Question: Calculate VECs WACC using the data in Exhibit 1. Hamilton: It may be difficult to estimate the cost of borrowing in the current recessionary environment.

Calculate VECs WACC using the data in Exhibit 1.

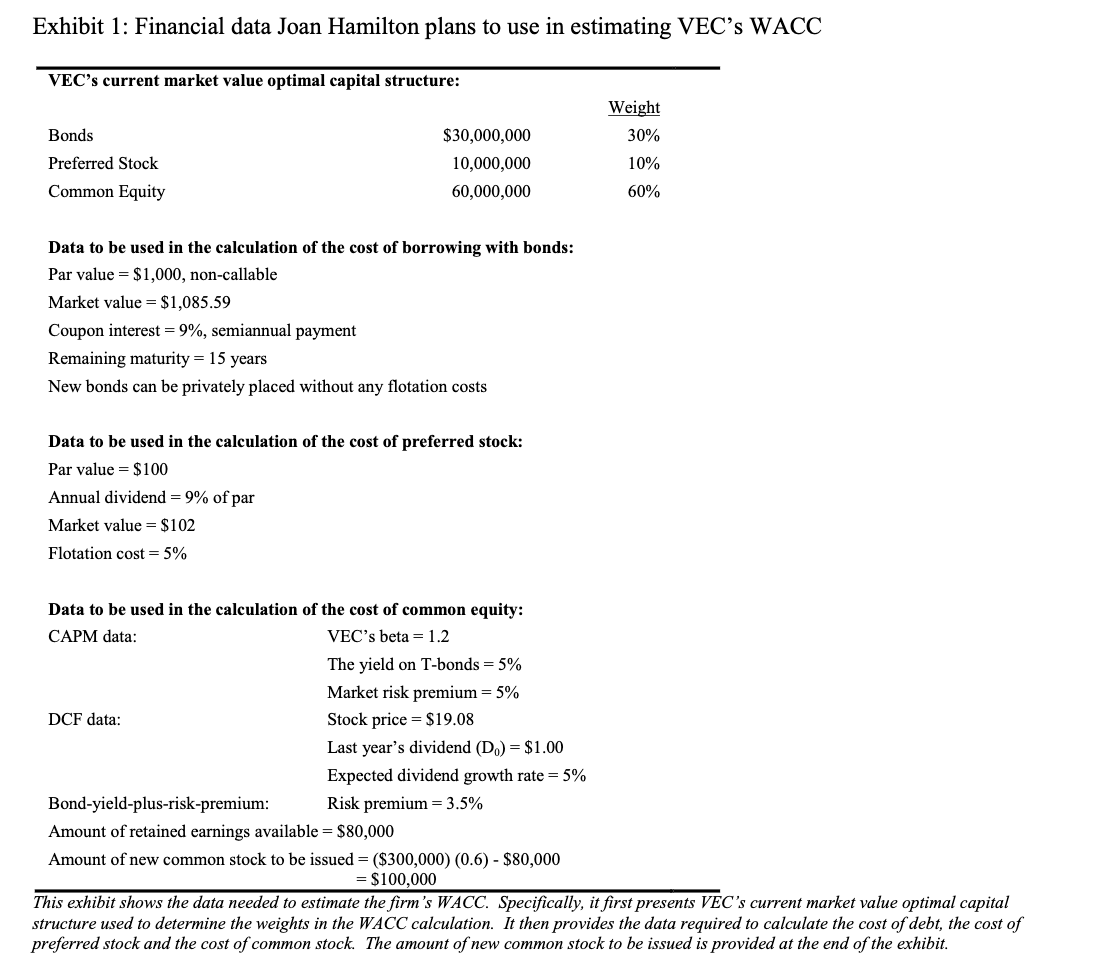

Hamilton: It may be difficult to estimate the cost of borrowing in the current recessionary environment. Gray: We can determine the yield to maturity (YTM) on our outstanding bonds by using their current market prices. We can assume that we will be able to issue additional bonds with this YTM as the cost of borrowing. We should be able to place the new bonds without any flotation costs. Therefore, we can assume no flotation costs in our calculations. We can re-examine the feasibility of the project later before raising funds by using sensitivity analysis to assess the impact of possible changes in interest rates on the net present value of the project. Hamilton: Do you think the company's current market value capital structure is optimal? Can we use the current percentages of the capital components as weights in the calculation of the company's WACC? Gray: Yes, I believe that the company's current market value capital structure of 30% debt, 10% preferred stock and 60% equity is optimal. We have about $80,000 in retained earnings this year, which is also available in cash. We should be able to use this year's retained earnings to finance part of the equity financing required for the project. However, we will have to issue some new common shares for the remainder of the necessary equity financing. We can assume a flotation cost of about 10% for the new common shares. Hamilton: There are three basic methods of calculating a firm's cost of equity when retained earnings are used as equity capital: 1) the capital asset pricing method (CAPM); 2) the discounted cash flow (DCF) approach; and, 3) the bond-yield-plus-risk-premium method. Which of these methods should we use in the calculation of our cost of retained earnings? Gray: Although each of these methods has its merits, I believe that the most appropriate approach for our company would be to find an average cost with the three methods. Benny Gray gave only one week to Joan Hamilton for her estimation of VEC's WACC. With the instructions she received from Benny Gray and with the help of the financial data in Exhibit 1, Joan Hamilton began the task of estimating the company's WACC immediately. Exhibit 1: Financial data Joan Hamilton plans to use in estimating VEC's WACC VEC's current market value optimal capital structure: Weight 30% Bonds Preferred Stock Common Equity $30,000,000 10,000,000 60,000,000 10% 60% Data to be used in the calculation of the cost of borrowing with bonds: Par value = $1,000, non-callable Market value = $1,085.59 Coupon interest = 9%, semiannual payment Remaining maturity = 15 years New bonds can be privately placed without any flotation costs Data to be used in the calculation of the cost of preferred stock: Par value = $100 Annual dividend = 9% of par Market value = $102 Flotation cost = 5% Data to be used in the calculation of the cost of common equity: CAPM data: VEC's beta = 1.2 The yield on T-bonds = 5% Market risk premium = 5% DCF data: Stock price = $19.08 Last year's dividend (D.) = $1.00 Expected dividend growth rate = 5% Bond-yield-plus-risk-premium: Risk premium = 3.5% Amount of retained earnings available = $80,000 Amount of new common stock to be issued = ($300,000) (0.6) - $80,000 = $100,000 This exhibit shows the data needed to estimate the firm's WACC. Specifically, it first presents VEC's current market value optimal capital structure used to determine the weights in the WACC calculation. It then provides the data required to calculate the cost of debt, the cost of preferred stock and the cost of common stock. The amount of new common stock to be issued is provided at the end of the exhibit. Hamilton: It may be difficult to estimate the cost of borrowing in the current recessionary environment. Gray: We can determine the yield to maturity (YTM) on our outstanding bonds by using their current market prices. We can assume that we will be able to issue additional bonds with this YTM as the cost of borrowing. We should be able to place the new bonds without any flotation costs. Therefore, we can assume no flotation costs in our calculations. We can re-examine the feasibility of the project later before raising funds by using sensitivity analysis to assess the impact of possible changes in interest rates on the net present value of the project. Hamilton: Do you think the company's current market value capital structure is optimal? Can we use the current percentages of the capital components as weights in the calculation of the company's WACC? Gray: Yes, I believe that the company's current market value capital structure of 30% debt, 10% preferred stock and 60% equity is optimal. We have about $80,000 in retained earnings this year, which is also available in cash. We should be able to use this year's retained earnings to finance part of the equity financing required for the project. However, we will have to issue some new common shares for the remainder of the necessary equity financing. We can assume a flotation cost of about 10% for the new common shares. Hamilton: There are three basic methods of calculating a firm's cost of equity when retained earnings are used as equity capital: 1) the capital asset pricing method (CAPM); 2) the discounted cash flow (DCF) approach; and, 3) the bond-yield-plus-risk-premium method. Which of these methods should we use in the calculation of our cost of retained earnings? Gray: Although each of these methods has its merits, I believe that the most appropriate approach for our company would be to find an average cost with the three methods. Benny Gray gave only one week to Joan Hamilton for her estimation of VEC's WACC. With the instructions she received from Benny Gray and with the help of the financial data in Exhibit 1, Joan Hamilton began the task of estimating the company's WACC immediately. Exhibit 1: Financial data Joan Hamilton plans to use in estimating VEC's WACC VEC's current market value optimal capital structure: Weight 30% Bonds Preferred Stock Common Equity $30,000,000 10,000,000 60,000,000 10% 60% Data to be used in the calculation of the cost of borrowing with bonds: Par value = $1,000, non-callable Market value = $1,085.59 Coupon interest = 9%, semiannual payment Remaining maturity = 15 years New bonds can be privately placed without any flotation costs Data to be used in the calculation of the cost of preferred stock: Par value = $100 Annual dividend = 9% of par Market value = $102 Flotation cost = 5% Data to be used in the calculation of the cost of common equity: CAPM data: VEC's beta = 1.2 The yield on T-bonds = 5% Market risk premium = 5% DCF data: Stock price = $19.08 Last year's dividend (D.) = $1.00 Expected dividend growth rate = 5% Bond-yield-plus-risk-premium: Risk premium = 3.5% Amount of retained earnings available = $80,000 Amount of new common stock to be issued = ($300,000) (0.6) - $80,000 = $100,000 This exhibit shows the data needed to estimate the firm's WACC. Specifically, it first presents VEC's current market value optimal capital structure used to determine the weights in the WACC calculation. It then provides the data required to calculate the cost of debt, the cost of preferred stock and the cost of common stock. The amount of new common stock to be issued is provided at the end of the exhibit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts