Question: Based on the data provided in the table below, delta, gamma, and vega neutralize the option portfolio with the $55-strike and the $60-strike call

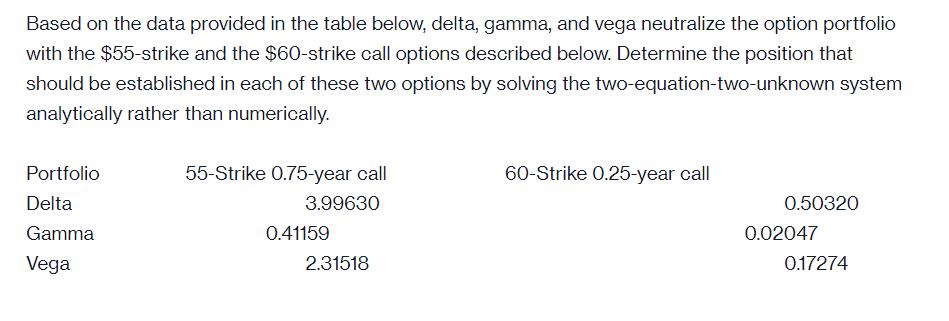

Based on the data provided in the table below, delta, gamma, and vega neutralize the option portfolio with the $55-strike and the $60-strike call options described below. Determine the position that should be established in each of these two options by solving the two-equation-two-unknown system analytically rather than numerically. Portfolio Delta Gamma Vega 55-Strike 0.75-year call 3.99630 0.41159 2.31518 60-Strike 0.25-year call 0.50320 0.02047 0.17274

Step by Step Solution

3.39 Rating (152 Votes )

There are 3 Steps involved in it

To delta gamma and vega neutralize the option portfoli... View full answer

Get step-by-step solutions from verified subject matter experts