Question: Can sombody explain how they got this answer, previous answer was incorrect, please help me The expected return on security A is 9% and the

Can sombody explain how they got this answer, previous answer was incorrect, please help me

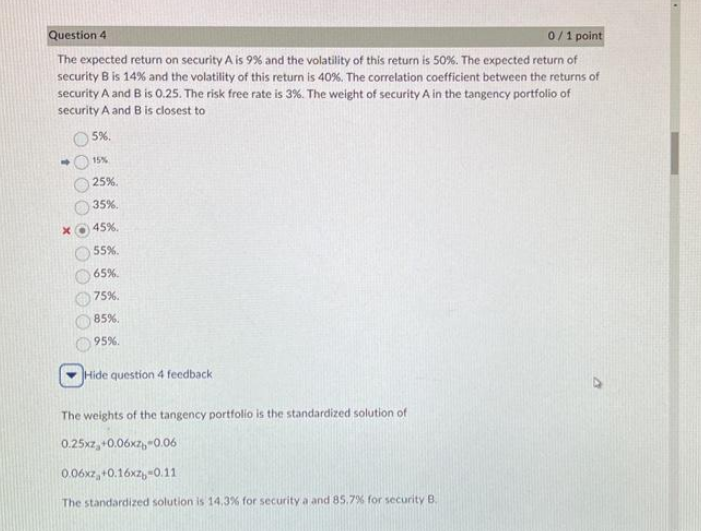

The expected return on security A is 9% and the volatility of this return is 50%. The expected return of security B is 14% and the volatility of this return is 40%. The correlation coefficient between the returns of security A and B is 0.25 . The risk free rate is 3%. The weight of security A in the tangency portfolio of security A and B is closest to fide question 4 feedback The weights of the tangency portfolio is the standardized solution of 0.25xza+0.06xzb=0.060.06xza+0.16xzb=0.11 The standardized solution is 14.3% for security a and 85.7% for security B. The expected return on security A is 9% and the volatility of this return is 50%. The expected return of security B is 14% and the volatility of this return is 40%. The correlation coefficient between the returns of security A and B is 0.25 . The risk free rate is 3%. The weight of security A in the tangency portfolio of security A and B is closest to fide question 4 feedback The weights of the tangency portfolio is the standardized solution of 0.25xza+0.06xzb=0.060.06xza+0.16xzb=0.11 The standardized solution is 14.3% for security a and 85.7% for security B

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts