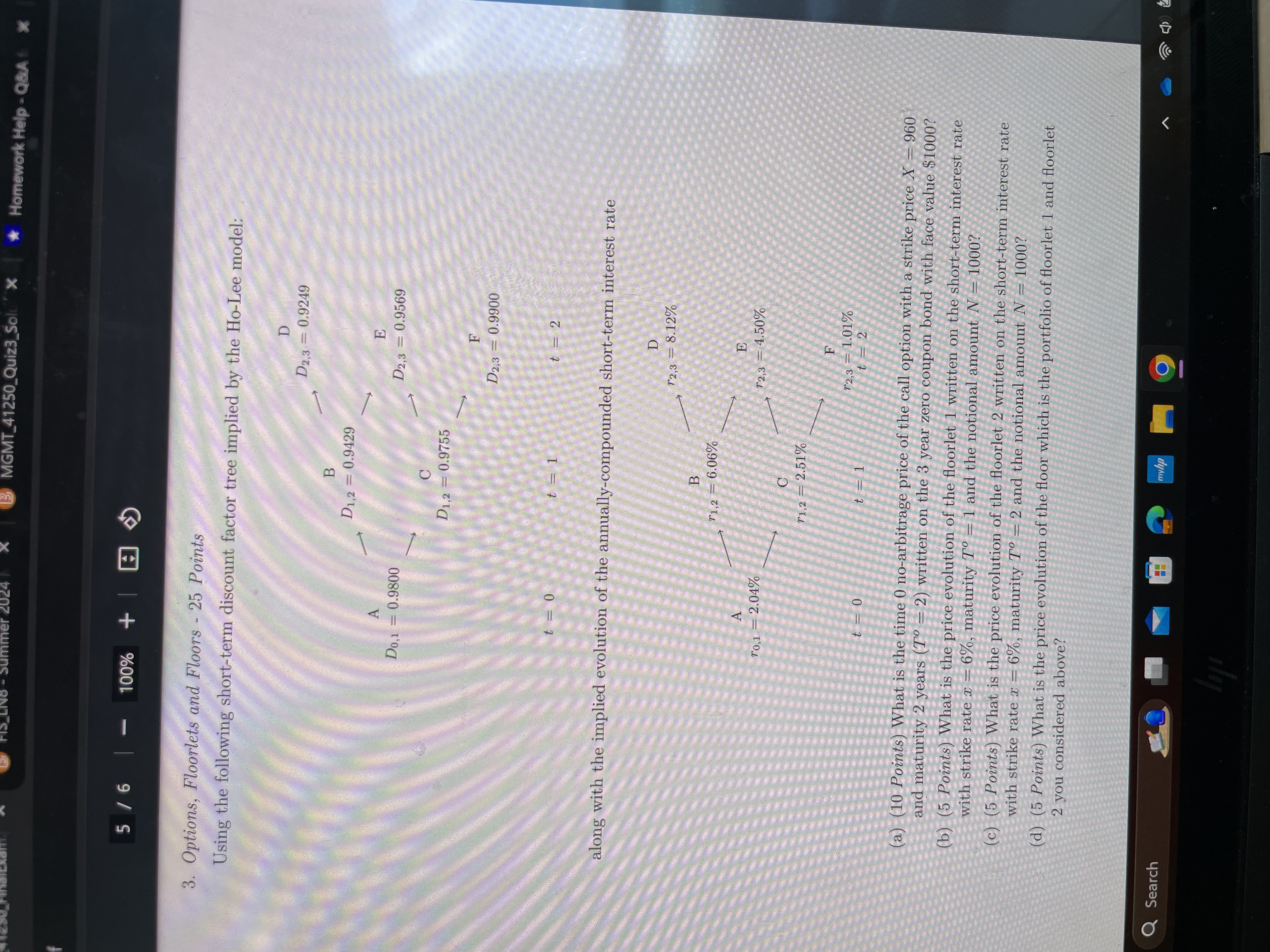

Question: BMGMT_41250_Quiz3_Sol X Homework Help - Q&A x 5/6 - 100% + 3. Options, Floorlets and Floors - 25 Points Using the following short-term discount factor

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock