Question: (Bond in the term structure, 20 points) Consider a 5-year, 7% coupon bond, paid annually, with a face value of $100 in a market

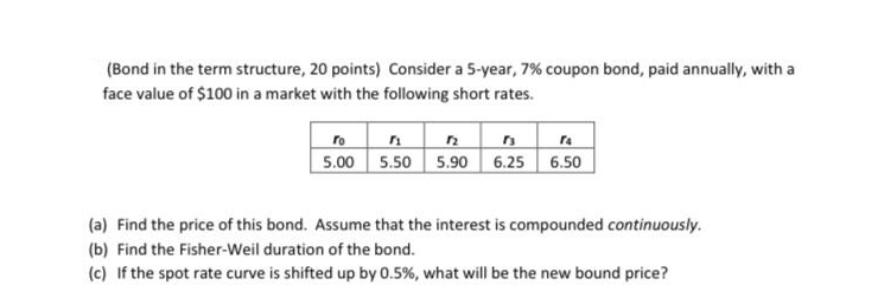

(Bond in the term structure, 20 points) Consider a 5-year, 7% coupon bond, paid annually, with a face value of $100 in a market with the following short rates. To n 5.00 5.50 5.90 6.25 6.50 (a) Find the price of this bond. Assume that the interest is compounded continuously. (b) Find the Fisher-Weil duration of the bond. (c) If the spot rate curve is shifted up by 0.5%, what will be the new bound price?

Step by Step Solution

3.38 Rating (151 Votes )

There are 3 Steps involved in it

To find the price of the bond we need to discount the future cash flows coupon payments and face val... View full answer

Get step-by-step solutions from verified subject matter experts