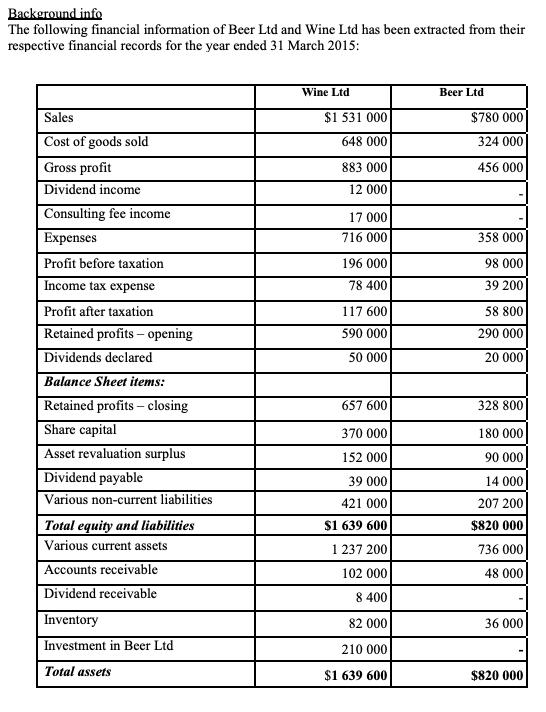

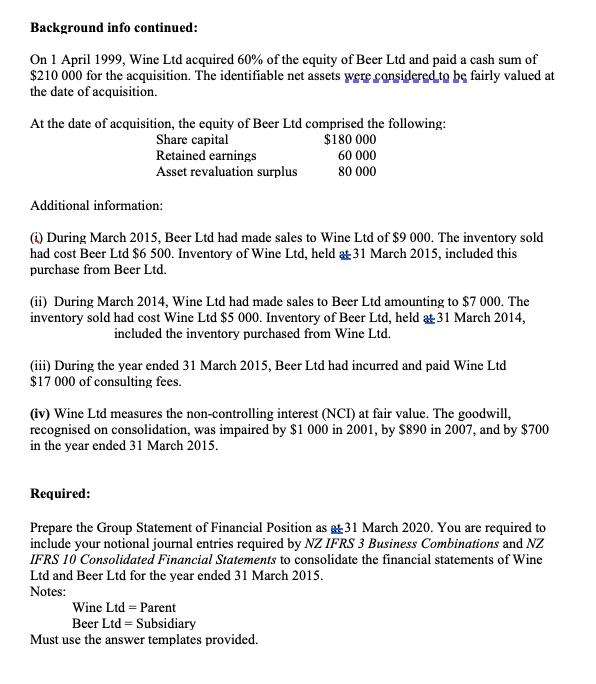

Background info The following financial information of Beer Ltd and Wine Ltd has been extracted from...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answer 1 Group Statement of Financial Position as at 31 March 2015 ASSETS NonCurrent Assets Property plant and equipment Wine Ltd 1237200 Beer Ltd 736000 Investment in Beer Ltd Wine Ltd 210000 Total n... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott

Posted Date: