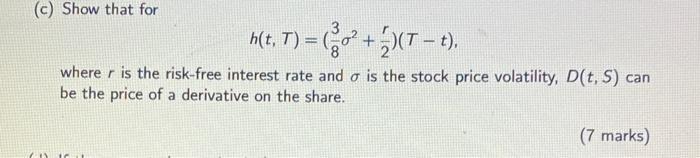

Question: (c) Show that for h(t, T) = ( +(T - t). where r is the risk-free interest rate and a is the stock price

(c) Show that for h(t, T) = ( +(T - t). where r is the risk-free interest rate and a is the stock price volatility, D(t, S) can be the price of a derivative on the share. (7 marks)

Step by Step Solution

★★★★★

3.42 Rating (149 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Solution O payopf at time of derivative S... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock