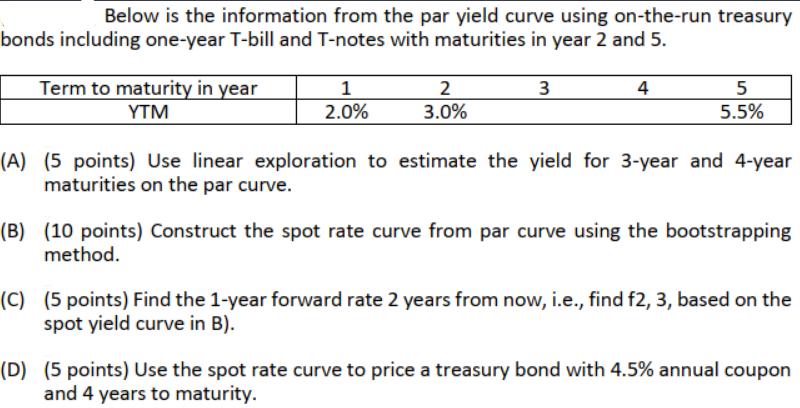

Question: Below is the information from the par yield curve using on-the-run treasury bonds including one-year T-bill and T-notes with maturities in year 2 and

Below is the information from the par yield curve using on-the-run treasury bonds including one-year T-bill and T-notes with maturities in year 2 and 5. 3 Term to maturity in year YTM 1 2.0% 2 3.0% 4 5 5.5% (A) (5 points) Use linear exploration to estimate the yield for 3-year and 4-year maturities on the par curve. (B) (10 points) Construct the spot rate curve from par curve using the bootstrapping method. (C) (5 points) Find the 1-year forward rate 2 years from now, i.e., find f2, 3, based on the spot yield curve in B). (D) (5 points) Use the spot rate curve to price a treasury bond with 4.5% annual coupon and 4 years to maturity.

Step by Step Solution

3.52 Rating (155 Votes )

There are 3 Steps involved in it

Based on the information youve provided you have the yields to maturity YTM for ontherun Treasury bonds with maturities of 1 year 2 years and 5 years Heres a summary of the yields 1year Tbill 20 YTM 2... View full answer

Get step-by-step solutions from verified subject matter experts