Question: Can anyone explain what I'm doing wrong? I keep getting this problem wrong by .01 give or take. The correct answer, in this case, is

Can anyone explain what I'm doing wrong? I keep getting this problem wrong by .01 give or take. The correct answer, in this case, is 2.59% but I am getting 2.60%.

![is 2.59% but I am getting 2.60%. [Related to Solved Problem 5.2b]](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/09/66f6f900d5f9d_63266f6f9004d58e.jpg)

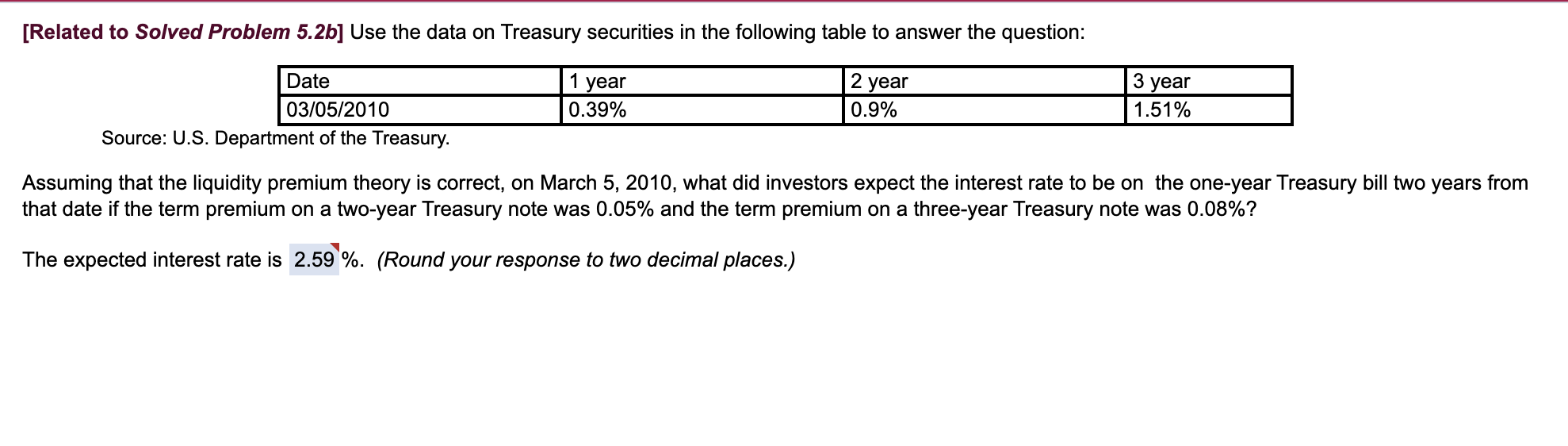

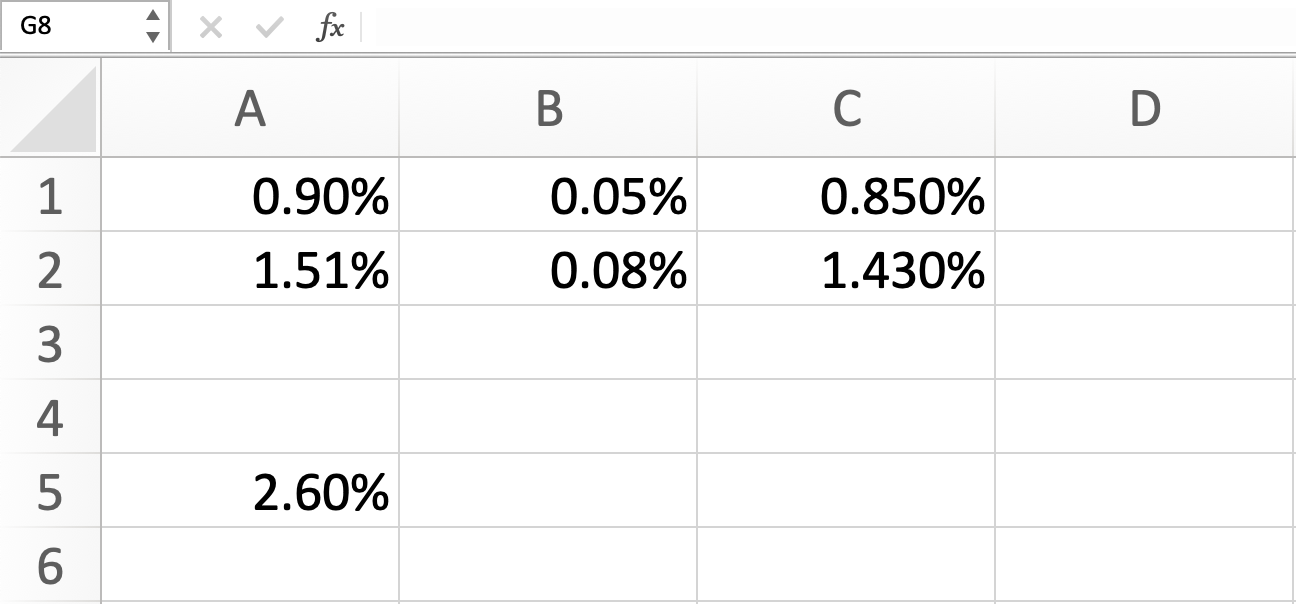

[Related to Solved Problem 5.2b] Use the data on Treasury securities in the following table to answer the question: Date 1 year 2 year 3 year 0.39% 0.9% 1.51% 03/05/2010 Source: U.S. Department of the Treasury. Assuming that the liquidity premium theory is correct, on March 5, 2010, what did investors expect the interest rate to be on the one-year Treasury bill two years from that date if the term premium on a two-year Treasury note was 0.05% and the term premium on a three-year Treasury note was 0.08%? The expected interest rate is 2.59 %. (Round your response to two decimal places.) G8 f B D 1 0.90% 0.05% 0.08% 0.850% 1.430% 2 1.51% Nm 3 4 5 2.60% 6 G8 A X fx A B 1 0.009 0.0005 =A1-B1 =A2-B2 2 0.0151 0.0008 3 4 5 =((1+C2)^3)/((1+C1)^2)-1 6 [Related to Solved Problem 5.2b] Use the data on Treasury securities in the following table to answer the question: Date 1 year 2 year 3 year 0.39% 0.9% 1.51% 03/05/2010 Source: U.S. Department of the Treasury. Assuming that the liquidity premium theory is correct, on March 5, 2010, what did investors expect the interest rate to be on the one-year Treasury bill two years from that date if the term premium on a two-year Treasury note was 0.05% and the term premium on a three-year Treasury note was 0.08%? The expected interest rate is 2.59 %. (Round your response to two decimal places.) G8 f B D 1 0.90% 0.05% 0.08% 0.850% 1.430% 2 1.51% Nm 3 4 5 2.60% 6 G8 A X fx A B 1 0.009 0.0005 =A1-B1 =A2-B2 2 0.0151 0.0008 3 4 5 =((1+C2)^3)/((1+C1)^2)-1 6

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts