Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

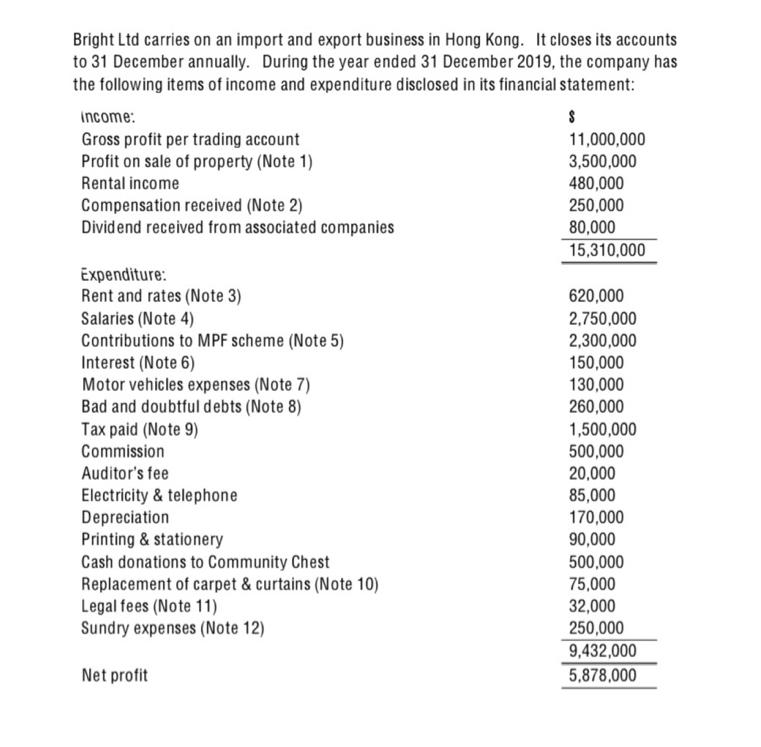

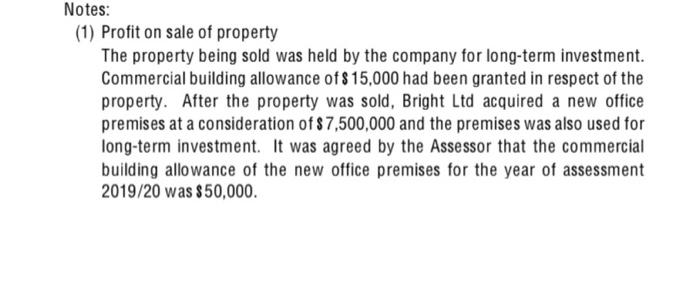

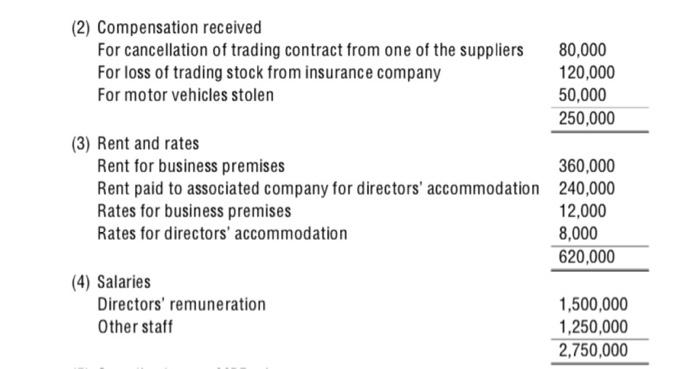

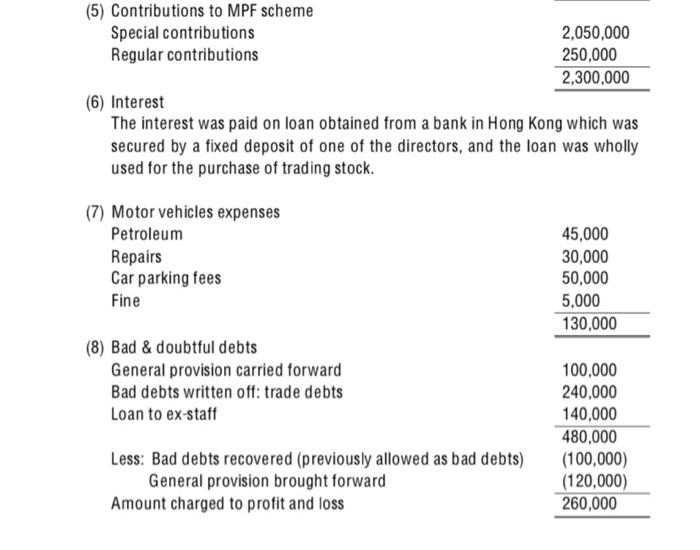

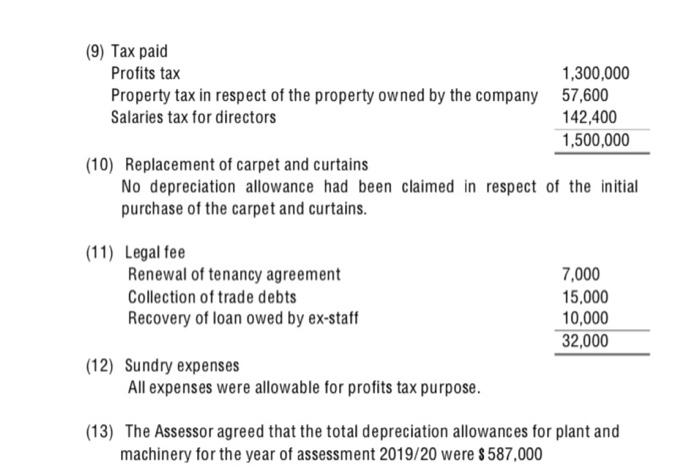

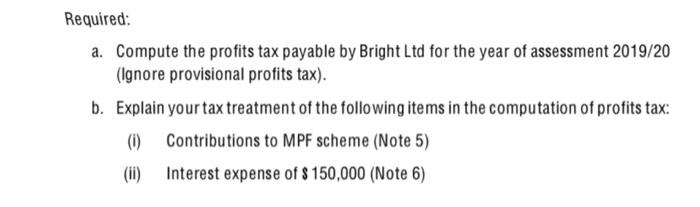

Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6) Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6) Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6) Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6)

Expert Answer:

Answer rating: 100% (QA)

Required Compute the profits tax payable by Bright Ltd for the year of assessment 201920 Ignore p... View the full answer

Related Book For

Advanced Accounting

ISBN: 978-0538480284

11th edition

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng

Posted Date:

Students also viewed these general management questions

-

During the year ended 30 June 2019 XYZ Pty Limited, a resident Australian private company (non BRE), received a franked dividend of $10,800 with $3,200 of attached franking credits. XYZ Pty Limited...

-

The Viking Corporation has the following items of income for 2016: Operating income ........................................................ $350,000 Dividend income (12%-owned corporations)...

-

During the year ended December 31, 2014, Bowersox International Corporation earned $ 3,500,000 in net income after taxes. The company reported $ 100,000 of net unrealized gains on available-for-sale...

-

Route Canal Shipping Company has the following schedule for aging of accounts receivable: AGE OF RECEIVABLES APRIL 30, 2001 a. Fill in column (4) for each month. b. If the firm had $1,440,000 in...

-

Determine the future worth for Problem 6. Should your company purchase the loader? In Problem 6, your company is looking at purchasing a loader at a cost of $125,000. The loader would have a useful...

-

"Snakeman" Jackson, as his friends call him, is an aging blues guitarist and songwriter. He frequently tours throughout Europe and South America. He requires tour promoters to pay him half of his fee...

-

Holze Music Co. issued 5\%, 10 -year bonds payable at 75 on December 31, 2006. At December 31, 2009, Holze reported the bonds payable as follows: Holze uses the straight-line amortization method....

-

An inexperienced accountant for Prestwick Company prepared the following income statement for the month of August 2015: Prepare a revised income statement in accordance with generally accepted...

-

Please use current tax rates, exemptions, and laws. Be sure to show ALL of your work so that I can give you partial credit. Use 2 0 2 3 tax law. Use these instructions: 2 0 2 3 Instruction 1 0 4 0 (...

-

Computer Project Exercises In developing the exercises, trade-offs had to be made to enrich the learning experience. One of the major problems students initially encounter is data and detail...

-

In Lake Serenity, there are two types of fish: Bass and Trout. The probability of catching a Bass is P(B) = 0.4, and the probability of catching a Trout is P(T) = 0.6. Additionally, it is known that...

-

When managers try to avoid hearsay and make decisions based on solid facts and information, this is known as ____________. (a) continuous improvement (b) evidence-based management (c) TQM (d) Theory...

-

What term is used to describe the worlds supply of natural resources, things like land, water, and minerals? (a) sustainable development (b) global warming (c) climate justice (d) environmental...

-

Work preferences of different generations and public values over things like high pay for corporate executives are examples of developments in the ____________ environment of organizations. (a) task...

-

The benefits of planning include __________. (a) improved focus (b) lower labour costs (c) more accurate forecasts (d) higher profits

-

It is ____________ when a foreign visitor takes offence at a local custom such as dining with ones fingers, considering it inferior to practices of his or her own culture. (a) universalist (b)...

-

Consider the circuit a 130 V 3 F 3 F C 4 F 4 F H b What is the equivalent capacitance for this network? Answer in units of F.

-

Suppose the market is semistrong form efficient. Can you expect to earn excess returns if you make trades based on? a. Your brokers information about record earnings for a stock? b. Rumors about a...

-

Refer to the preceding facts for Postmans acquisition of 80% of Spartans common stock and the bond transactions. Postman uses the simple equity method to account for its investment in Spartan. On...

-

On June 30, 2015, the shareholders equity of Fabinet, a foreign corporation, was 10,500,000 FC. At that time, Newcore, a U.S. corporation, acquired 40% in Fabinet by paying $3,120,000 when 1 FC was...

-

Company S has the following stockholders equity on January 1, 2015: Common stock ($1par, 100,000 shares) ............... $100,000 6%preferred stock ($100par, 2,000 shares ............. 200,000...

-

A healthy diet is becoming increasingly important for consumers, especially women aged 2535. As a result, they are taking active steps to ensure they are eating healthy but are also looking for other...

-

Lael was just hired by Best East Motels into their manager training program and was excited about the potential benefits after her graduation from Florida State University. Working part-time and...

-

Sophie just completed a sales training course with one of the firms most productive sales representatives, Emma. At the end of the first week, Sophie and Emma sat in a motel room filling out their...

Study smarter with the SolutionInn App