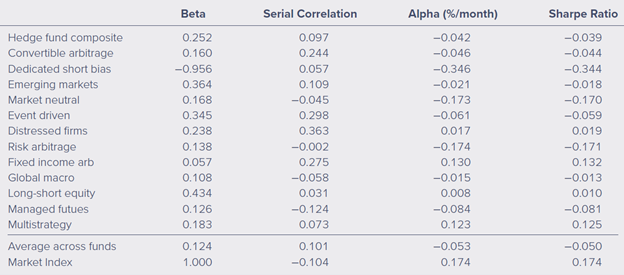

Question: Beta Serial Correlation Alpha (%/month) Sharpe Ratio Hedge fund composite 0.252 0.097 -0.042 -0.039 Convertible arbitrage 0.160 0.244 -0.046 -0.044 Dedicated short bias -0.956 0.057

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock