Question: Background Torus Technologies Inc. Torus Technologies is a Canadian multinational company, privately owned, that specializes in design and manufacturing of complete digital transmission systems as

Background

Torus Technologies Inc.

Torus Technologies is a Canadian multinational company, privately owned, that specializes in

design and manufacturing of complete digital transmission systems as well as individual

components for digital audio and video broadcasting.

The company has been in business since 1990 and was trading on the Toronto Stock Exchange

until 2003, when management bought the manufacturing and technology development assets

and created a privately held company known today as Torus Technologies. Inspired by strong

demand for its products and in anticipation of rising sales of digital broadcasting equipment,

Torus Technologies vigorously expanded its global presence by establishing subsidiaries in

some of the most promising markets around the world. Presently, Torus Beijing, Torus America,

and Torus Europe are all controlled by Torus Technologies and constitute an integral part of the

firms corporate strategy, directed at supporting Torus Technologies international clients and

promoting its products and services abroad.

While Torus Technologies has a very comprehensive and highly competitive product line, which

continuously expands, the primary focus has always been on customization of design and

production to address the specific needs of its clients in the following sectors:

Broadcast

Instrumentation & Scientific Equipment

Military (TACAN) / Radar

SATCOM

Amplifiers

The focus of the company is on the following areas:

GaN / GaAs / LDMOS - based high power indoor and outdoor amplifier systems, phase

combined to achieve power level up to 10 KW.

Solid state amplifier modules

Satellite/ Terrestrial SFN & MFN Solution

Adaptive pre-correction for power amplifier linearization

Digital Modulation solution for all key international standards ( Including DVB T/H, DVB

SH, DVB T2, DVB S2, DAB, DTMB. CMMB, ISDB-T, ISDBT-TB and ATSC)

Passives components including waveguide (Including flex), Couplers filters and other co-

axial parts

Military RF and Calibration equipment (TACAN (IFF) and UHF Amplifier)

Mobile digital television and radio broadcasting equipment.

Torus Technologies is widely-recognized and has a reputation for designing, developing, and

manufacturing solid-state high-power amplifiers that are critically important for satellite,

industrial, scientific, and medical applications.

Torus had developed a proprietary technology to manufacture broadband and band-specific

solid state power amplifiers and the demand has steadily increased over the years due to

increase in mobile communications and satellite deployments.

However, the maintenance costs have increased significantly in the last period. The amplifiers

are designed to work in extreme conditions and the repairs and maintenance are done, most of

the time, remotely. If one component of the amplifier malfunctions, it is critical to fix it

immediately; otherwise the issue could cascade and trigger the failure of all other components.

Usually, the clients detect and report the problems with the amplifiers very late in the process

making the repair extremely costly. Also this has a significant negative impact on the customer

satisfaction.

The Project

To overcome this problem, Toruss management decided to launch a new device that will be

installed inside the amplifiers to continuously monitor and stream data related to the functioning

performance of all components.

In this way, issues related to different components will be identified and fixed soon after they

occur without the client involvement. Moreover, this device will provide statistics related to the

quality of components and their behavior in different environments allowing Torus to optimize

the product quality for the clients specific needs.

At the same time by manufacturing this new device, Torus has the opportunity to expand the

scope of the project beyond internal need as other manufacturers of equipment might face the

same issues. After conducting a market research, Toruss management expects that the new

device can be sold externally with minimum adjustments.

Torus decided to set up a separate department with the exclusive mandate of designing,

launching, manufacturing and marketing the new device internally and externally. This new

department would be an investment center.

You as a Toruss controller have to determine if the project is feasible based on the following

estimations provided by the management; the life of the project is 10 years:

The new division will generate revenue from two streams: internal orders for amplifiers and

external clients.

Toruss management estimates that internal sales will be 8,500 units in the first year and it will

increase between 5% and 15% per year the following years.

After internal analysis and discussions, the transfer price of the new device was set up to equal

the variable cost plus 16%.

An analyst hired by Torus estimates that the new division will be able to sell 6000 units in the first year to external clients and it expects a subsequent increase between 3% to 12% year over year. This estimation is based on a selling price of $ 320

The standard usage of materials for the new device is 1.9 meters of copper cable, one chip of

$50, and other raw materials totaling $22. It customary for Torus, to purchase copper cables

only in large rolls of 325 meters at a price of $1,144 per roll.

Assembly workers are paid at an hourly rate of $45 and testers at a rate of $60 per hour.

The company policy is to increase salaries with the inflation rate plus 1%. It is estimated that the

inflation rate will be constant in the foreseeable future at 2 per year.

The standard labour required for the device is 3.5 hours for assembly and 1.5 for testing.

The overhead costs will be $300,000 in the first year and expected to increase at a rate of 1%

per year.

Working Capital needed is $400,000, which will be recovered fully at the end of the project.

To promote the new device to external clients, Torus will spend an estimated $200,000 per

year.

Every 2 years an additional $40,000 is required for software development and deployment. The

first software upgrade is expected to take place in year 3.

Depreciation

Total investment in the project is estimated at $3,500,000 from which 20 % will be invested in

software development (no salvage value) Class 10, CCA rate 30%, and the remaining amount

will be used to acquire a new assembly line (Class 8, CCA rate 20%), the assembly line has a

salvage value estimated at 15% of the original price.

WACC

Torus has another $3,000,000 bank loan with an effective interest rate of 7%;

$6,000,000, 8%, 17-year bonds selling at 85% of face value;

$4,500,000 of 8%, $10 noncumulative, non-callable preferred stock with a total market

value of $2,440,000;

100,000 shares of $10 par common stock, with a total current market value of

$6,500,000. The estimated required rate of return on the common stock, based on

application of the CAPM, is 15%.

Other

The firm is subject to a 40% income tax rate, and it uses 10% discount rate.

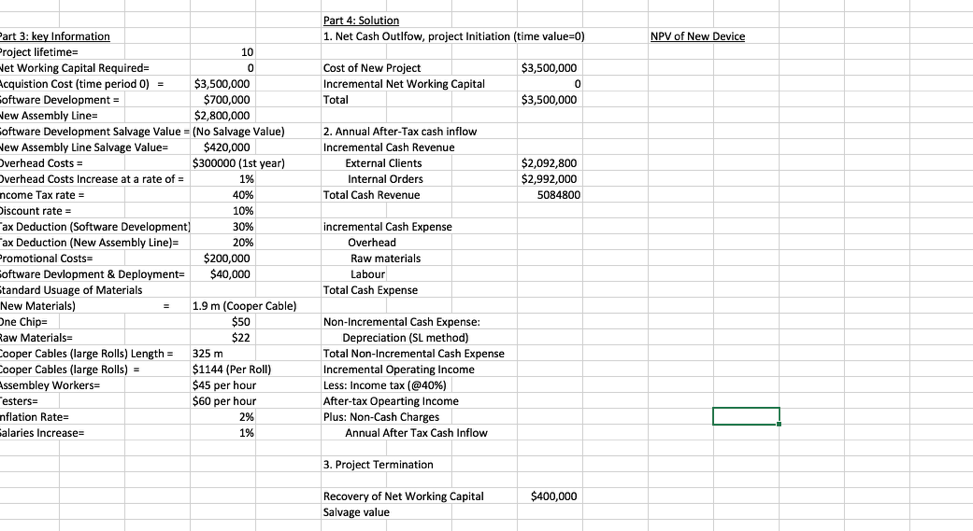

Hi, My Previous question similar to this wasn't answered for some reason What I'm wondering is how will we calculate the NPV or the MIRR or IRR using this information because it seems its all over the place. Here's what I have worked up so far can someone tell me at the very least if I am on track. Please and thanks :

1. Net Cash Outlfow, project Initiation (time valu NPV of New roject lifetime- et Working Capital Required cquistion Cost (time period 0)$3,500,000 oftware Development ew Assembly Line oftware Development Salvage Value-(No Salvage Value) ew Assembly Line Salvage Value verhead Costs- verhead Costs Increase at a rate of- ncome Tax rate iscount rate- ax Deduction (Software Development ax Deduction (New Assembly Line)- romotional Costs oftware Devlopment& Deployment $40,000 tandard Usuage of Materials New Materials) ne Chip aw Materials- ooper Cables (large Rolls) Length325 m ooper Cables (large Rolls)- ssembley Workers esters nflation Rate- alaries Increase:- 10 0 3,500,000 Cost of New Project Incremental Net Working Capital Total 0 3,500,000 $700,000 $2,800,000 2.Annual After-Tax cash inflow Incremental Cash Revenue $420,000 300000 (1st year) External Clients Internal Orders Total Cash Revenue 2,092,800 2,992,000 5084800 1% 40% 10% 3096 20% $200,000 incremental Cash Expense Overhead Raw materials Labour Total Cash Expense 1.9 m (Cooper Cable) $50 $22 Non-Incremental Cash Expense Depreciation (SL method) Total Non-Incremental Cash Expense Incremental Operating Income Less: Income tax (@40%) After-tax Opearting Income Plus: Non-Cash Charges $1144 (Per Roll $45 per hour $60 per hour 2% 1% Annual After Tax Cash Inflow 3. Project Termination $400,000 Recovery of Net Working Capital Salvage value

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts