In the practice set you will have the opportunity to maintain a set of accounting records...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

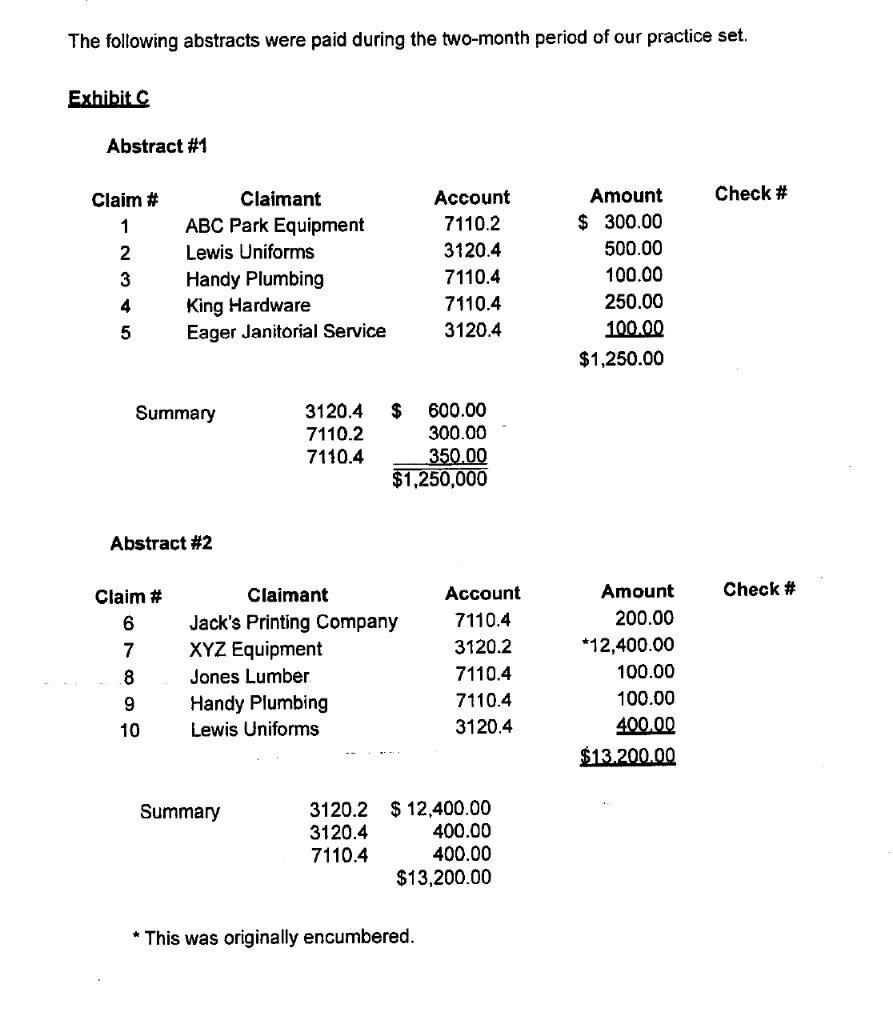

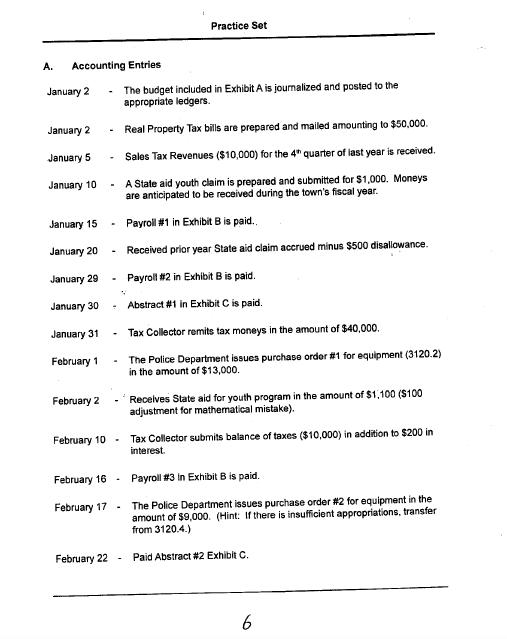

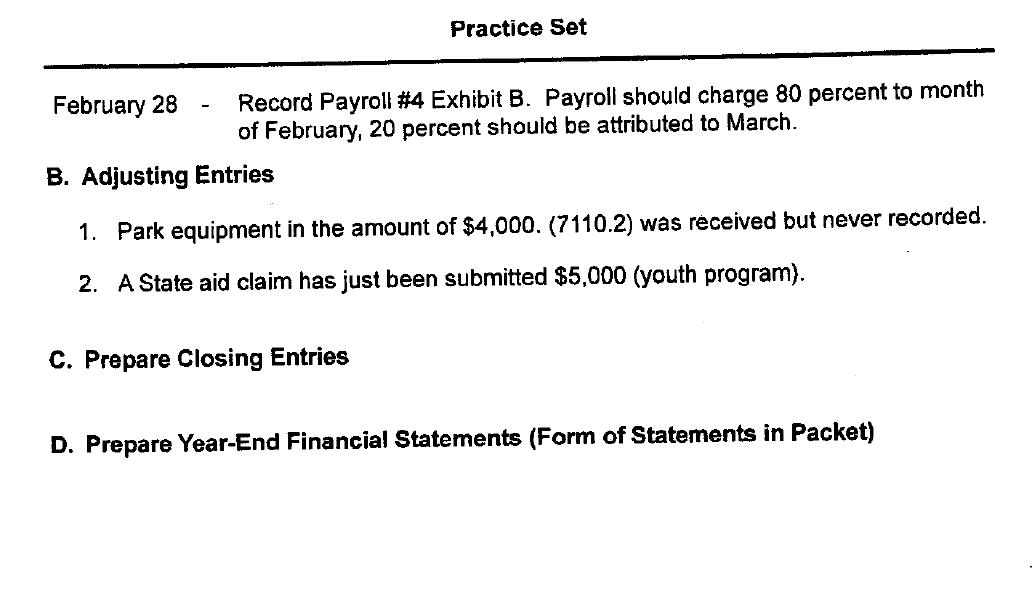

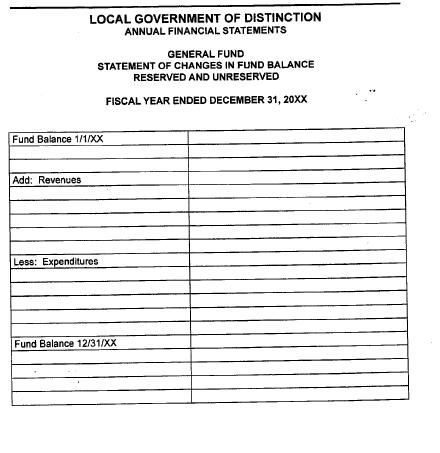

In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX In the practice set you will have the opportunity to maintain a set of accounting records for a typical local town government encompassing the first two months of its fiscal year. At the end of the second month we will make the adjusting and closing entries as if it were the end of the fiscal year. We will also prepare the appropriate financial statements. The town maintains its accounting records on the modified accrual basis of accounting. This means that all material items of revenues earned or expenditures incurred are accrued in order to prepare the financial statements. The accounting system used by the town is prescribed by the State Comptroller and consists of the following records: > General Journal Cash Disbursements Journal > Cash Receipts Journal General Ledger > Subsidiary Expenditure Ledger Subsidiary Revenue Ledger Also included in the practice set is a chart of accounts and a schedule of exhibits to assist in recording the appropriate transactions. Balances from the previous year have been brought forward in the General Ledger. General Fund -General Ledger Account Codes CHART OF ACCOUNTS Assets A200 Cash A201 Cash in Time Deposits A250 Taxes Receivable, Current A410 State and Federal, Other A440 Due from Other Governments Budgetary and Expenditure Accounts A510 Estimated Revenues A521 Encumbrances A522 Expenditures A599 Appropriated Fund Balance Liabilities A600 Accounts Payable A601 Accrued Liabilities Fund Balance, Reserved A821 Reserve for Encumbrances Fund Balance, Unreserved A909 Fund Balance, Unreserved Budgetary and Revenue Accounts A960 Appropriations A980 Revenues General Fund - Individual Revenue and Expenditure Account Codes Revenue Account Codes A1001 Real Property Taxes A1090 Interest on Taxes A1120 A1255 Clerk Fees A3820 Youth Programs Non-Property Tax Distribution by County (Sales Tax) Expenditure Account Codes A1990.4 Contingent Account A3120.1 Police Personal Services A3120.2 Police - Equipment and Other Capital Outlay A3120.4 Police - Contractual Expenditure A7110.1 Parks Personal Services A7110.2 Parks - Equipment and Other Capital Outlay A7110.4 Parks - Contractual Expenditure Practice Set - Assumptions and Exhibits The following assumptions and exhibits will be used in preparing the practice set. The Town's opening balances are: Cash State and Federal, Other Due from Other Governments 909 Fund Balance (General Ledgers are already posted) 200 410 440 Exhibit A The following budget was approved for 20XX year: A510 Estimated Revenues A1001 A1120 A3820 Real Property Taxes Sales Tax State Aid A599 Appropriated Fund Balance A960 Appropriations $40,000 $10,000 $10,000 $50,000 40,000 10,000 $60,000 $ 100,000 $ 30,000 $ 130,000 Appropriation Subsidiaries A3120.1 Police Personal Services A3120.2 Police Equipment Contractual A3120.4 Police A7110.1 A7110.2 A7110.4 A1990.4 Parks - Personal Services Parks - Equipment Parks - Contractual Contingent Account Exhibit B The following payrolls were prepared and recorded during the first two months. The town pays all employees on a bi-weekly basis. Police Parks Police Parks (only gross payroll entries will be made) Police Parks Payroll #1 3120.1 7110.1 Police Parks Payroll #2 3120.1 7110.1 Payroll #3 3120.1 7110.1 $ 50,000 21,000 11,000 25,000 12,000 10,000 1.000 $130.000 Payroll #4 3120.1 7110.1 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $1,500.00 $ 750.00 $ 1,500.00 $ 750.00 The following abstracts were paid during the two-month period of our practice set. Exhibit C Abstract #1 Claim # 1 2 3 4 5 Claimant ABC Park Equipment Lewis Uniforms Handy Plumbing King Hardware Eager Janitorial Service Summary Abstract #2 Claim # 6 7 8 9 10 3120.4 $ 7110.2 7110.4 Claimant Jack's Printing Company XYZ Equipment Jones Lumber Handy Plumbing Lewis Uniforms Summary 600.00 300.00 350.00 $1,250,000 3120.2 3120.4 7110.4 Account 7110.2 3120.4 7110.4 7110.4 3120.4 * This was originally encumbered. Account 7110.4 3120.2 7110.4 7110.4 3120.4 $12,400.00 400.00 400.00 $13,200.00 Amount $ 300.00 500.00 100.00 250.00 100.00 $1,250.00 Amount 200.00 *12,400.00 100.00 100.00 400.00 $13.200.00 Check # Check # A. Accounting Entries January 2 January 2 January 5 January 10 January 15 January 20 January 29 January 30 January 31 February 1 February 2 February 10 February 22 The budget included in Exhibit A is journalized and posted to the appropriate ledgers. Real Property Tax bills are prepared and mailed amounting to $50,000. Sales Tax Revenues ($10,000) for the 4" quarter of last year is received. - A State aid youth claim is prepared and submitted for $1,000. Moneys are anticipated to be received during the town's fiscal year. Payroll #1 in Exhibit B is paid. Received prior year State aid claim accrued minus $500 disallowance. Payroll #2 in Exhibit B is paid. Abstract #1 in Exhibit C is paid. - . - February 16 February 17 - Practice Set Y Tax Collector remits tax moneys in the amount of $40,000. The Police Department issues purchase order #1 for equipment (3120.2) in the amount of $13,000. Receives State aid for youth program in the amount of $1,100 ($100 adjustment for mathematical mistake). Tax Collector submits balance of taxes ($10,000) in addition to $200 in interest. Payroll #3 in Exhibit B is paid. The Police Department issues purchase order #2 for equipment in the amount of $9,000. (Hint: If there is insufficient appropriations, transfer from 3120.4.) Paid Abstract #2 Exhibit C. 6 February 28 Record Payroll #4 Exhibit B. Payroll should charge 80 percent to month of February, 20 percent should be attributed to March. B. Adjusting Entries Practice Set 1. Park equipment in the amount of $4,000. (7110.2) was received but never recorded. 2. A State aid claim has just been submitted $5,000 (youth program). C. Prepare Closing Entries D. Prepare Year-End Financial Statements (Form of Statements in Packet) LOCAL GOVERNMENT OF DISTINCTION ANNUAL FINANCIAL STATEMENTS Add: Revenues GENERAL FUND STATEMENT OF CHANGES IN FUND BALANCE RESERVED AND UNRESERVED FISCAL YEAR ENDED DECEMBER 31, 20XX Fund Balance 1/1/XX Less: Expenditures Fund Balance 12/31/XX

Expert Answer:

Answer rating: 100% (QA)

Step 1 Recording Transactions Using the prescribed accounting records and the chart of accounts prov... View the full answer

Related Book For

Fraud examination

ISBN: 978-0538470841

4th edition

Authors: Steve Albrecht, Chad Albrecht, Conan Albrecht, Mark zimbelma

Posted Date:

Students also viewed these accounting questions

-

Is it possible to maintain a pressure of 10 kPa in a condenser that is being cooled by river water entering at 20C?

-

Why is it important to maintain a chain of custody for documentary evidence?

-

a) "It is always best to maintain a level of working capital that is as high as possible." Discuss. b) Explain what the balanced scorecard is and suggest two performance measures that are relevant to...

-

Company OMEGA wants to invest in Bonds and Stocks. The financial manager was looking at different types of Bonds and Stocks. After studying the market, he decided to choose 3 bonds and 3 stocks....

-

A loan of $6000 was repaid by quarterly payments of $450. If interest was 12% compounded monthly, how long did it take to pay back the loan?

-

What is the difference between primary data and secondary data?

-

Find all components of the stiffness and compliance matrices for a specially orthotropic lamina made of AS/3501 carbon/epoxy.

-

You are the regional manager of a chain of stores selling computer equipment and accessories, mainly based on out-of-town retail parks. Following promotion, a new manager has just been appointed to...

-

Here is some hypothetical testimony from prosecution of an assault of a victim in a grocery store parking lot: The prosecutor calls Bart (an eyewitness and the "primary" or "fact" witness in this...

-

Joe and Jessie are married and have one dependent child, Lizzie. Lizzie is currently in college at State University. Joe works as a design engineer for a manufacturing firm while Jessie runs a craft...

-

A consumer's utility function is given by Ux1,x2=2x1x2+3x1U(x1,x2) = 2x1x2 + 3x1 where x1*1 and x2 %3D X2 denote the number of items of two goods G1 and G2 that are bought. Each item costs $1 for G1...

-

A female snail that coils to the left has offspring that coil to the right. What are the genotypes of this mother and of the maternal grandmother of the offspring, respectively? a. dd, DD b. Dd, Dd...

-

Two different strains of sweet peas are true-breeding and have white flowers. When plants of these two strains are crossed, the F1 offspring all have purple flowers. This outcome is due to a....

-

A female born with Angelman syndrome carries a deletion in the AS gene (i.e., the UBE3A gene). Which parent transmitted the deletion to her? a. Her father c. Either her mother or father b. Her mother

-

A pea plant has the genotype TtRr. The independent assortment of these two genes occurs at ________ because chromosomes carrying the _______ alleles line up independently of the chromosomes carrying...

-

A cross is made between a green four-oclock plant and a variegated one. If the variegated plant provides the pollen, the expected outcome of the phenotypes of the offspring will be a. all plants with...

-

A movie stunt performer is filming a scene where he swings across a river on a vine. The safety crew must use a vine with enough strength so that it doesn't break while swinging. The stunt...

-

The value of a share of common stock depends on the cash flows it is expected to provide, and those flows consist of the dividends the investor receives each year while holding the stock and the...

-

Bill and Sue were college students when they met each other in the library and began dating. After a few short months, they decided to get married. After a time of marital bliss, both Bill and Sue...

-

After working out at the gym, you notice that your car has been broken into and your wallet has been stolen. What should you do?

-

Robert was the chief teller in a large New York bank. Over a period of three years, he embezzled $1.5 million. He took the money by manipulating dormant accounts. Unfortunately, Robert was both...

-

The financial year end for Florence Ltd is 31 December 20X7. Calculate the amount charged to the income statement and the balance outstanding (for the balance sheet) in respect of the following...

-

Electricity bills amounting to 4,500 were paid by Edinburgh Ltd during the year ended 31 December 20X7. All of these bills relate to the year ended 31 December 20X7. A bill of :1,500 was received in...

-

The following is the trial balance of Cadiz Ltd as at 31 December. You also know that the inventory at 31 December is 380,000. You are required to: prepare an income statement for the year ended 31...

Study smarter with the SolutionInn App