Below are the separate statements of financial position of Ghana Ltd and its two investee companies...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

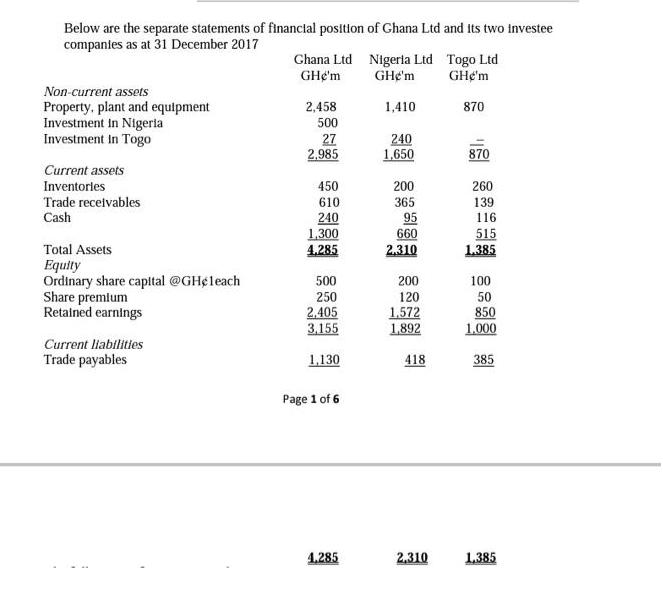

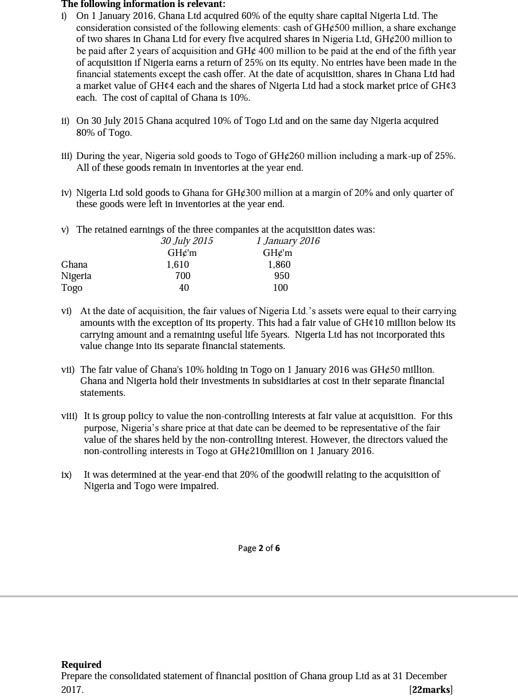

Below are the separate statements of financial position of Ghana Ltd and its two investee companies as at 31 December 2017 Non-current assets Property, plant and equipment Investment in Nigeria Investment in Togo Current assets Inventories Trade receivables Cash Total Assets Equity Ordinary share capital @GHcleach Share premium Retained earnings Current liabilities Trade payables Ghana Ltd GHe'm 2,458 500 27 2,985 450 610 240 1,300 4.285 500 250 2,405 3,155 1,130 Page 1 of 6 4.285 Nigeria Ltd GHe'm 1,410 240 1,650 200 365 95 660 2.310 200 120 1,572 1,892 418 2.310 Togo Ltd GHç'm 870 870 260 139 116 515 1.385 100 50 850 1,000 385 1.385 The following information is relevant: 1) On 1 January 2016, Ghana Ltd acquired 60% of the equity share capital Nigeria Ltd. The consideration consisted of the following elements: cash of GH¢500 million, a share exchange of two shares in Chana Ltd for every five acquired shares in Nigeria Ltd, GHe200 million to be paid after 2 years of acquisition and GHe 400 million to be paid at the end of the fifth year of acquisition if Nigeria earns a return of 25% on Its equity. No entries have been made in the financial statements except the cash offer. At the date of acquisition, shares in Ghana Ltd had a market value of GHC4 each and the shares of Nigeria Ltd had a stock market price of GH¢3 each. The cost of capital of Ghana is 10%. 11) On 30 July 2015 Ghana acquired 10% of Togo Ltd and on the same day Nigeria acquired 80% of Togo. III) During the year, Nigeria sold goods to Togo of GHe260 million including a mark-up of 25%. All of these goods remain in Inventories at the year end. Iv) Nigerta Ltd sold goods to Ghana for GH 300 million at a margin of 20% and only quarter of these goods were left in Inventories at the year end. v) The retained earnings of the three companies at the acquisition dates was: 30 July 2015 1 January 2016 GHe'm GHe'm 1,610 Ghana Nigeria Togo 700 40 1,860 950 100 VI) At the date of acquisition, the fair values of Nigeria Ltd.'s assets were equal to their carrying amounts with the exception of its property. This had a fair value of GH¢ 10 million below its carrying amount and a remaining useful life 5years. Nigeria Ltd has not incorporated this value change into its separate financial statements. vil) The fair value of Ghana's 10% holding in Togo on 1 January 2016 was GH₂50 million. Chana and Nigeria hold their investments in subsidiaries at cost in their separate financial statements. VIII) It is group policy to value the non-controlling interests at fair value at acquisition. For this purpose, Nigeria's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling Interest. However, the directors valued the non-controlling interests in Togo at GHe210million on 1 January 2016. Ix) It was determined at the year-end that 20% of the goodwill relating to the acquisition of Nigeria and Togo were impaired. Page 2 of 6 Required Prepare the consolidated statement of financial position of Chana group Ltd as at 31 December 2017. [22marks] Below are the separate statements of financial position of Ghana Ltd and its two investee companies as at 31 December 2017 Non-current assets Property, plant and equipment Investment in Nigeria Investment in Togo Current assets Inventories Trade receivables Cash Total Assets Equity Ordinary share capital @GHcleach Share premium Retained earnings Current liabilities Trade payables Ghana Ltd GHe'm 2,458 500 27 2,985 450 610 240 1,300 4.285 500 250 2,405 3,155 1,130 Page 1 of 6 4.285 Nigeria Ltd GHe'm 1,410 240 1,650 200 365 95 660 2.310 200 120 1,572 1,892 418 2.310 Togo Ltd GHç'm 870 870 260 139 116 515 1.385 100 50 850 1,000 385 1.385 The following information is relevant: 1) On 1 January 2016, Ghana Ltd acquired 60% of the equity share capital Nigeria Ltd. The consideration consisted of the following elements: cash of GH¢500 million, a share exchange of two shares in Chana Ltd for every five acquired shares in Nigeria Ltd, GHe200 million to be paid after 2 years of acquisition and GHe 400 million to be paid at the end of the fifth year of acquisition if Nigeria earns a return of 25% on Its equity. No entries have been made in the financial statements except the cash offer. At the date of acquisition, shares in Ghana Ltd had a market value of GHC4 each and the shares of Nigeria Ltd had a stock market price of GH¢3 each. The cost of capital of Ghana is 10%. 11) On 30 July 2015 Ghana acquired 10% of Togo Ltd and on the same day Nigeria acquired 80% of Togo. III) During the year, Nigeria sold goods to Togo of GHe260 million including a mark-up of 25%. All of these goods remain in Inventories at the year end. Iv) Nigerta Ltd sold goods to Ghana for GH 300 million at a margin of 20% and only quarter of these goods were left in Inventories at the year end. v) The retained earnings of the three companies at the acquisition dates was: 30 July 2015 1 January 2016 GHe'm GHe'm 1,610 Ghana Nigeria Togo 700 40 1,860 950 100 VI) At the date of acquisition, the fair values of Nigeria Ltd.'s assets were equal to their carrying amounts with the exception of its property. This had a fair value of GH¢ 10 million below its carrying amount and a remaining useful life 5years. Nigeria Ltd has not incorporated this value change into its separate financial statements. vil) The fair value of Ghana's 10% holding in Togo on 1 January 2016 was GH₂50 million. Chana and Nigeria hold their investments in subsidiaries at cost in their separate financial statements. VIII) It is group policy to value the non-controlling interests at fair value at acquisition. For this purpose, Nigeria's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling Interest. However, the directors valued the non-controlling interests in Togo at GHe210million on 1 January 2016. Ix) It was determined at the year-end that 20% of the goodwill relating to the acquisition of Nigeria and Togo were impaired. Page 2 of 6 Required Prepare the consolidated statement of financial position of Chana group Ltd as at 31 December 2017. [22marks]

Expert Answer:

Answer rating: 100% (QA)

ANSWER Consolidated Statement of Financial Position of Ghana Group Ltd as at 31 December 2017 Ghana ... View the full answer

Related Book For

International Financial Reporting A Practical Guide

ISBN: 978-1292200743

6th edition

Authors: Alan Melville

Posted Date:

Students also viewed these accounting questions

-

Below are the comparative statements of financial position for Lowenstein Corporation. Dividends in the amount of $10,000 were declared and paid in 2019. Instructions From this information, prepare a...

-

As at 31 December 2019, Portal Development Limited (PD) has trade receivables of HK$20,000,000 overdue for more than one year. After some rounds of tough negotiation with the auditor, PD finally...

-

The comparative statements of financial position for Sergipe Company show these changes in non-cash current asset accounts: accounts receivable decrease R$80.000, prepaid expenses increase R$28,000,...

-

What is a random variable? What is a discrete random variable? What is a continuous random variable? Give some examples of discrete random variables.

-

A partnership is currently holding $400,000 in assets and $234,000 in liabilities. The partnership is to be liquidated, and $20,000 is the best estimation of the expenses that will be incurred during...

-

Expand using logarithmic properties. Where possible, evaluate logarithmic expressions. logs xy 125

-

Look back at Table 5.3. What type of correlation coefficient would you use to examine the relationship between ethnicity (defined as different categories) and political affiliation (defined as...

-

Sidney Industries manufactures a variety of custom products. The company has traditionally used a plantwide manufacturing overhead rate based on machine hours to allocate manufacturing overhead...

-

Hypothetically, let's say the New York Jets believe that the injury to Aaron Rodgers constituted a career ending injury pursuant to an exit clause in the contract and Aaron Rodgers argued that his...

-

Use mesh analysis to find ix in Fig. 13.80, Where is = 4 cos(600t) A and vs = 110 cos(600t + 30º) 12 F 150 800 mH 600 mH

-

Calculate heating rate (BTU/kWh) for the Energy Center based on provided materials: HP Pressure to STG 1742 Psi HP Final Steam Temperature 991 Fahrenheit Cold Reheat Pressure 451 Psi Cold Reheat...

-

Part I: Reflection Reflect on your use of the Big6 Research Model (CO2). What step was the most challenging? How did you overcome the challenge? Using the steps in the Big 6 Research Model, consider...

-

Matthias Corp. had the following foreign currency transactions during 2020: Purchased merchandise from a foreign supplier on January 20 for the U.S. dollar equivalent of $63,100 and paid the invoice...

-

Suppose the expected return for the general market is 7% and the risk premium in the market is 10%. If the required rate of return for a particular stock is 12% then what is the Beta of the stock?...

-

Aluminum costs $1.417 per pound. If aluminum's density is 2.70g/cm3, how much does 3.0997 cubic feet cost? Record answer to the nearest hundredth place.

-

7) A coil with 60 turns is wrapped around a square frame with an area of 0.15 m. The coil is immersed inside a magnetic field that changes at the rate of 0.5 T/s. What is the induced emf in the coil?

-

Education and educators consistently reference data-driven decisions. Schools leverage student data to drive curriculum and instructional decisions. It is important to support a campus culture where...

-

Problem 3.5 (4 points). We will prove, in steps, that rank (L) = rank(LT) for any LE Rnxm (a) Prove that rank (L) = rank (LTL). (Hint: use Problem 3.4.) (b) Use part (a) to deduce that that rank(L) =...

-

A company has purchased the following intangible assets in separate transactions: (a) A patent which expires after ten years; the company expects to make use of this patent for six years and then...

-

(a) Define the term "property, plant and equipment". (b) When should an item of property, plant and equipment be recognised as an asset and when should it be derecognised? (c) Which of the following...

-

On 1 May 2017, a company which prepares financial statements to 30 April each year issues 750,000 of 3% loan stock at a discount of 5%. Issue costs are 13,175. Interest is payable on 30 April each...

-

At the beginning of April one year, the silver forward prices (in cents per troy ounce) were as follows: The carrying cost of silver is about 20 cents per ounce per year, paid at the beginning of...

-

Suppose that a forward contract on an asset is written at time zero and there are \(M\) periods until delivery. Suppose that the proportional carrying charge in period \(k\) is \(q S(k)\), where...

-

The current price of gold is \(\$ 412\) per ounce. The storage cost is \(\$ 2\) per ounce per year, payable quarterly in advance. Assuming a constant interest rate of \(9 \%\) compounded quarterly,...

Study smarter with the SolutionInn App