Question: Can anyone solve this question and please answer it clear THANK YOU !!!!! QUESTION 4 (CONTEMPORARY ISSUES IN FMS AND FUND MANAGEMET) a) On April

Can anyone solve this question and please answer it clear THANK YOU !!!!!

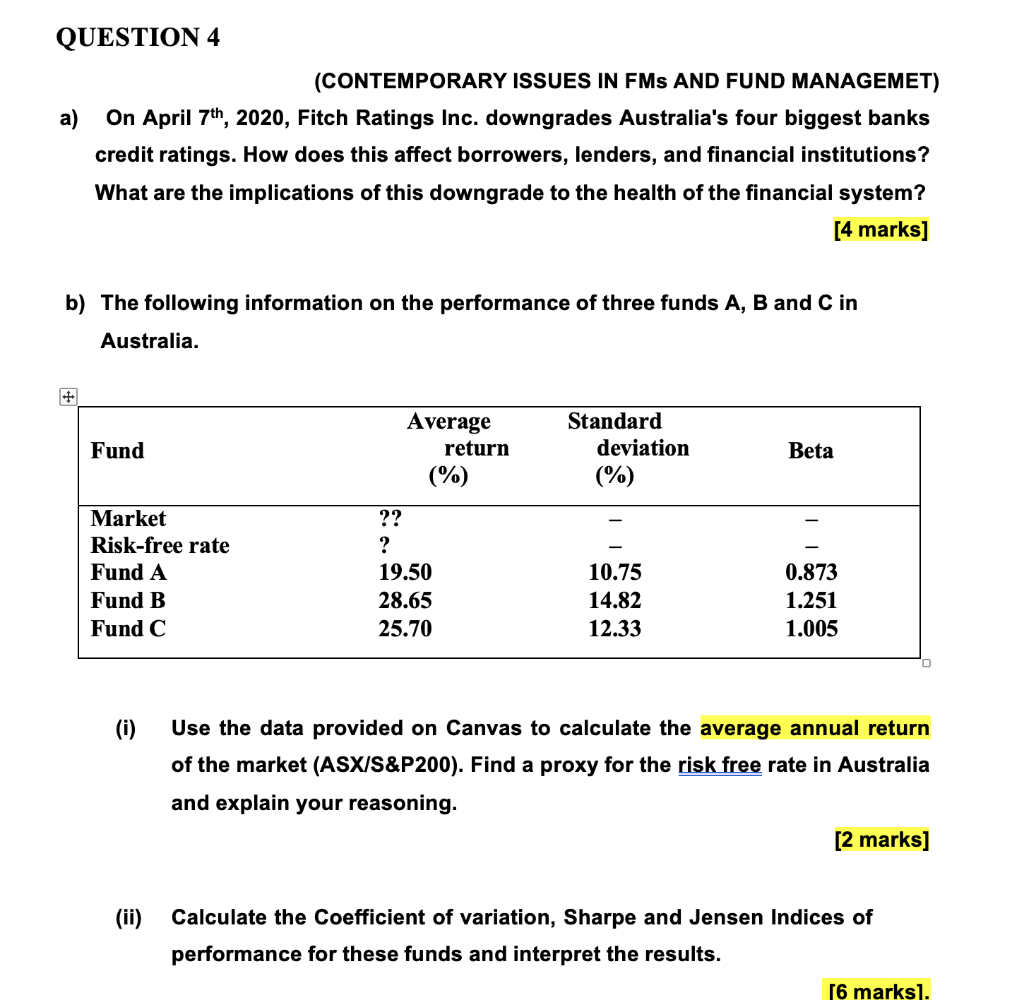

QUESTION 4 (CONTEMPORARY ISSUES IN FMS AND FUND MANAGEMET) a) On April 7th, 2020, Fitch Ratings Inc. downgrades Australia's four biggest banks credit ratings. How does this affect borrowers, lenders, and financial institutions? What are the implications of this downgrade to the health of the financial system? [4 marks] b) The following information on the performance of three funds A, B and C in Australia. Average return Fund Standard deviation (%) Beta (%) Market Risk-free rate Fund A Fund B Fund C ?? ? 19.50 28.65 25.70 10.75 14.82 12.33 0.873 1.251 1.005 (i) Use the data provided on Canvas to calculate the average annual return of the market (ASX/S&P200). Find a proxy for the risk free rate in Australia and explain your reasoning. [2 marks] (ii) Calculate the Coefficient of variation, Sharpe and Jensen Indices of performance for these funds and interpret the results. [6 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts