Question: Because Valuation Allowances are primarily a judgement call this assignment will focus simply on making that decision. We want you to practice exing some professional

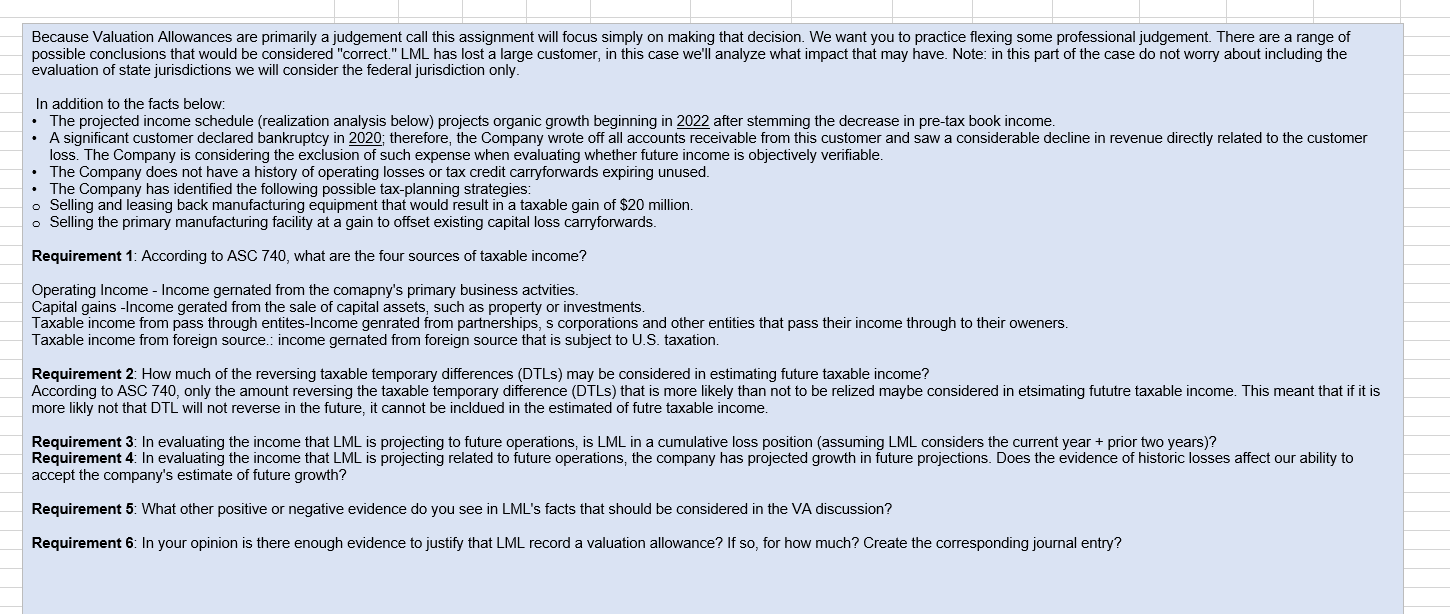

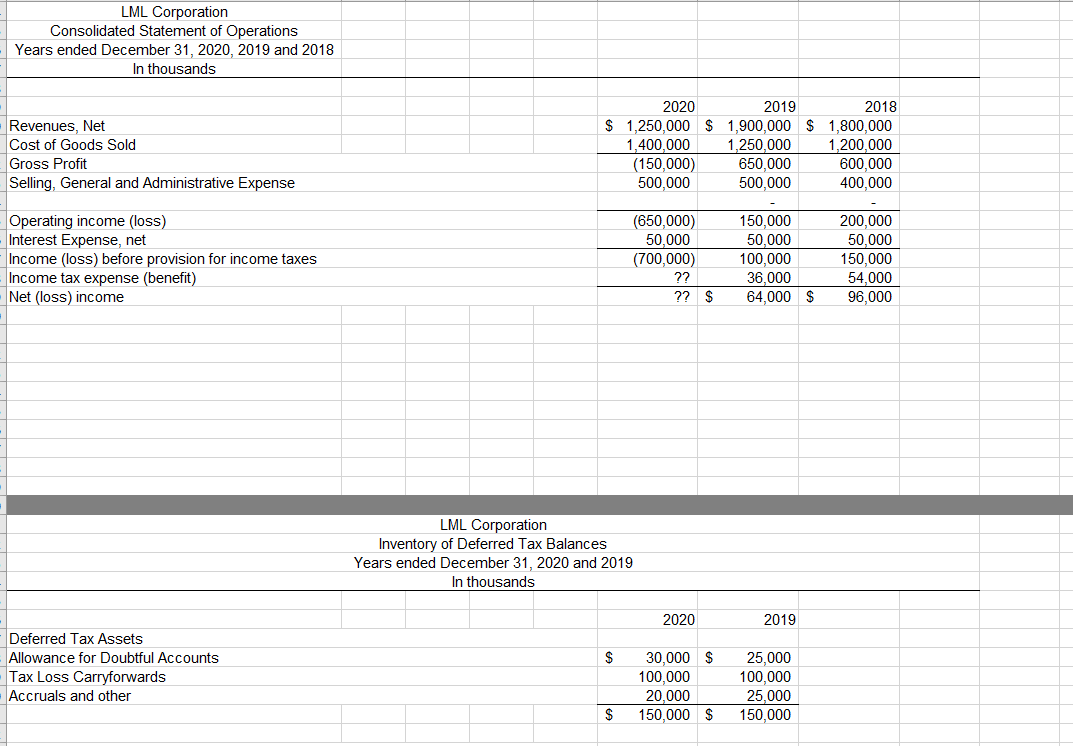

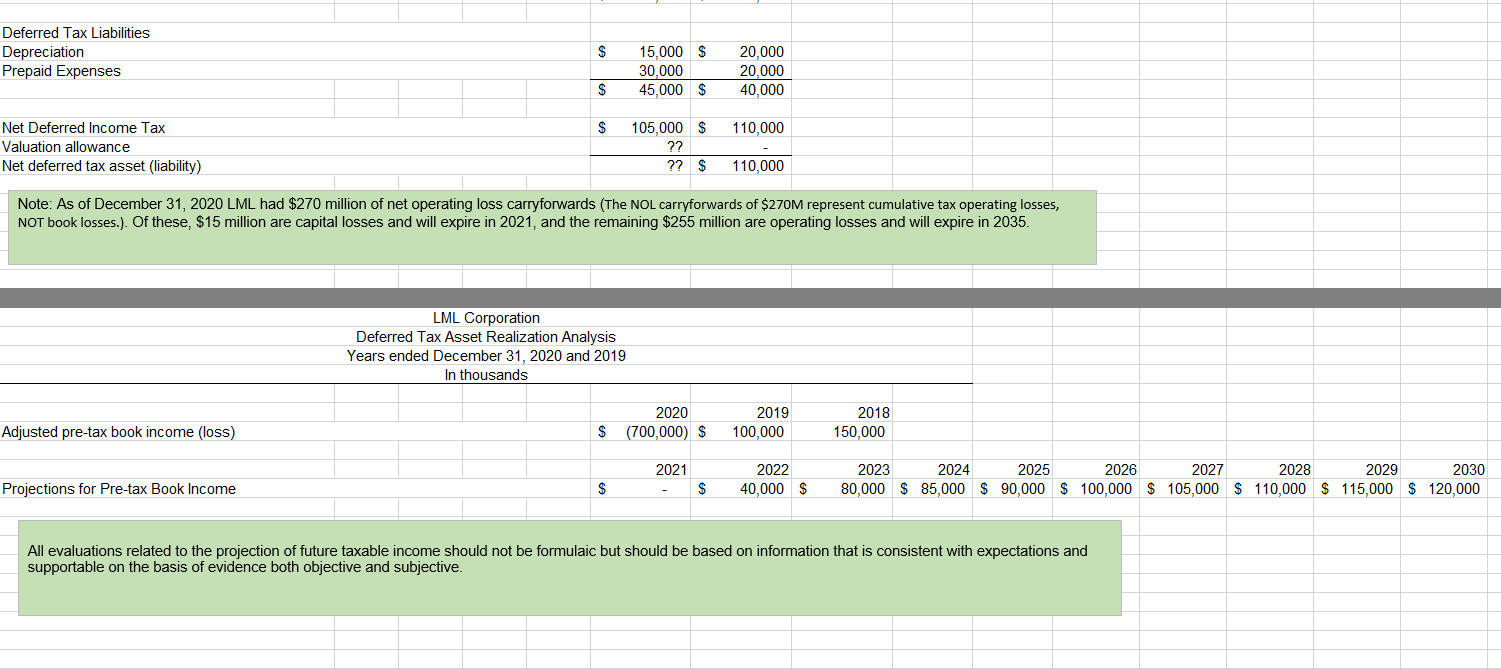

Because Valuation Allowances are primarily a judgement call this assignment will focus simply on making that decision. We want you to practice exing some professional judgement. There are a range of possmle conclusions that would be considered "correct " LML has lost a large customer. in this case we'll analyze what Impact that may have. Note: in this pan of the case do not wony about Including the evaluation of state jurisdictions we Will con5ider the federal jurisdiction only. In addition to the facts below - The projected income schedule (realization analysis below) projects organic growth beginning in & after stemming the decrease in pretax book income. A Signicant customer declared bankantcy in w; therefore, the Company wrote off all accounts receivable from this customer and saw a considerable decline in revenue directly related to the customer loss The Company is considering the exclusion of such expense when evaluating whether future income is objectively veriable The Company does not have a history of operating losses or tax credit carryfowvards expiring unused. - The Company has identied the following posSibIe tax-planning strategies. o Selling and leasing back manufacturing equipment that would result in a taxable gain of $20 million 0 Selling the primary manufacturing facnity at a gain to otfset existing capital loss carryforwards. Requirement 1 According to ABC 740, what are the four sources of taxable income? Operating Income - Income gernated from the comapny's primary bUSiness actVilies. Capital gains -lncome gerated from the sale of capital assetsI such as property or investments. Taxable income from pass through entites-lncome genrated from partnerships, s corporations and other entities that pass their income through to their oweners Taxable income from foreign source income gemated from foreign source that is subject to US. taxation Requirement 2. How much of the reversing taxable temporary differences (DTLs) may be considered in estimating future taxable income? According to A80 740, only the amount reversing the taxable temporary difference (DTLs) that is more likely than not to be relized maybe considered in eISimating fututre taxable income This meant that if it is more likly not that DTL will not reverse in the futurei it cannot be incldued in the estimated of futre taxable income. Requirement 3' In evaluating the income that LML is projecting to future operations. is LML in a cumulative loss position (assuming LML considers the current year + prior two years)? Requirement 4: In evaluating the income that LML is projecting related to future operations: the company has prOjected growth in future projections. Does the evidence of historic losses affect our ability to accept the company's estimate of future growth? Requirement 5: What other positive or negative evidence do you see in LML's facts that should be considered in the VA discussion? Requirement 6 In your opinion is there enough eVidence to justify that LML record a valuation allowance? If so, for how much? Create the conesponding joun'ial entry? LML Corporation Consolidated Statement of Operations - Years ended December 31, 2020, 2019 and 2018 ' In thousands 2020 2010 2018 Revenues, Net $ 1,250,000 3 1,900,000 3 1,800,000 Cost of Goods Sold 1,400,000 1,250,000 1,200,000 Gross Profit (150,000) 650,000 600,000 Selling, General and Administrative Expense 500,000 500,000 400,000 Operating income (loss) (650,000) 150,000 200,000 - Interest Expense, net 50,000 50,000 50,000 ' Income (loss) before provision for income taxes (?00,000} 100,000 150,000 . Income tax expense (benefit) ?? 36 000 54 000 -Net(loss)income ?? 3 64,000 3 LIv'IL Corporation Inventory of Deferred Tax Balances Years ended December 31, 2020 and 2019 In thousands 90,000 - 2020 2010 ' Deferred Tax Assets . Allowance for Doubtful Accounts $ 30,000 3 25,000 - Tax Loss Carrvforwards 100,000 100,000 Accruals and other 20 000 25 000 12_ $ 150,000 3 150,000 Deferred Tax Liabilities Depreciation 15,000 $ 20,000 Prepaid Expenses 30,000 20,000 $ 45,000 $ 40,000 Net Deferred Income Tax $ 105,000 $ 110,000 Valuation allowance ?? Net deferred tax asset (liability) ?? $ 110,000 Note: As of December 31, 2020 LML had $270 million of net operating loss carryforwards (The NOL carryforwards of $270M represent cumulative tax operating losses, NOT book losses.). Of these, $15 million are capital losses and will expire in 2021, and the remaining $255 million are operating losses and will expire in 2035. LML Corporation Deferred Tax Asset Realization Analysis Years ended December 31, 2020 and 2019 In thousands 2020 2019 2018 Adjusted pre-tax book income (loss) $ (700,000) $ 100,000 150,000 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 Projections for Pre-tax Book Income $ $ 40,000 $ 80,000 $ 85,000 $ 90,000 $ 100,000 $ 105,000 $ 110,000 $ 115,000 $ 120,000 All evaluations related to the projection of future taxable income should not be formulaic but should be based on information that is consistent with expectations and supportable on the basis of evidence both objective and subjective

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!