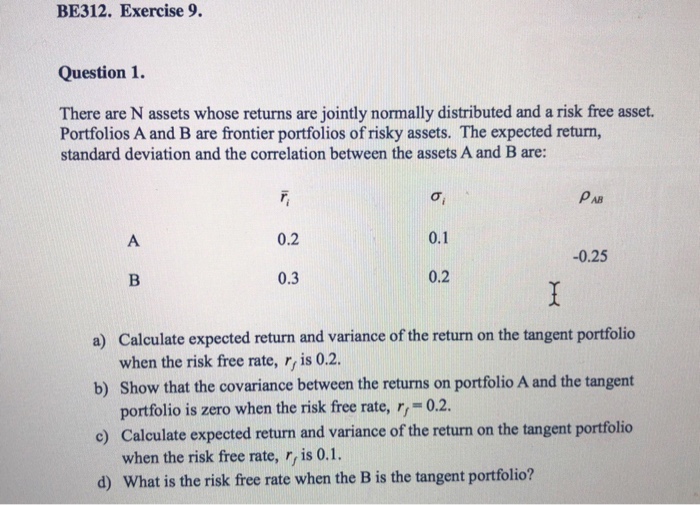

Question: BE312. Exercise 9 Question 1. There are N assets whose returns are jointly normally distributed and a risk free asset. Portfolios A and B are

BE312. Exercise 9 Question 1. There are N assets whose returns are jointly normally distributed and a risk free asset. Portfolios A and B are frontier portfolios of risky assets. The expected return, standard deviation and the correlation between the assets A and B are: ?i 0.1 0.2 AB 0.2 -0.25 0.3 Calculate expected return and variance of the return on the tangent portfolio a) b) Show that the covariance between the returns on portfolio A and the tangent c) Calculate expected return and variance of the return on the tangent portfolio d) What is the risk free rate when the B is the tangent portfolio? when the risk free rate, r, is 0.2. portfolio is zero when the risk free rate, r,-0.2. when the risk free rate, r, is 0.1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts