Question: Background information The profit before tax, reported in the statement of comprehensive income of Mexis Ltd for the year ended 30 June 2021 amounted to:

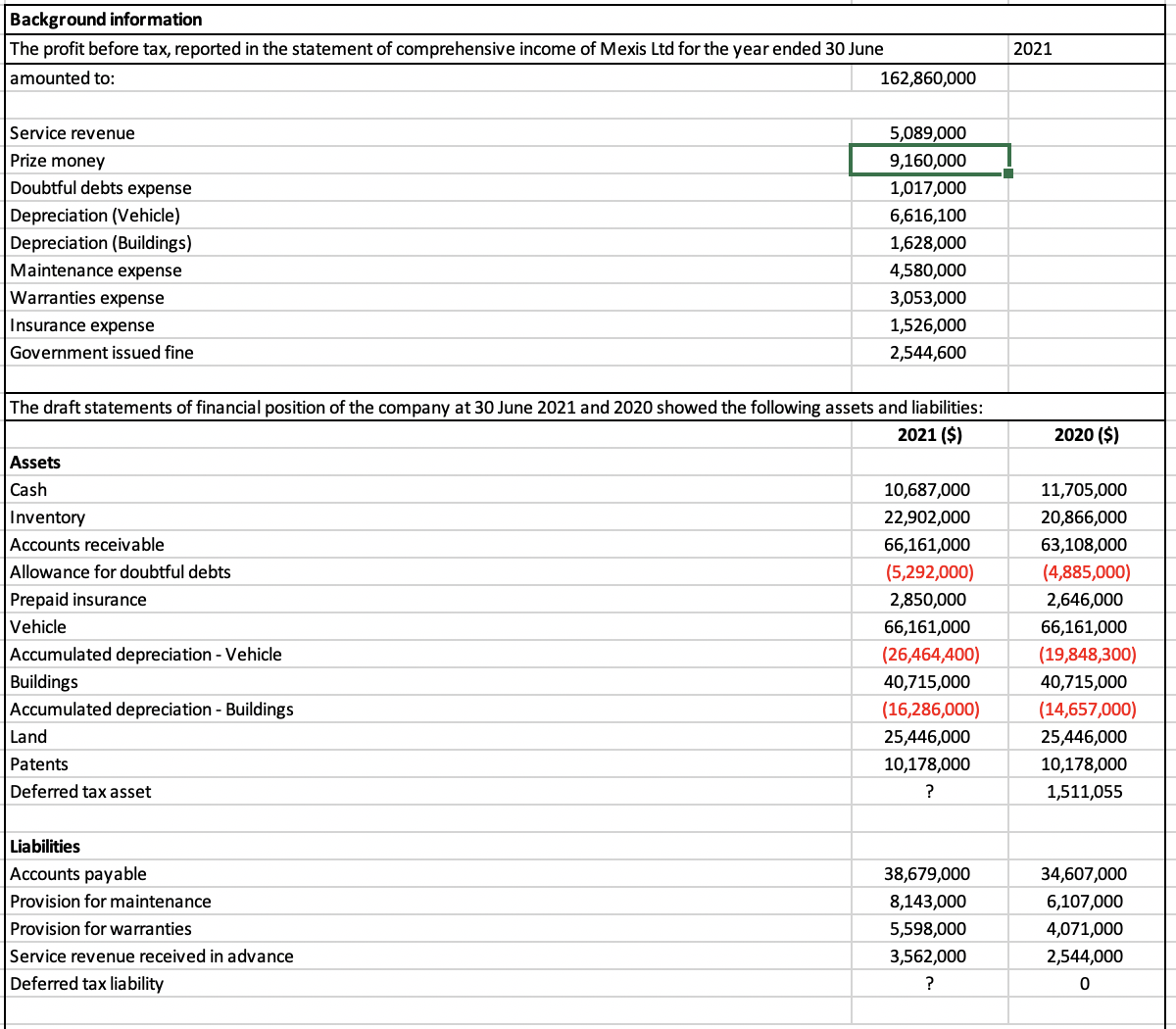

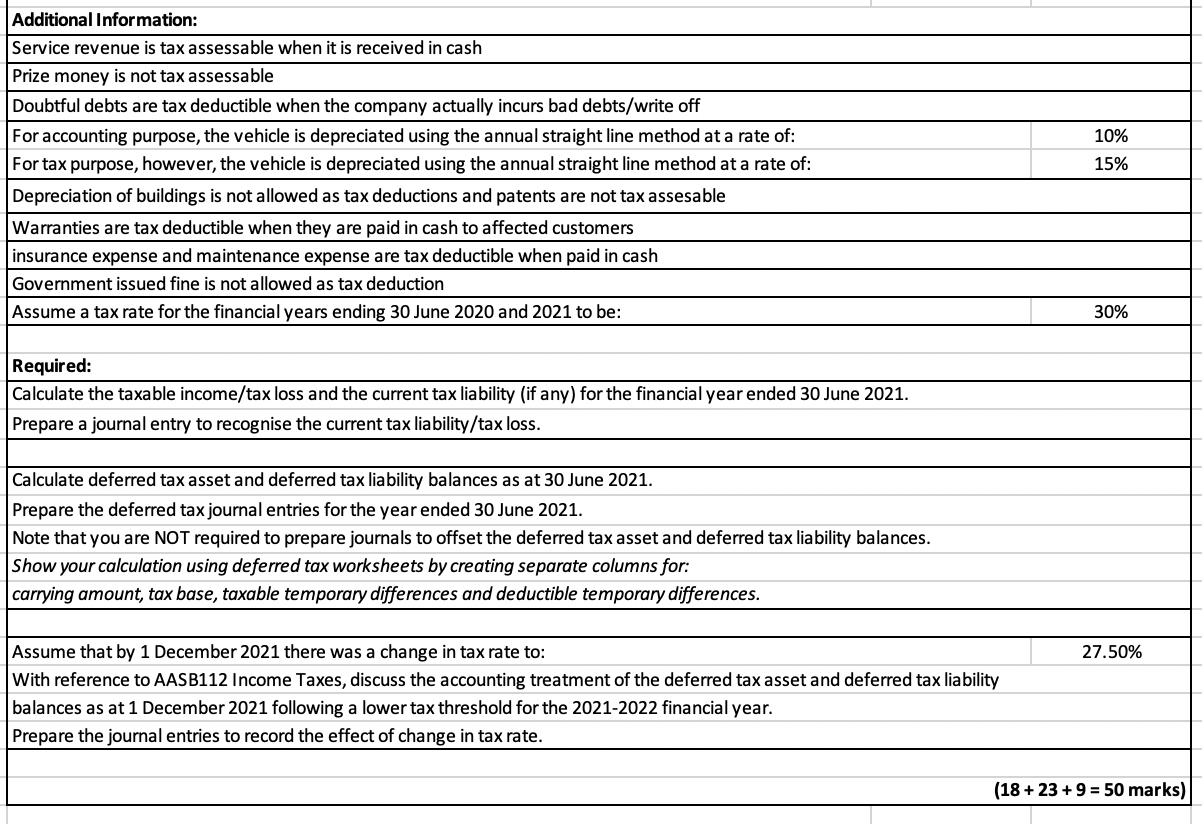

Background information The profit before tax, reported in the statement of comprehensive income of Mexis Ltd for the year ended 30 June 2021 amounted to: 162,860,000 Service revenue 5,089,000 Prize money 9,160,00 Doubtful debts expense 1,017,000 Depreciation (Vehicle 6,616,100 Depreciation (Buildings) 1,628,000 Maintenance expense 4,580,000 Warranties expense 3,053,000 Insurance expense 1,526,000 Government issued fine 2,544,600 The draft statements of financial position of the company at 30 June 2021 and 2020 showed the following assets and liabilities: 2021 ($) 2020 ($) Assets Cash 10,687,000 11,705,000 Inventory 22,902,000 20,866,000 Accounts receivable 66,161,000 63,108,000 Allowance for doubtful debts (5,292,000) (4,885,000) Prepaid insurance 2,850,000 2,646,000 Vehicle 66,161,000 66,161,000 Accumulated depreciation - Vehicle (26,464,400) (19,848,300) Buildings 40,715,000 40,715,000 Accumulated depreciation - Buildings (16,286,000) (14,657,000) Land 25,446,000 25,446,000 Patents 10,178,000 10,178,000 Deferred tax asset ? 1,511,055 Liabilities Accounts payable 38,679,000 34,607,000 Provision for maintenance 8,143,000 6,107,000 Provision for warranties 5,598,000 4,071,000 Service revenue received in advance 3,562,000 2,544,000 Deferred tax liability ? 0Additional Information: Service revenue is tax assessable when it is received in cash Prize money is not tax assessable Doubtful debts are tax deductible when the company actually incurs bad debts/write off For accounting purpose, the vehicle is depreciated using the annual straight line method at a rate of: 10% For tax purpose, however, the vehicle is depreciated using the annual straight line method at a rate of: 15% Depreciation of buildings is not allowed as tax deductions and patents are not tax assesable Warranties are tax deductible when they are paid in cash to affected customers insurance expense and maintenance expense are tax deductible when paid in cash Government issued fine is not allowed as tax deduction Assume a tax rate for the financial years ending 30 June 2020 and 2021 to be: 30% Required: Calculate the taxable income/tax loss and the current tax liability (if any) for the financial year ended 30 June 2021. Prepare a journal entry to recognise the current tax liability/tax loss. Calculate deferred tax asset and deferred tax liability balances as at 30 June 2021. Prepare the deferred tax journal entries for the year ended 30 June 2021. Note that you are NOT required to prepare journals to offset the deferred tax asset and deferred tax liability balances. Show your calculation using deferred tax worksheets by creating separate columns for: carrying amount, tax base, taxable temporary differences and deductible temporary differences. Assume that by 1 December 2021 there was a change in tax rate to: 27.50% With reference to AASB112 Income Taxes, discuss the accounting treatment of the deferred tax asset and deferred tax liability balances as at 1 December 2021 following a lower tax threshold for the 2021-2022 financial year. Prepare the journal entries to record the effect of change in tax rate. (18 + 23 + 9 = 50 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts