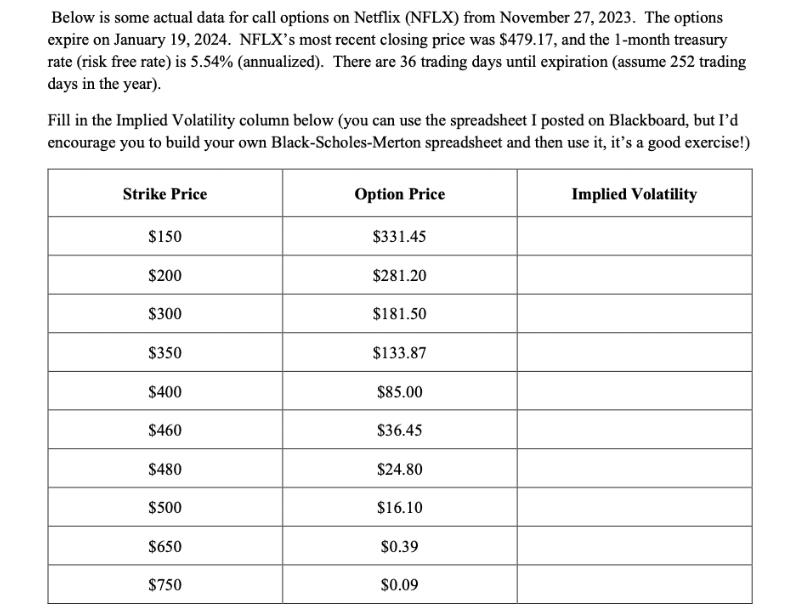

Below is some actual data for call options on Netflix (NFLX) from November 27, 2023. The...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: