Question: Can some one help explain why this it the solution for Principles of Auditing & Other Assurance Service 21st e by O Ray Ray Whittington

Can some one help explain why this it the solution for Principles of Auditing & Other Assurance Service 21st e by O Ray Ray Whittington Chapter 7 Question 7-45 (in class Team Cases)

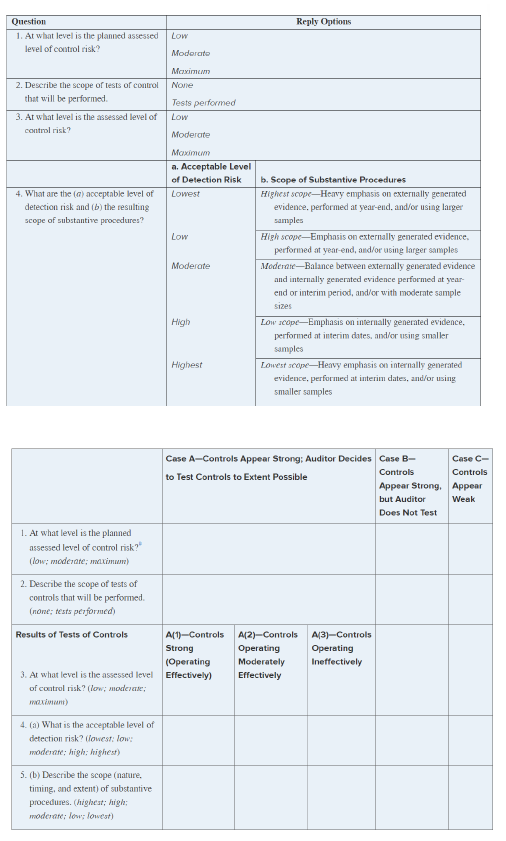

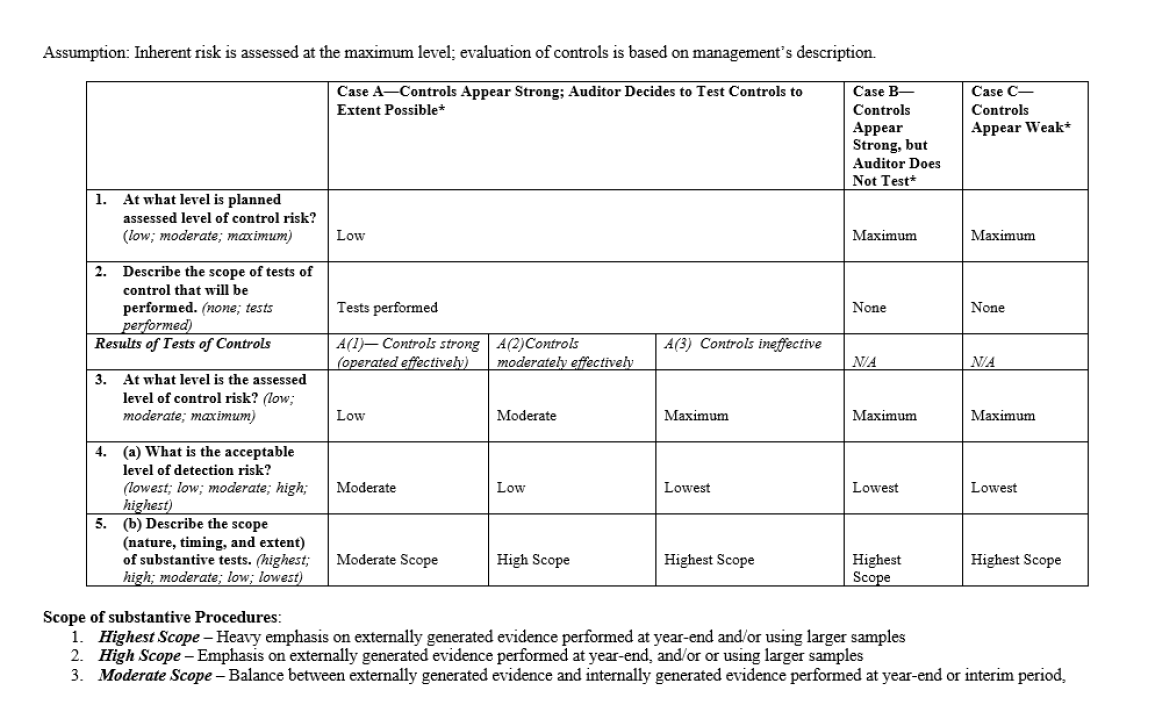

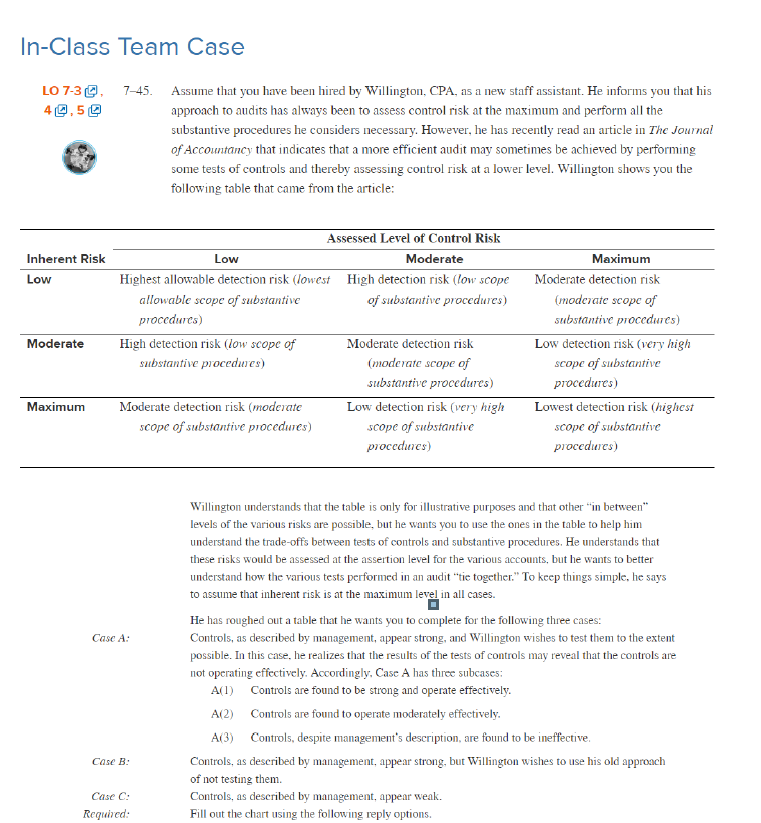

Question Reply Options 1. At what level is the planned assessed | Low level of control risk? Moderate 2. Describe the scope of tests of control None that will be performed Tests performed 3. At what level is the assessed level of Low control risk? Moderate n. Acceptable Level of Detection Risk b. Scope of Substantive Procedures 4. What are the (o) acceptable level of Lowest Highest scope-Henry emphasis on externally generated detection risk and (b) the resulting evidence. performed at year-end. andfor using larger scope of substantive procedures? samples Low High scope-Emphasis on externally generated evidence. performed at year-end, and/or using larger samples Moderate Moderate-Balance between externally generated evidence and internally generated evidence performed at year- end or interim period, andfor with moderate sample sizes High Low rope-Emphasis on internally generated evidence. performed at interim dates, andfor using smaller samples Highest Lower scope-Heavy emphasis on internally generated evidence, performed at interim dates, andfor using smaller samples Case A-Controls Appear Strong: Auditor Decides| Case B- Case C- to Test Controls to Extent Possible Controls Controls Appear Strong, Appear but Auditor Weak Does Not Test 1. At what level is the planned assessed level of control risk?" flow; moderate; maximum) 2. Describe the scope of tests of controls that will be performed. (none; rests performed) Results of Tests of Controls A(1)-Controls A(2)-Controls A(3]-Controls Strong Operating Operating Operating Moderately Ineffectively 3. At what level is the assessed level Effectively) Effectively of control risk? (low; moderate; 4. (a) What is the acceptable level of detection risk? (lowest: lows moderate; high: highest) 5. (b) Describe the scope (nature. timing, and extent) of substantive procedures. (highest; high; moderate; low lowest)Assumption: Inherent risk is assessed at the maximum level; evaluation of controls is based on management's description. Case A-Controls Appear Strong; Auditor Decides to Test Controls to Case B- Case C- Extent Possible* Controls Controls Appear Appear Weak* Strong, but Auditor Does Not Test* 1. At what level is planned assessed level of control risk? (low; moderate; maximum) Low Maximum Maximum 2. Describe the scope of tests of control that will be performed. (mone; tests Tests performed None None performed) Results of Tests of Controls A(1)- Controls strong A(2) Controls A(3) Controls ineffective (operated effectively) moderately effectively NIA NIA 3. At what level is the assessed level of control risk? (low; moderate; maximum) Low Moderate Maximum Maximum Maximum 4. (a) What is the acceptable level of detection risk? (lowest; low; moderate; high; Moderate Low Lowest Lowest Lowest highest) 5. (b) Describe the scope (nature, timing, and extent) of substantive tests. (highest; Moderate Scope High Scope Highest Scope Highest Highest Scope high; moderate; low; lowest) Scope Scope of substantive Procedures: 1. Highest Scope - Heavy emphasis on externally generated evidence performed at year-end and/or using larger samples 2. High Scope - Emphasis on externally generated evidence performed at year-end, and/or or using larger samples 3. Moderate Scope - Balance between externally generated evidence and internally generated evidence performed at year-end or interim period,In-Class Team Case LO 7-39. 7-45. Assume that you have been hired by Willington, CPA, as a new staff assistant. He informs you that his 40.50 approach to audits has always been to assess control risk at the maximum and perform all the substantive procedures he considers necessary. However, he has recently read an article in The Journal of Accountancy that indicates that a more efficient audit may sometimes be achieved by performing some tests of controls and thereby assessing control risk at a lower level. Willington shows you the following table that came from the article: Assessed Level of Control Risk Inherent Risk Low Moderate Maximum Low Highest allowable detection risk (lowest High detection risk (low scope Moderate detection risk allowable scope of substantive of substantive procedures) (moderate scope of procedures) substantive procedures) Moderate High detection risk (low scope of Moderate detection risk Low detection risk (very high substantive procedures) (moderate scope of scope of substantive substantive procedures) procedures Maximum Moderate detection risk (moderate Low detection risk (very high Lowest detection risk (highest scope of substantive procedures) scope of substantive scope of substantive procedures) procedures) Willington understands that the table is only for illustrative purposes and that other "in between" levels of the various risks are possible, but he wants you to use the ones in the table to help him understand the trade-offs between tests of controls and substantive procedures, He understands that these risks would be assessed at the assertion level for the various accounts, but he wants to better understand how the various tests performed in an audit "tic together." To keep things simple, he says to assume that inherent risk is at the maximum level in all cases. He has roughed out a table that he wants you to complete for the following three cases: Case A: Controls, as described by management, appear strong, and Willington wishes to test them to the extent possible. In this case. he realizes that the results of the tests of controls may reveal that the controls are not operating effectively. Accordingly. Case A has three subcases; A(1) Controls are found to be strong and operate effectively. A(2) Controls are found to operate moderately effectively. A(3) Controls, despite management's description, are found to be ineffective. Case B: Controls, as described by management, appear strong, but Willington wishes to use his old approach of not testing them. Case C: Controls, as described by management, appear weak. Required: Fill out the chart using the following reply options