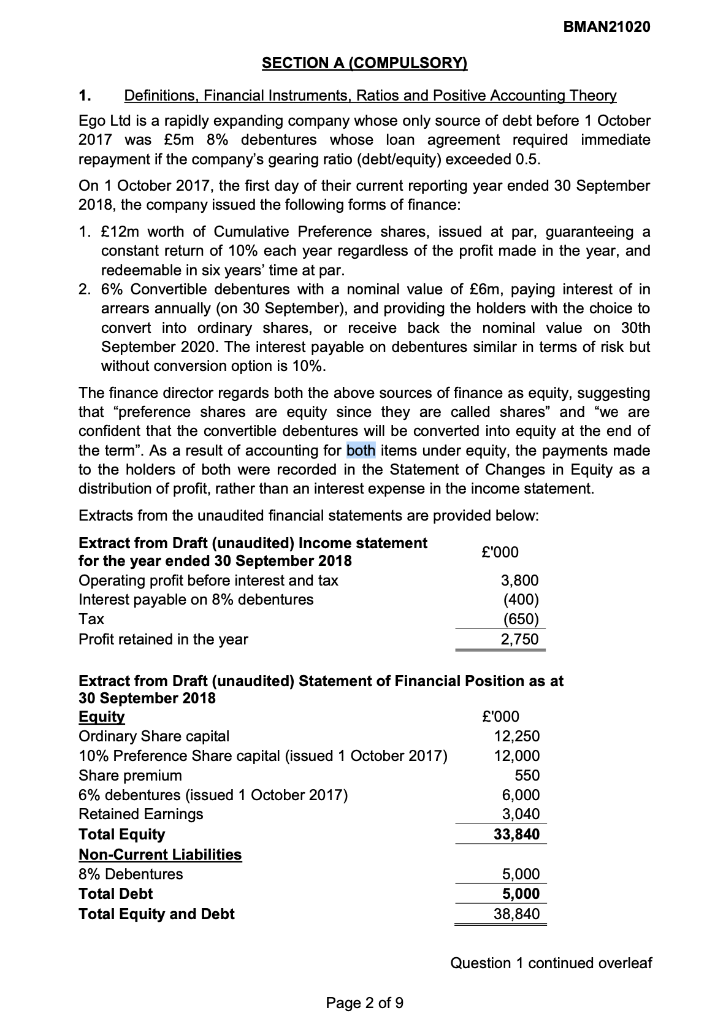

Question: BMAN21020 SECTION A (COMPULSORY) 1. Definitions, Financial Instruments, Ratios and Positive Accounting Theory Ego Ltd is a rapidly expanding company whose only source of debt

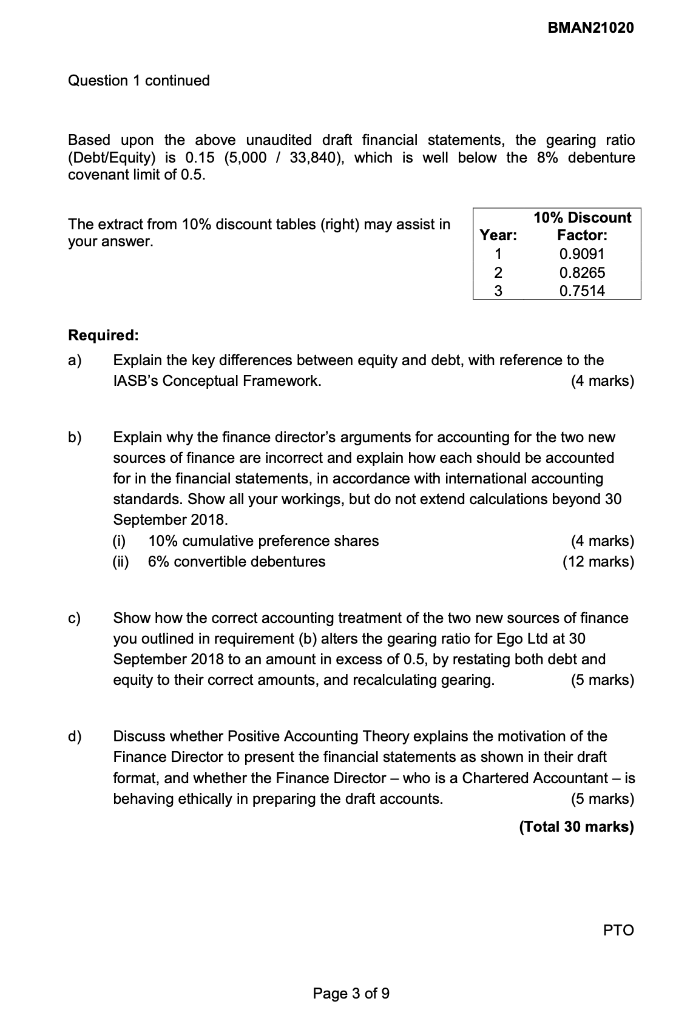

BMAN21020 SECTION A (COMPULSORY) 1. Definitions, Financial Instruments, Ratios and Positive Accounting Theory Ego Ltd is a rapidly expanding company whose only source of debt before 1 October 2017 was 5m 8% debentures whose loan agreement required immediate repayment if the company's gearing ratio (debt/equity) exceeded 0.5. On 1 October 2017, the first day of their current reporting year ended 30 September 2018, the company issued the following forms of finance: 1. 12m worth of Cumulative Preference shares, issued at par, guaranteeing a constant return of 10% each year regardless of the profit made in the year, and redeemable in six years' time at par. 2. 6% Convertible debentures with a nominal value of 6m, paying interest of in arrears annually (on 30 September), and providing the holders with the choice to convert into ordinary shares, or receive back the nominal value on 30th September 2020. The interest payable on debentures similar in terms of risk but without conversion option is 10%. The finance director regards both the above sources of finance as equity, suggesting that preference shares are equity since they are called shares" and "we are confident that the convertible debentures will be converted into equity at the end of the term". As a result of accounting for both items under equity, the payments made to the holders of both were recorded in the Statement of Changes in Equity as a distribution of profit, rather than an interest expense in the income statement. Extracts from the unaudited financial statements are provided below: Extract from Draft (unaudited) Income statement '000 for the year ended 30 September 2018 Operating profit before interest and tax 3,800 Interest payable on 8% debentures (400) Tax (650) Profit retained in the year 2,750 Extract from Draft (unaudited) Statement of Financial Position as at 30 September 2018 Equity '000 Ordinary Share capital 12,250 10% Preference Share capital (issued 1 October 2017) 12,000 Share premium 550 6% debentures (issued 1 October 2017) 6,000 Retained Earnings 3,040 Total Equity 33,840 Non-Current Liabilities 8% Debentures 5,000 Total Debt 5,000 Total Equity and Debt 38,840 Question 1 continued overleaf Page 2 of 9 BMAN21020 Question 1 continued Based upon the above unaudited draft financial statements, the gearing ratio (Debt/Equity) is 0.15 (5,000 / 33,840), which is well below the 8% debenture covenant limit of 0.5. The extract from 10% discount tables (right) may assist in your answer. Year: 1 2 3 10% Discount Factor: 0.9091 0.8265 0.7514 Required: a) Explain the key differences between equity and debt, with reference to the IASB's Conceptual Framework. (4 marks) b) Explain why the finance director's arguments for accounting for the two new sources of finance are incorrect and explain how each should be accounted for in the financial statements, in accordance with international accounting standards. Show all your workings, but do not extend calculations beyond 30 September 2018. (0) 10% cumulative preference shares (4 marks) (ii) 6% convertible debentures (12 marks) C) Show how the correct accounting treatment of the two new sources of finance you outlined in requirement (b) alters the gearing ratio for Ego Ltd at 30 September 2018 to an amount in excess of 0.5, by restating both debt and equity to their correct amounts, and recalculating gearing. (5 marks) d) Discuss whether Positive Accounting Theory explains the motivation of the Finance Director to present the financial statements as shown in their draft format, and whether the Finance Director - who is a Chartered Accountant - is behaving ethically in preparing the draft accounts. (5 marks) (Total 30 marks) PTO Page 3 of 9 BMAN21020 SECTION A (COMPULSORY) 1. Definitions, Financial Instruments, Ratios and Positive Accounting Theory Ego Ltd is a rapidly expanding company whose only source of debt before 1 October 2017 was 5m 8% debentures whose loan agreement required immediate repayment if the company's gearing ratio (debt/equity) exceeded 0.5. On 1 October 2017, the first day of their current reporting year ended 30 September 2018, the company issued the following forms of finance: 1. 12m worth of Cumulative Preference shares, issued at par, guaranteeing a constant return of 10% each year regardless of the profit made in the year, and redeemable in six years' time at par. 2. 6% Convertible debentures with a nominal value of 6m, paying interest of in arrears annually (on 30 September), and providing the holders with the choice to convert into ordinary shares, or receive back the nominal value on 30th September 2020. The interest payable on debentures similar in terms of risk but without conversion option is 10%. The finance director regards both the above sources of finance as equity, suggesting that preference shares are equity since they are called shares" and "we are confident that the convertible debentures will be converted into equity at the end of the term". As a result of accounting for both items under equity, the payments made to the holders of both were recorded in the Statement of Changes in Equity as a distribution of profit, rather than an interest expense in the income statement. Extracts from the unaudited financial statements are provided below: Extract from Draft (unaudited) Income statement '000 for the year ended 30 September 2018 Operating profit before interest and tax 3,800 Interest payable on 8% debentures (400) Tax (650) Profit retained in the year 2,750 Extract from Draft (unaudited) Statement of Financial Position as at 30 September 2018 Equity '000 Ordinary Share capital 12,250 10% Preference Share capital (issued 1 October 2017) 12,000 Share premium 550 6% debentures (issued 1 October 2017) 6,000 Retained Earnings 3,040 Total Equity 33,840 Non-Current Liabilities 8% Debentures 5,000 Total Debt 5,000 Total Equity and Debt 38,840 Question 1 continued overleaf Page 2 of 9 BMAN21020 Question 1 continued Based upon the above unaudited draft financial statements, the gearing ratio (Debt/Equity) is 0.15 (5,000 / 33,840), which is well below the 8% debenture covenant limit of 0.5. The extract from 10% discount tables (right) may assist in your answer. Year: 1 2 3 10% Discount Factor: 0.9091 0.8265 0.7514 Required: a) Explain the key differences between equity and debt, with reference to the IASB's Conceptual Framework. (4 marks) b) Explain why the finance director's arguments for accounting for the two new sources of finance are incorrect and explain how each should be accounted for in the financial statements, in accordance with international accounting standards. Show all your workings, but do not extend calculations beyond 30 September 2018. (0) 10% cumulative preference shares (4 marks) (ii) 6% convertible debentures (12 marks) C) Show how the correct accounting treatment of the two new sources of finance you outlined in requirement (b) alters the gearing ratio for Ego Ltd at 30 September 2018 to an amount in excess of 0.5, by restating both debt and equity to their correct amounts, and recalculating gearing. (5 marks) d) Discuss whether Positive Accounting Theory explains the motivation of the Finance Director to present the financial statements as shown in their draft format, and whether the Finance Director - who is a Chartered Accountant - is behaving ethically in preparing the draft accounts. (5 marks) (Total 30 marks) PTO Page 3 of 9

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts