Question: BLANKS For Helen: 1. Single payment OR Installment 2. made the best use of the rental money OR didn't want to write a lot of

BLANKS For Helen:

BLANKS For Helen:

1. Single payment OR Installment

2. made the best use of the rental money OR didn't want to write a lot of checks

BLANKS For Gabe

1. Single payment OR Installment

2. He doesnt want to keep track of multiple payments OR he can surely pay of the loan

CARL

1. Fixed or variable rate

2. were subject to change or NOT subjected to change

Jeff

1. Fixed or variable rate

2. Interest rates were holding steady or long term probably assured a variable rate

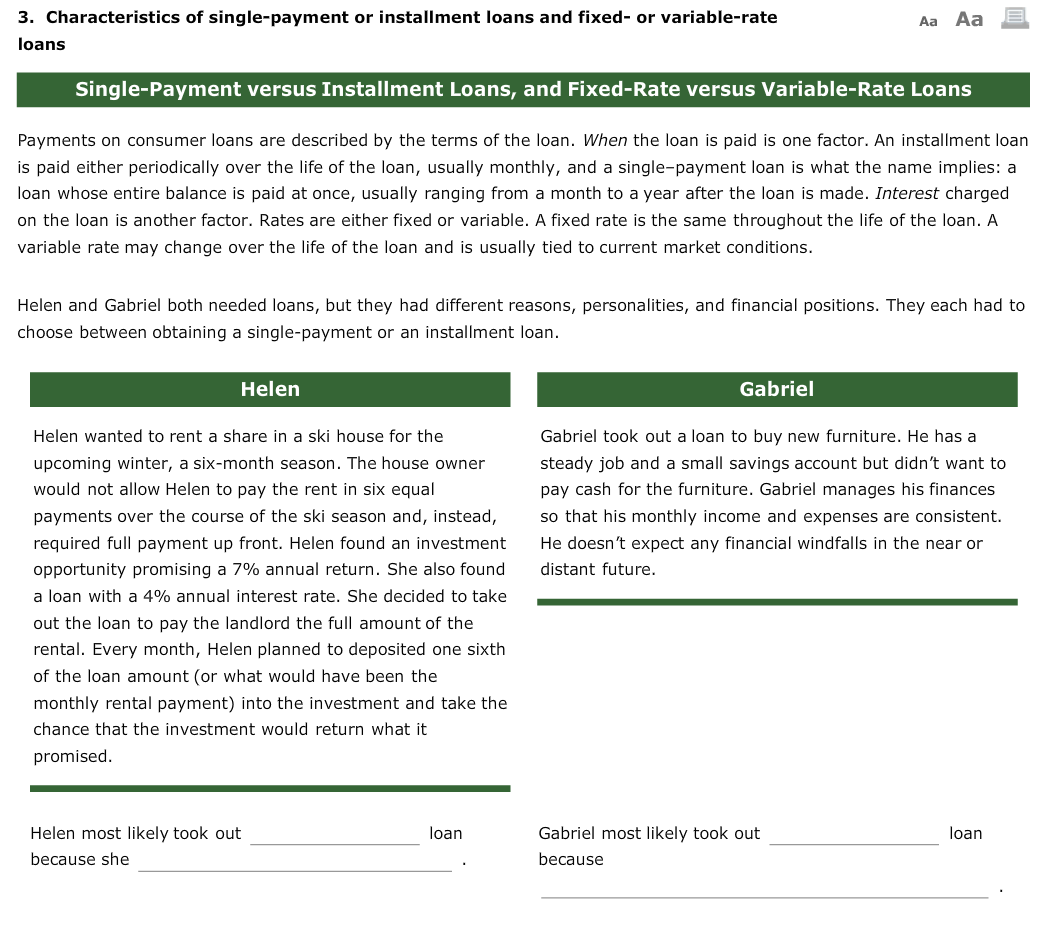

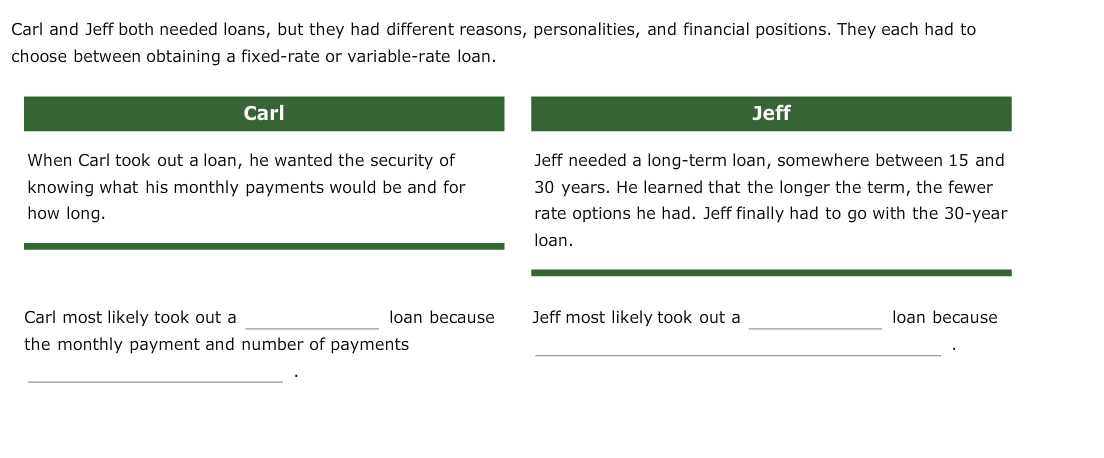

3. Characteristics of single-payment or installment loans and fixed- or variable-rate loans Aa Aa E Single-Payment versus Installment Loans, and Fixed-Rate versus Variable-Rate Loans Payments on consumer loans are described by the terms of the loan. When the loan is paid is one factor. An installment loan is paid either periodically over the life of the loan, usually monthly, and a single-payment loan is what the name implies: a loan whose entire balance is paid at once, usually ranging from a month to a year after the loan is made. Interest charged on the loan is another factor. Rates are either fixed or variable. A fixed rate is the same throughout the life of the loan. A variable rate may change over the life of the loan and is usually tied to current market conditions. Helen and Gabriel both needed loans, but they had different reasons, personalities, and financial positions. They each had to choose between obtaining a single-payment or an installment loan. Helen Gabriel Gabriel took out a loan to buy new furniture. He has a steady job and a small savings account but didn't want to pay cash for the furniture. Gabriel manages his finances so that his monthly income and expenses are consistent. He doesn't expect any financial windfalls in the near or distant future. Helen wanted to rent a share in a ski house for the upcoming winter, a six-month season. The house owner would not allow Helen to pay the rent in six equal payments over the course of the ski season and, instead, required full payment up front. Helen found an investment opportunity promising a 7% annual return. She also found a loan with a 4% annual interest rate. She decided to take out the loan to pay the landlord the full amount of the rental. Every month, Helen planned to deposited one sixth of the loan amount (or what would have been the monthly rental payment) into the investment and take the chance that the investment would return what it promised. loan loan Helen most likely took out because she Gabriel most likely took out because Carl and Jeff both needed loans, but they had different reasons, personalities, and financial positions. They each had to choose between obtaining a fixed-rate or variable-rate loan. Carl Jeff When Carl took out a loan, he wanted the security of knowing what his monthly payments would be and for how long. Jeff needed a long-term loan, somewhere between 15 and 30 years. He learned that the longer the term, the fewer rate options he had. Jeff finally had to go with the 30-year loan. Jeff most likely took out a loan because Carl most likely took out a loan because the monthly payment and number of payments 3. Characteristics of single-payment or installment loans and fixed- or variable-rate loans Aa Aa E Single-Payment versus Installment Loans, and Fixed-Rate versus Variable-Rate Loans Payments on consumer loans are described by the terms of the loan. When the loan is paid is one factor. An installment loan is paid either periodically over the life of the loan, usually monthly, and a single-payment loan is what the name implies: a loan whose entire balance is paid at once, usually ranging from a month to a year after the loan is made. Interest charged on the loan is another factor. Rates are either fixed or variable. A fixed rate is the same throughout the life of the loan. A variable rate may change over the life of the loan and is usually tied to current market conditions. Helen and Gabriel both needed loans, but they had different reasons, personalities, and financial positions. They each had to choose between obtaining a single-payment or an installment loan. Helen Gabriel Gabriel took out a loan to buy new furniture. He has a steady job and a small savings account but didn't want to pay cash for the furniture. Gabriel manages his finances so that his monthly income and expenses are consistent. He doesn't expect any financial windfalls in the near or distant future. Helen wanted to rent a share in a ski house for the upcoming winter, a six-month season. The house owner would not allow Helen to pay the rent in six equal payments over the course of the ski season and, instead, required full payment up front. Helen found an investment opportunity promising a 7% annual return. She also found a loan with a 4% annual interest rate. She decided to take out the loan to pay the landlord the full amount of the rental. Every month, Helen planned to deposited one sixth of the loan amount (or what would have been the monthly rental payment) into the investment and take the chance that the investment would return what it promised. loan loan Helen most likely took out because she Gabriel most likely took out because Carl and Jeff both needed loans, but they had different reasons, personalities, and financial positions. They each had to choose between obtaining a fixed-rate or variable-rate loan. Carl Jeff When Carl took out a loan, he wanted the security of knowing what his monthly payments would be and for how long. Jeff needed a long-term loan, somewhere between 15 and 30 years. He learned that the longer the term, the fewer rate options he had. Jeff finally had to go with the 30-year loan. Jeff most likely took out a loan because Carl most likely took out a loan because the monthly payment and number of payments

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts