Question: Based on the information provided, please give 2 0 2 3 & 2 0 2 2 estiamxed equity beta and Unlevered ( Asset ) Beta

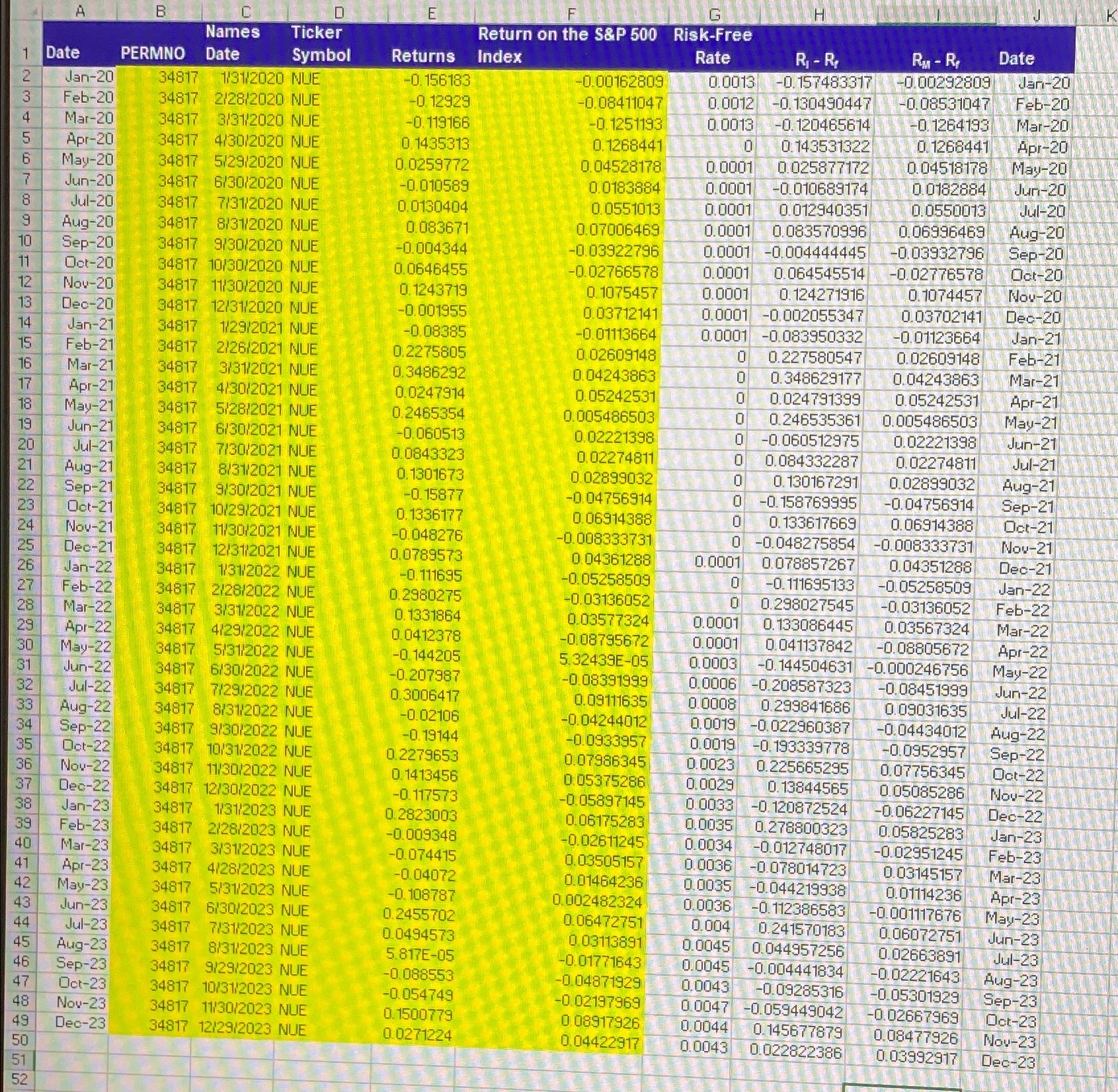

Based on the information provided, please give & estiamxed equity beta and Unlevered Asset Beta numbers. Betas should be calculated using a month rolling return window. Use monthly returns from January december to etimate your equity beta and the monthly returns from Jan Dec. to estimate beta.

Once equity beta is calculated, Net debt and Market value of equity are used to calculate asset beta for firm.

Assume debt beta is equel to zero.

net debt ; $ MVE:

net debt: MVE;

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock