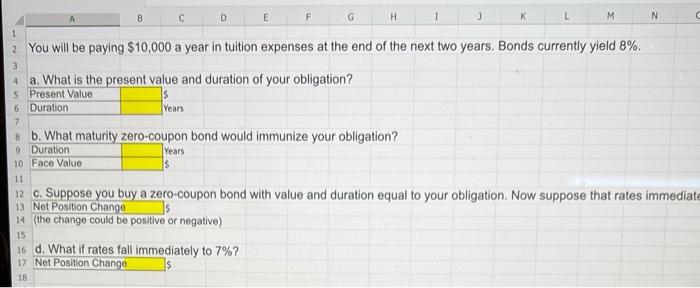

Question: c is cut off the full question is below Suppose you buy a zero-coupon bond with value and duration equal to your obligation. Now suppose

c is cut off the full question is below

Suppose you buy a zero-coupon bond with value and duration equal to your obligation. Now suppose that rates immediately increase to 9%. What happens to your net position, that is, to the

difference between the value of the bond and that of your tuition obligation?

You will be paying $10,000 a year in tuition expenses at the end of the next two years. Bonds currently yield 8%. a. What is the present value and duration of your obligation? b. What maturity zero-coupon bond would immunize your obligation? Duration lyears c. Suppose vou buv a zero-coupon bond with value and duration equal to your obligation. Now suppose that rates immediate (the change could be positive or negative) d. What if rates fall immediately to 7% ? 5

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock