Question: c) Consider a putable bond that has 1 year to maturity, par value of 100 and a coupon rate of 4%, paid semi-annually. Assume that

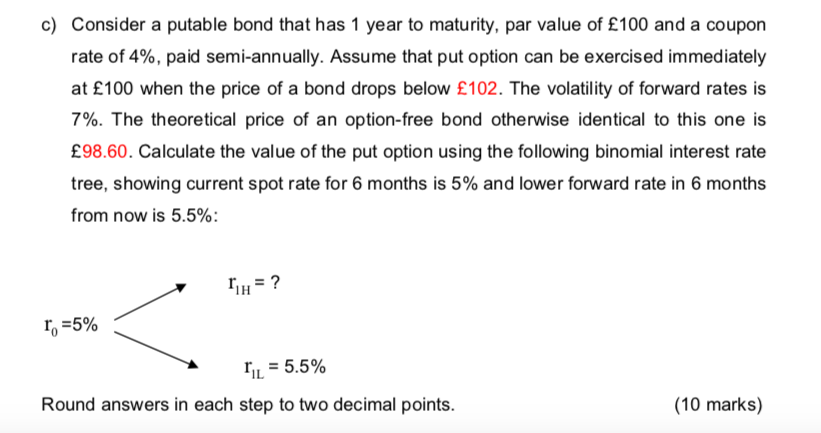

c) Consider a putable bond that has 1 year to maturity, par value of 100 and a coupon rate of 4%, paid semi-annually. Assume that put option can be exercised immediately at 100 when the price of a bond drops below 102. The volatility of forward rates is 7%. The theoretical price of an option-free bond otherwise identical to this one is 98.60. Calculate the value of the put option using the following binomial interest rate tree, showing current spot rate for 6 months is 5% and lower forward rate in 6 months from now is 5.5%; h"5% r,L-5.5% Round answers in each step to two decimal points. (10 marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock