Question: Calculation-type Problems: SHOW ALL YOUR WORK. DO NOT PRESENT ANSWERS ONLY 2. The risk-free rate, average returns, standard deviations, below. Fund c 13.690 12.4% Std

Calculation-type Problems: SHOW ALL YOUR WORK. DO NOT PRESENT ANSWERS ONLY

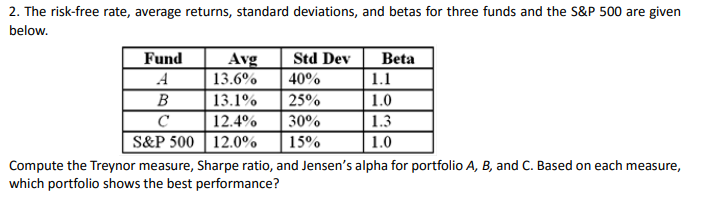

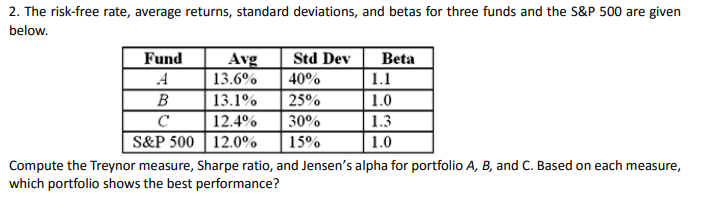

2. The risk-free rate, average returns, standard deviations, below. Fund c 13.690 12.4% Std Dev 2590 3090 S&P500 12.090 and betas for three funds and the 500 are given Beta 1.1 1.0 1.3 1.0 Compute the Treynor measure, Sharpe ratio, and Jensen's alpha for portfolio A, B, and C. Based on each measure, which portfolio shows the best performance?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock