Question: Calculate materiality Learning objective One of the underlying principles in auditing is the concept of materiality. An auditor designs procedures in order to identify and

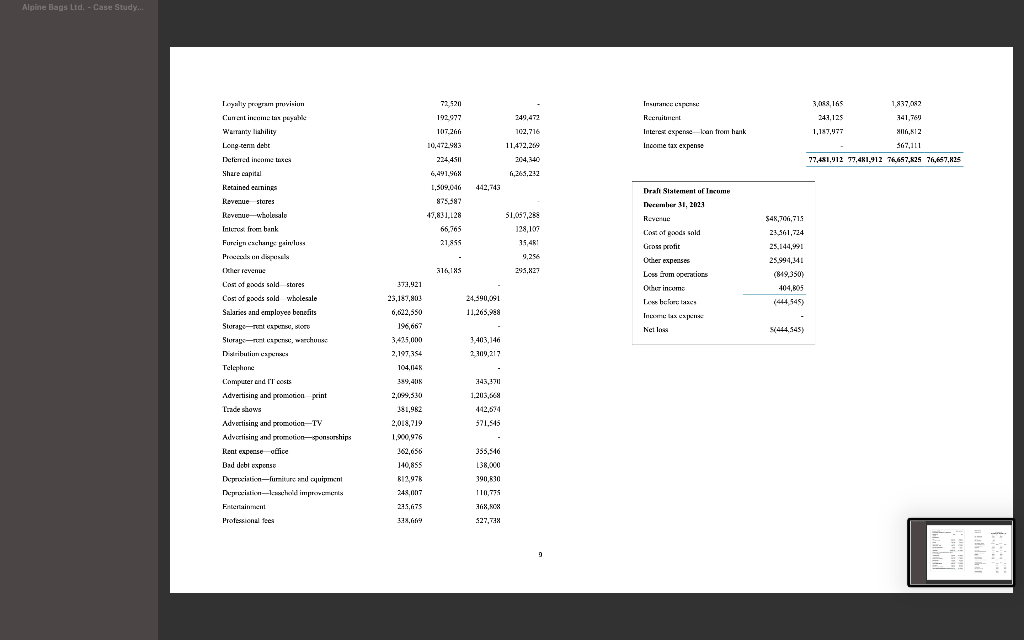

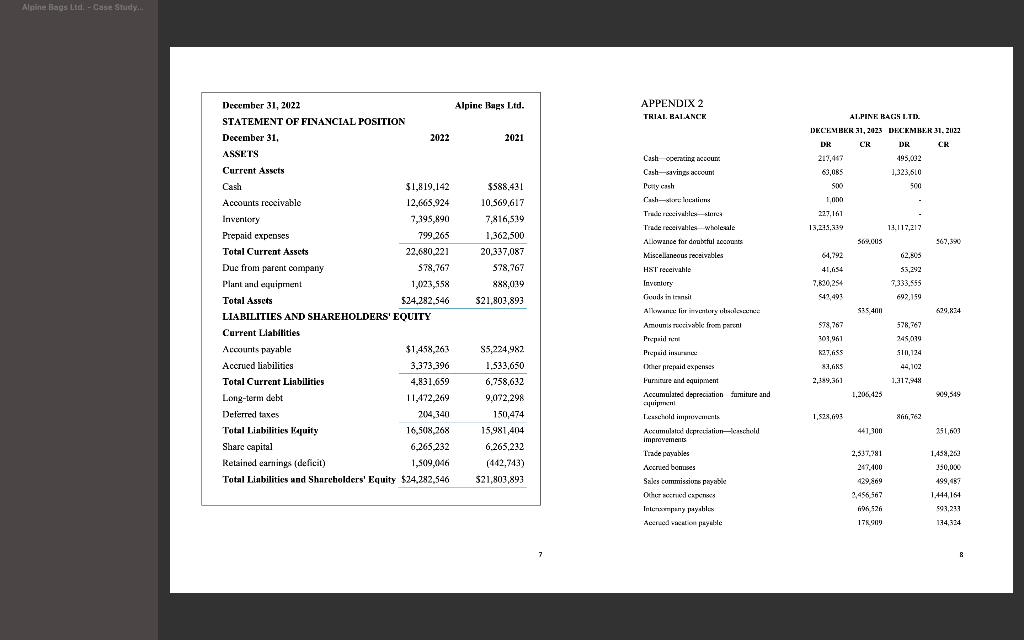

Calculate materiality Learning objective One of the underlying principles in auditing is the concept of materiality. An auditor designs procedures in order to identify and correct errors or irregularities that would have a material impact on the financial statements. Such errors or irregularities are considered material if they would impact the decision-making of the users of the financial statements. Materiality is used in determining audit procedures, selecting samples, and evaluating differences from client records to audit results. It is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the base figure to be used to calculate materiality, an auditor should consider the key driver of the business. They should ask themselves, What are the end users (such as shareholders and banks) of the financial statements going to be looking at? For example, will shareholders be interested in the net income that can be used to pay dividends and increase share price? Planning materiality W&S Partners audit methodology dictates that one planning materiality (PM) amount is to be used for the financial statements as a whole. Further, only one basis should be selecteda blended approach or average should not be used. The basis selected is the one determined to be the key driver of the business. W&S Partners uses the following percentages as starting points for the various bases. These starting points can be increased or decreased by taking into account qualitative client factors, which could be: the nature of the clients business and industry (such as rapid change, either through growth or downsizing, or unstable environment) the fact that it is a publicly listed entity (or subsidiary of one) subject to regulations the knowledge of or high risk of fraud. Base Profit before tax Revenues Total assets Equity Threshold (%) 5.0 1.0 1.0 3.0 Typically, profit before tax is used; however, it cannot be used if the entity is reporting a loss for the year or if profitability is not consistent.When calculating PM based on interim figures, it may be necessary to annualize the results. This allows the auditor to properly plan the audit based on an approximate projected year-end balance. Then, at year end, the figure is adjusted, if necessary, to reflect the actual results. Note: Adjustments to the starting points are made by an experienced auditor using their professional judgement. The aim is to set PM at a high enough level that appropriately balances the amount of testing, while still keeping the audit risk to an acceptable level. Performance materiality W&S Partners also dictates that performance materiality be determined for each audit engagement. Performance materiality is an amount less than planning materiality that reduces the likelihood that any uncorrected and undetected misstatements within a class of transactions, account balances, or disclosures in aggregate exceed overall planning materiality. W&S Partners policy is to use 70 percent of planning materiality to determine performance materiality. Required Using the working paper provided (A21): Select the basis for planning materiality that you believe is most appropriate. Justify your selection. Calculate the planning materiality (PM) using the December 31, 2023, trial balance and draft Statement of Income in Appendix 2. Based on your determination of PM, calculate and conclude on performance materiality. Alpine Bags Ltd. December 31, 2023 Setting materiality Users W/P ref: A21 Prepared by: _____ Date prepared: _____ Financial statement area of most concern to the user Base selected for planning materiality (PM): ______________________________________ Justification for selection: __________________________________________________________________________ __________________________________________________________________________ __________________________________________________________________________ __________________________________________________________________________ __________________________________________________________________________ Calculation of PM Trial balance amount: Normalizing adjustments (that is, non-recurring items) Annualized (if required): Benchmark applied Calculated materiality: Current Year _______________________ _______________________ _______________________ _______________________ _______________________ Prior Year _______________________ _______________________ _______________________ _______________________ _______________________ Conclusion: PM materiality is __________. Performance materiality: 70% ________. Conclusion: Performance materiality is __________. Discussion points Consider how you will use the planning materiality in your audit. What factors might lead you to increase or decrease the planning materiality amount? Are there qualitative factors that could impact your materiality decision?

Calculate materiality Learning objective One of the underlying principles in auditing is the concept of materiality. An auditor designs procedures in order to identify and correct errors or irregularities that would have a material impact on the financial statements. Such errors or irregularities are considered material if they would impact the decision-making of the users of the financial statements. Materiality is used in determining audit procedures, selecting samples, and evaluating differences from client records to audit results. It is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the base figure to be used to calculate materiality, an auditor should consider the key driver of the business. They should ask themselves, What are the end users (such as shareholders and banks) of the financial statements going to be looking at? For example, will shareholders be interested in the net income that can be used to pay dividends and increase share price? Planning materiality W&S Partners audit methodology dictates that one planning materiality (PM) amount is to be used for the financial statements as a whole. Further, only one basis should be selecteda blended approach or average should not be used. The basis selected is the one determined to be the key driver of the business. W&S Partners uses the following percentages as starting points for the various bases. These starting points can be increased or decreased by taking into account qualitative client factors, which could be: the nature of the clients business and industry (such as rapid change, either through growth or downsizing, or unstable environment) the fact that it is a publicly listed entity (or subsidiary of one) subject to regulations the knowledge of or high risk of fraud. Base Profit before tax Revenues Total assets Equity Threshold (%) 5.0 1.0 1.0 3.0 Typically, profit before tax is used; however, it cannot be used if the entity is reporting a loss for the year or if profitability is not consistent.When calculating PM based on interim figures, it may be necessary to annualize the results. This allows the auditor to properly plan the audit based on an approximate projected year-end balance. Then, at year end, the figure is adjusted, if necessary, to reflect the actual results. Note: Adjustments to the starting points are made by an experienced auditor using their professional judgement. The aim is to set PM at a high enough level that appropriately balances the amount of testing, while still keeping the audit risk to an acceptable level. Performance materiality W&S Partners also dictates that performance materiality be determined for each audit engagement. Performance materiality is an amount less than planning materiality that reduces the likelihood that any uncorrected and undetected misstatements within a class of transactions, account balances, or disclosures in aggregate exceed overall planning materiality. W&S Partners policy is to use 70 percent of planning materiality to determine performance materiality. Required Using the working paper provided (A21): Select the basis for planning materiality that you believe is most appropriate. Justify your selection. Calculate the planning materiality (PM) using the December 31, 2023, trial balance and draft Statement of Income in Appendix 2. Based on your determination of PM, calculate and conclude on performance materiality. Alpine Bags Ltd. December 31, 2023 Setting materiality Users W/P ref: A21 Prepared by: _____ Date prepared: _____ Financial statement area of most concern to the user Base selected for planning materiality (PM): ______________________________________ Justification for selection: __________________________________________________________________________ __________________________________________________________________________ __________________________________________________________________________ __________________________________________________________________________ __________________________________________________________________________ Calculation of PM Trial balance amount: Normalizing adjustments (that is, non-recurring items) Annualized (if required): Benchmark applied Calculated materiality: Current Year _______________________ _______________________ _______________________ _______________________ _______________________ Prior Year _______________________ _______________________ _______________________ _______________________ _______________________ Conclusion: PM materiality is __________. Performance materiality: 70% ________. Conclusion: Performance materiality is __________. Discussion points Consider how you will use the planning materiality in your audit. What factors might lead you to increase or decrease the planning materiality amount? Are there qualitative factors that could impact your materiality decision?

Alpine Bags Ltd. - Case Study... In response 72, 120 192.972 349,472 Reni 243,125 1,187,027 1.817,042 341,760 116,2 1017.2611 10,472.983 102,716 11,472,20 204,10 Interer experkan from hunk Income tax expense 367,111 77,481.912 77.401,912 76,657,825 76,667.825 442,743 224.4501 6,491.964 1,509.06 825.387 -17,831,L28 66.765 Draft Statement of Income December 31, 2021 Rever 51.052.24 128,10 35,401 $4,701,715 21.561,714 25,144,091 25.994,941 (819.350) 104.93 9,256 - 316.15 295.X27 Car of Raods sold Grosxotit Other expenses Los trum operatives Other income Label I beX ENIRO Netlog Tavaly program provision Cunct income la pelle W'erranty Wahility Loup ten debt Telenci income taxes Shure capital Retained eunings Revecue stores Revue Wholesale In uns from bank Furcin esclungs in Prix und her revenue Cost of Raods sold stores Cost of goods sold wholesale Salaries and employee benedits Storage Rat DTS, Stura-huise Dribution Telehane Computer und IT costs Advertising and resocon print Trade shows Adructising and promotion-TV Advertising and personships Rent expense office Bad Jcbt uspense :pris- in-furniture Pril ajuipmeni Despruit-ci impre Flertainment Professional fees 24,390,091 11,265,988 (444.545) 54444.545) 3,408,146 2.309,217 - 373.921 23,189,803 6,622,350 196,667 3,415,000 2,197,354 104,1148 389,4118 2,099,530 181,982 2,018,719 1.900,976 182,656 140,855 B12,976 248,007 1.205, 571.545 355,516 138,000 390,30 110,775 36X,CX 527,28 215,675 9 Alpine Bags Ltd. - Case Study... APPENDIX 2 TRIAI, RALANCE December 31, 2022 Alpine Bags Ltd. STATEMENT OF FINANCIAL POSITION December 31, 2022 2021 ASSETS Current Asset Cash $1,819,142 $588,431 Accounts rcocivable 12,665,924 10.569.617 Inventory 7,395,890 7,816,539 Prepaid expenses 799.265 1,362,500 Total Current Assets 22,680.221 20,337,087 Due from parent company 578,767 $78,767 Plant and equipment 1,023,558 888,039 Total Assets 524,282,546 $21,803,893 LIABILITIES AND SHAREHOLDERS' EQUITY Current Liabilities Accounts payable $1,458,263 S5,224,982 Accrued liabilities 3,373 396 mo 1.533,650 Total Current Linbilities 4,831.659 6.758,632 Long-term delt 11,472,269 9.072.298 Deferred taxes secas 2014 340 150,474 Total Liabilities Equity 16,508,268 15,981,404 Share capital 6,265,232 6.265.222 Retained earnings (deficit) 1,509,046 (442,743) Total Liabilities and Shareholders' Equity $24,282,546 $21,803,893 Cash opening accoun Cash savings account Pully eash Cash kelis Trude rivalsares Trade receivalley whole le Allowance for doubculocuits Miscellaneous receivables HNT receivahle Inventury Cuisin innst Alkmana: lur inviter les Amuumis ble from parent Propuilor Prepaid in her prepaid expenses Furniture and equipment Accumulated depreciation fumiture and |eularlil impuvanars Accumulalai dapreciation cold improvements Trade payables Accrued bonuses Sales commissions payable Other creden Int -lix Acredito yelle ALPINE BACIS LTD DECEMBER 31, 2023 DECEMBER 31.2022 DR CR DR CR 195,002 63,0BS 1,323.6.0 SOO 500 1,000 227,161 13,215,339 13.117,217 569.005 567,390 61,792 62.105 41.654 53,292 7,620,254 7,333,555 S41,493 692,159 535400 629,834 S78.760 578,767 1961 148,019 K27,655 SIN,124 83,685 44,102 2,349,361 1.317,948 1,206,425 909,519 1.518,69 86,762 441,300 351,603 2,537.781 247.400 429,869 1,458,25 150,000 199,487 1,444,164 693,211 106 526 176909 134,334 7 & Alpine Bags Ltd. - Case Study... In response 72, 120 192.972 349,472 Reni 243,125 1,187,027 1.817,042 341,760 116,2 1017.2611 10,472.983 102,716 11,472,20 204,10 Interer experkan from hunk Income tax expense 367,111 77,481.912 77.401,912 76,657,825 76,667.825 442,743 224.4501 6,491.964 1,509.06 825.387 -17,831,L28 66.765 Draft Statement of Income December 31, 2021 Rever 51.052.24 128,10 35,401 $4,701,715 21.561,714 25,144,091 25.994,941 (819.350) 104.93 9,256 - 316.15 295.X27 Car of Raods sold Grosxotit Other expenses Los trum operatives Other income Label I beX ENIRO Netlog Tavaly program provision Cunct income la pelle W'erranty Wahility Loup ten debt Telenci income taxes Shure capital Retained eunings Revecue stores Revue Wholesale In uns from bank Furcin esclungs in Prix und her revenue Cost of Raods sold stores Cost of goods sold wholesale Salaries and employee benedits Storage Rat DTS, Stura-huise Dribution Telehane Computer und IT costs Advertising and resocon print Trade shows Adructising and promotion-TV Advertising and personships Rent expense office Bad Jcbt uspense :pris- in-furniture Pril ajuipmeni Despruit-ci impre Flertainment Professional fees 24,390,091 11,265,988 (444.545) 54444.545) 3,408,146 2.309,217 - 373.921 23,189,803 6,622,350 196,667 3,415,000 2,197,354 104,1148 389,4118 2,099,530 181,982 2,018,719 1.900,976 182,656 140,855 B12,976 248,007 1.205, 571.545 355,516 138,000 390,30 110,775 36X,CX 527,28 215,675 9 Alpine Bags Ltd. - Case Study... APPENDIX 2 TRIAI, RALANCE December 31, 2022 Alpine Bags Ltd. STATEMENT OF FINANCIAL POSITION December 31, 2022 2021 ASSETS Current Asset Cash $1,819,142 $588,431 Accounts rcocivable 12,665,924 10.569.617 Inventory 7,395,890 7,816,539 Prepaid expenses 799.265 1,362,500 Total Current Assets 22,680.221 20,337,087 Due from parent company 578,767 $78,767 Plant and equipment 1,023,558 888,039 Total Assets 524,282,546 $21,803,893 LIABILITIES AND SHAREHOLDERS' EQUITY Current Liabilities Accounts payable $1,458,263 S5,224,982 Accrued liabilities 3,373 396 mo 1.533,650 Total Current Linbilities 4,831.659 6.758,632 Long-term delt 11,472,269 9.072.298 Deferred taxes secas 2014 340 150,474 Total Liabilities Equity 16,508,268 15,981,404 Share capital 6,265,232 6.265.222 Retained earnings (deficit) 1,509,046 (442,743) Total Liabilities and Shareholders' Equity $24,282,546 $21,803,893 Cash opening accoun Cash savings account Pully eash Cash kelis Trude rivalsares Trade receivalley whole le Allowance for doubculocuits Miscellaneous receivables HNT receivahle Inventury Cuisin innst Alkmana: lur inviter les Amuumis ble from parent Propuilor Prepaid in her prepaid expenses Furniture and equipment Accumulated depreciation fumiture and |eularlil impuvanars Accumulalai dapreciation cold improvements Trade payables Accrued bonuses Sales commissions payable Other creden Int -lix Acredito yelle ALPINE BACIS LTD DECEMBER 31, 2023 DECEMBER 31.2022 DR CR DR CR 195,002 63,0BS 1,323.6.0 SOO 500 1,000 227,161 13,215,339 13.117,217 569.005 567,390 61,792 62.105 41.654 53,292 7,620,254 7,333,555 S41,493 692,159 535400 629,834 S78.760 578,767 1961 148,019 K27,655 SIN,124 83,685 44,102 2,349,361 1.317,948 1,206,425 909,519 1.518,69 86,762 441,300 351,603 2,537.781 247.400 429,869 1,458,25 150,000 199,487 1,444,164 693,211 106 526 176909 134,334 7 &

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts