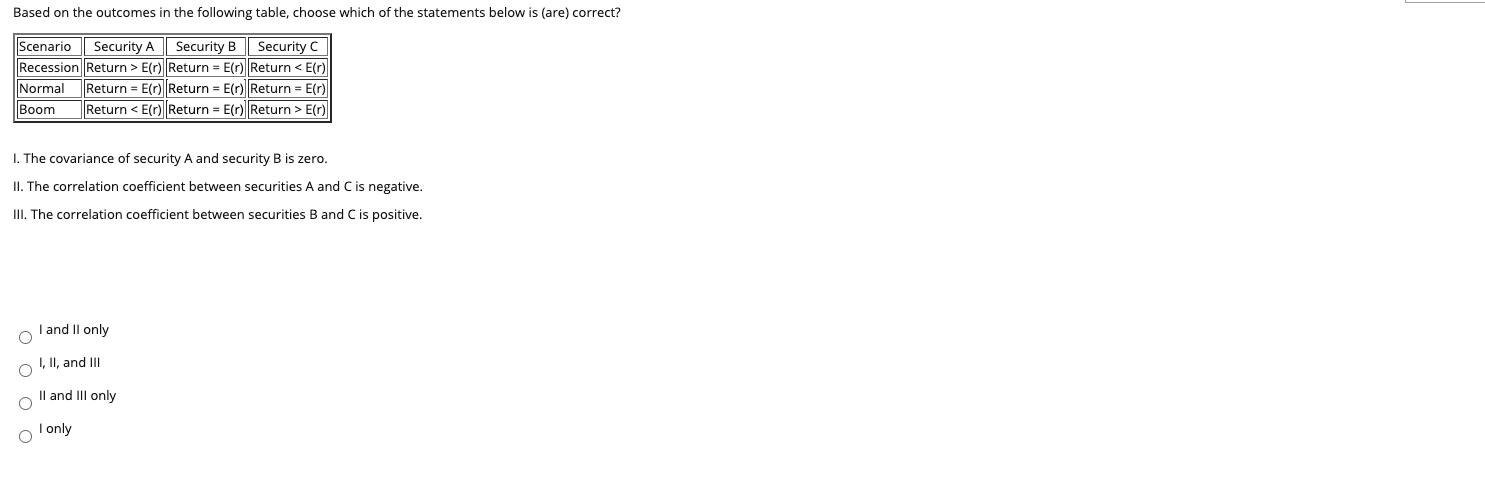

Question: Based on the outcomes in the following table, choose which of the statements below is (are) correct? Scenario Security A Security B Security C Recession

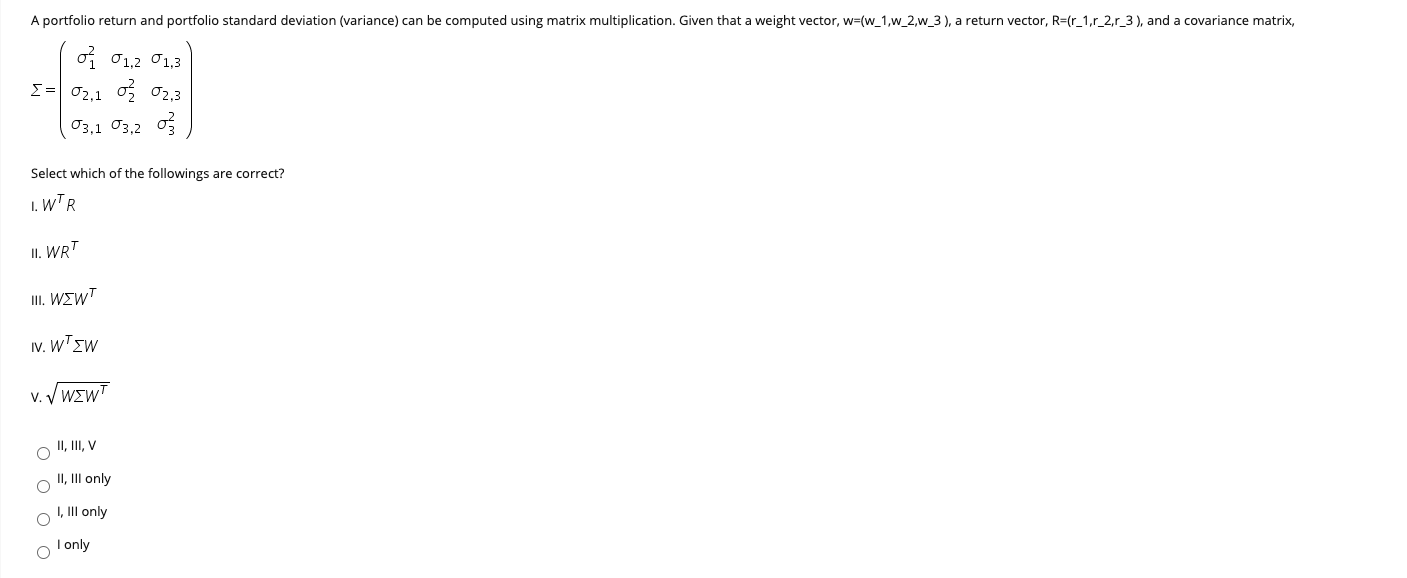

Based on the outcomes in the following table, choose which of the statements below is (are) correct? Scenario Security A Security B Security C Recession Return > E() Return = E() Return E() 1. The covariance of security A and security B is zero. II. The correlation coefficient between securities A and C is negative. III. The correlation coefficient between securities B and C is positive. I and Il only I, II, and III II and III only I only An investment firm, FINC3330, uses the Fama-French three factor model. The risk-free rate equals 3%. Factor Exposures 1.2 Factors Market Size (SMB) Value (HML) Factor Risk Premiums 0.05 0.015 0.08 0.39 0.8 The expected excess return for its portfolio from the above result would be % and the expected return on the portfolio would be %. (Note: Round to the nearest hundredth.) A portfolio return and portfolio standard deviation (variance) can be computed using matrix multiplication. Given that a weight vector, w=(w_1,w_2,w_3), a return vector, R=(r_1,r_2.r_3), and a covariance matrix, o 01,201,3 = 02.10 02,3 03,1 03,2 op Select which of the followings are correct? 1. WTR II. WRT III. WEWT iv. WTEW v. VWEW II, III, V II, III only I, III only 0 0 I only

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts