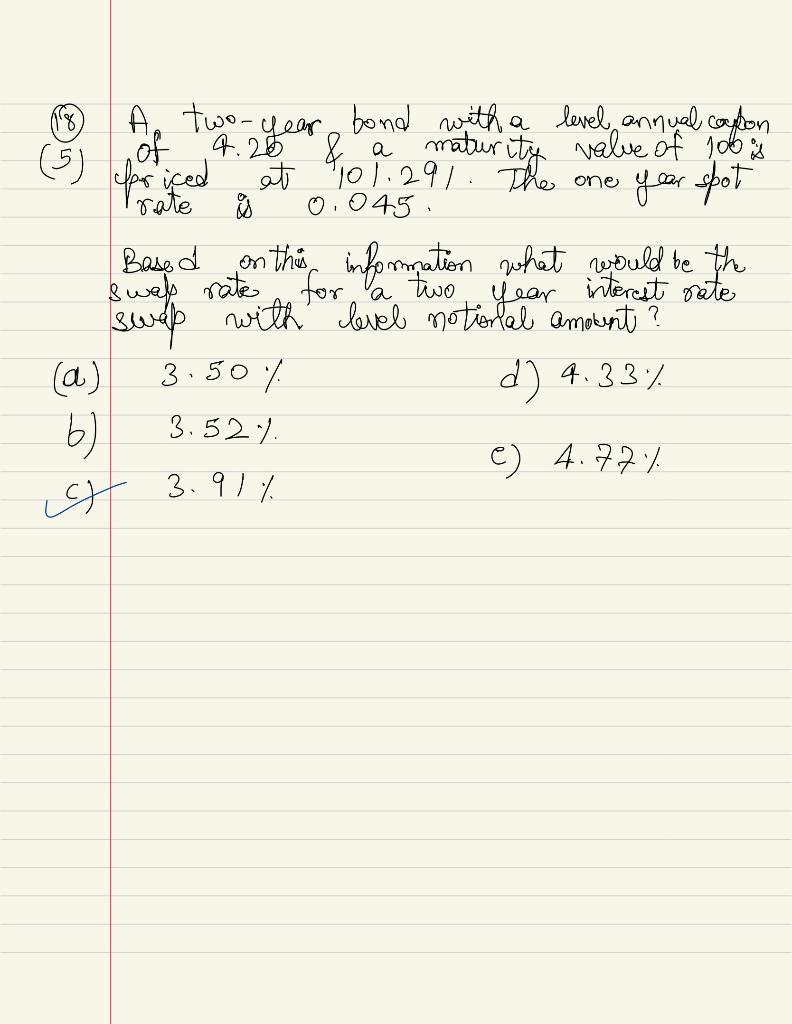

Question: (c) is not the correct answer (5) for iced A two-year bond with a level annual coupon of 4.20 & a at 101.291. The one

(c) is not the correct answer

(5) for iced A two-year bond with a level annual coupon of 4.20 & a at 101.291. The one year spot Irate 0.045 Based on this information what would be the swal rate for swap with level notional amocent ? 3.50 d) 4.33% 3.52). e) 4.724 (a b) 9 3.91%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock