Question: Based on the information provided in question 2, the 1-yr and 3-yr zero bond prices are: $0.986 and $0.942, respectively $0.916 and $0.999, respectively $0.816

Based on the information provided in question 2, the 1-yr and 3-yr zero bond prices are:

| $0.986 and $0.942, respectively | ||

| $0.916 and $0.999, respectively | ||

| $0.816 and $0.982, respectively | ||

| $0.926 and $0.957, respectively |

Based on the information reported in Table from question 2, what is the forward rate between year 1.5 and year 2?

| a. | 1% | |

| b. | 3% | |

| c. | 2% | |

| d. | 4% |

QUESTION 5

Based on the information reported in Table from question 2, what is the forward rate between year 2.5 and year 3?

| a. | 2% | |

| b. | 3% | |

| c. | 4% | |

| d. | 1% |

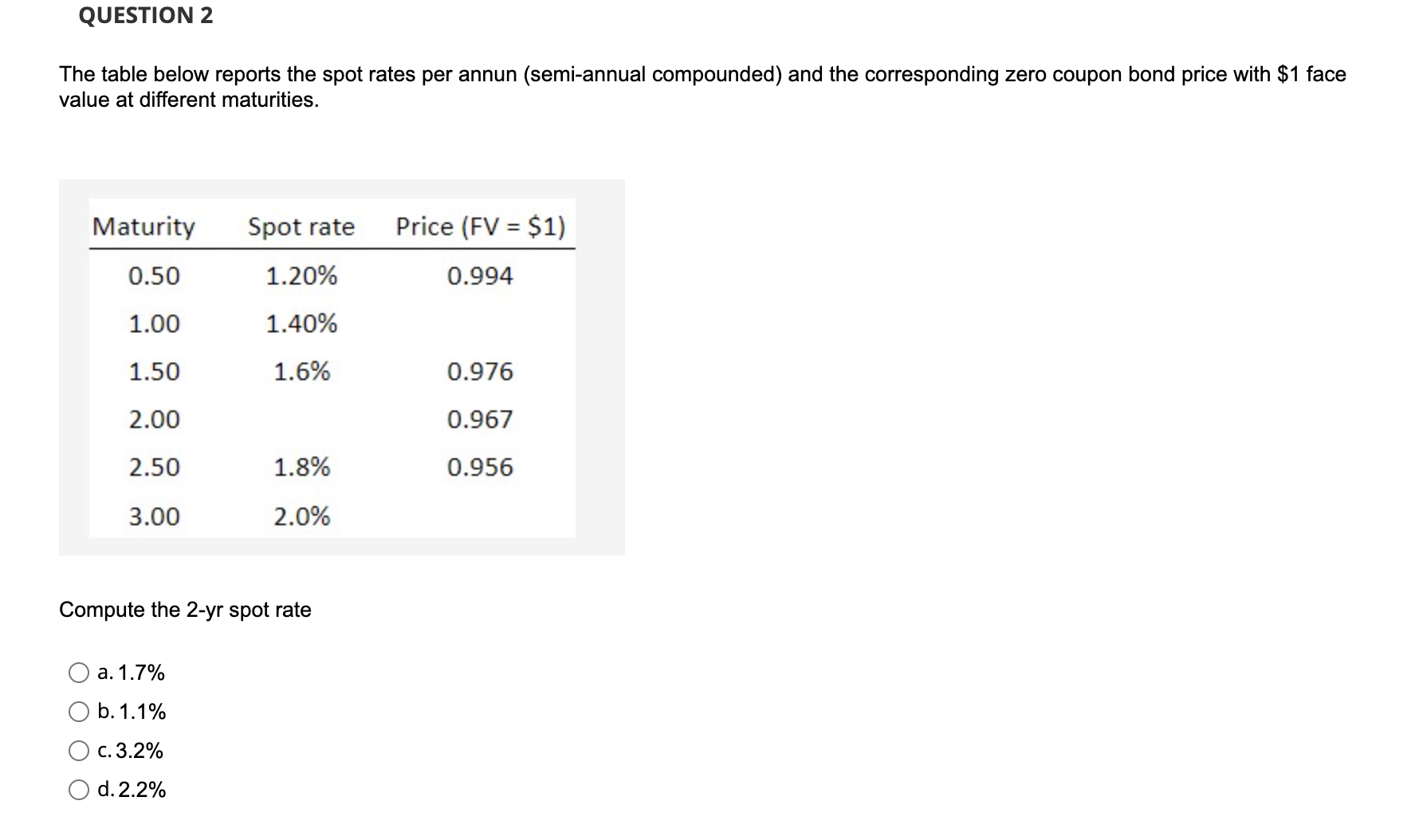

The table below reports the spot rates per annun (semi-annual compounded) and the corresponding zero coupon bond price with $1 face value at different maturities. Compute the 2-yr spot rate a. 1.7% b. 1.1% c. 3.2% d. 2.2%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock