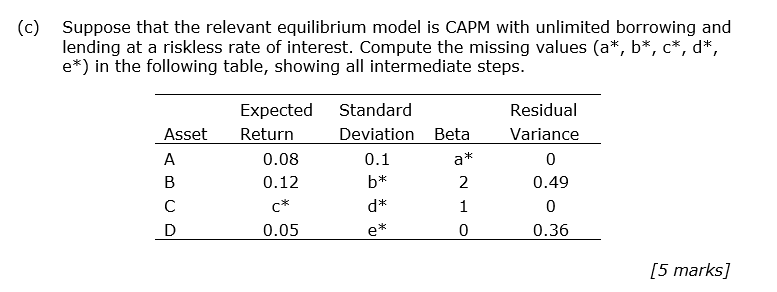

Question: (c) Suppose that the relevant equilibrium model is CAPM with unlimited borrowing and lending at a riskless rate of interest. Compute the missing values (a*,

(c) Suppose that the relevant equilibrium model is CAPM with unlimited borrowing and lending at a riskless rate of interest. Compute the missing values (a*, b*, c*, d*, e*) in the following table, showing all intermediate steps. Expected Standard Residual Variance Asset Return Deviation Beta A 0.1 a* 0 B b* 2 0.49 d* 1 0 D 0 0.36 [5 marks] 0.08 0.12 c* 0.05 e*

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock