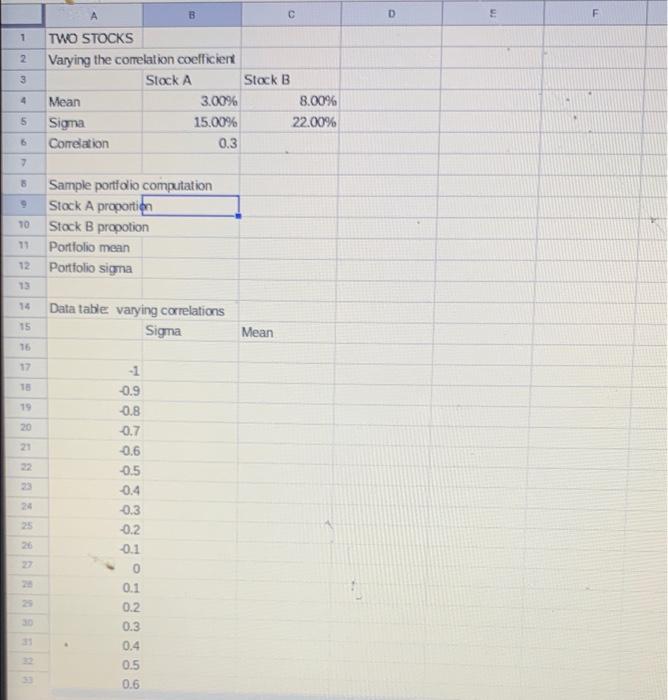

Question: C D E F 1 2 3 TWO STOCKS Varying the comelation coefficient Stock A Stock B Mean 3.00% 8.00% Sigma 15.00% 22.00% Comelation 0.3

C D E F 1 2 3 TWO STOCKS Varying the comelation coefficient Stock A Stock B Mean 3.00% 8.00% Sigma 15.00% 22.00% Comelation 0.3 4 5 7 10 Sample portfolio computation Stock A proportion Stock B propotion Portfolio mean Portfolio Sigma 10 12 13 14 Data table varying correlations Sigma 15 Mean 16 17 18 19 20 20 -1 -0.9 -0.8 0.7 -0,6 -0.5 0.4 -0.3 -0.2 -0.1 24 25 20 22 0.1 0.2 2 0.3 3 0.4 0.5 0.6 D E F G 35 0.7 0.8 0.9 1 96 37

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock