Question: Blueprint Problem: Direct materials variance Materials Variance Analysis Variance analysis is used as a performance evaluation measure for responsible managers. Materials variance occurs when the

Blueprint Problem: Direct materials variance

Materials Variance Analysis

Variance analysis is used as a performance evaluation measure for responsible managers. Materials variance occurs when the cost of materials or the amount of materials used for actual output deviates from what was initially planned by company management for a given period of time or for a specific amount of production. Materials variance analysis is conducted by comparing the standard materials cost for production with the actual materials cost incurred for the actual production quantity of the product.

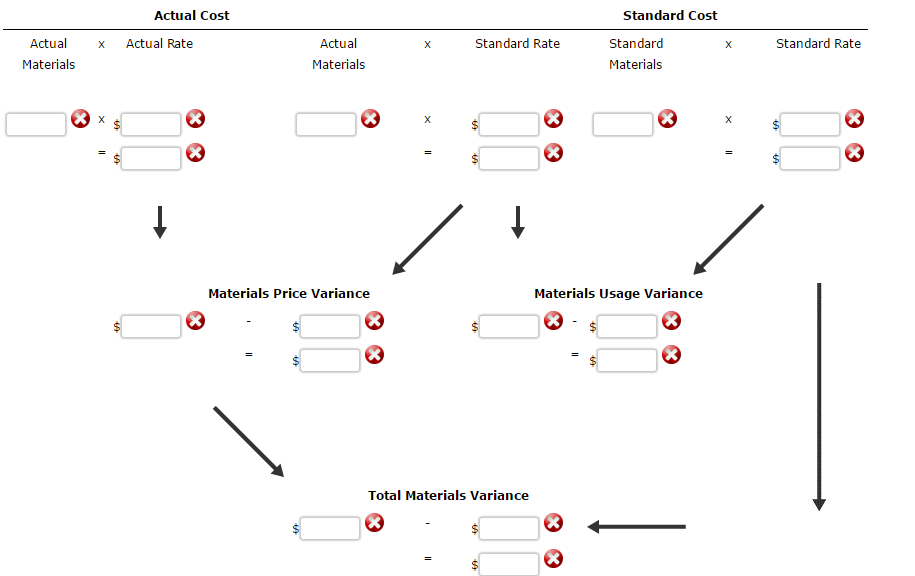

There are two parts to materials variance analysis. The first is a comparison of the standard cost per unit of materials with the actual cost per unit of materials, which results in the determination of the materials price variance. The second is a comparison of the standard quantity of use of units of materials with the actual quantity of use of units of materials for the actual production completed, which results in the determination of the materials (or quantity) variance.

Materials Price Variance

This type of variance is concerned with the difference between what was paid for materials and what should have been paid for materials used in production.

Which of the following activities are possible causes of materials price variance? Select "Yes" for all that apply.

Materials Usage Variance

This type of variance is concerned with the difference between materials used and materials that should have been used for the actual output.

Which of the following activities are possible causes of materials price variance? Select "Yes" for all that apply.

Gauging the Favorableness of Variances

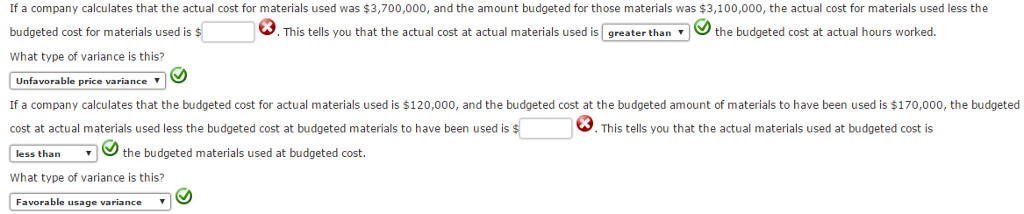

When variances occur, they are described as being either favorable or unfavorable. When actual activity consumes more time or money than initially planned, an unfavorable variance exists. However, when actual activity consumes less time or money than initially planned, a favorable variance exists. Note that the terms favorable and unfavorable are used, rather than saying that a variance is good or bad, because until the cause of a variance is discovered, it is not clear whether a variance is either good or bad.

Note: Use the minus sign to indicate negative values (when the budgeted amount is greater than the actual).

APPLY THE CONCEPTS: Conduct the Materials Variance Analysis

Complete the following graphic to compute the direct materials price variance, the direct materials usage variance, and the total materials variance for your shoe-making business. When required, enter the rates as dollars and cents. If required, use the minus sign to indicate a negative value.

1. Using lower-quality materials than planned 2. Using higher-quality materials than planned 3. Unexpected quantity discounts Yes Yes Yes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts