Question: Can someone help me I don't know if I'm going in the right direction Greenville's Shoe Company has a periodic inventory system and uses the

Can someone help me I don't know if I'm going in the right direction

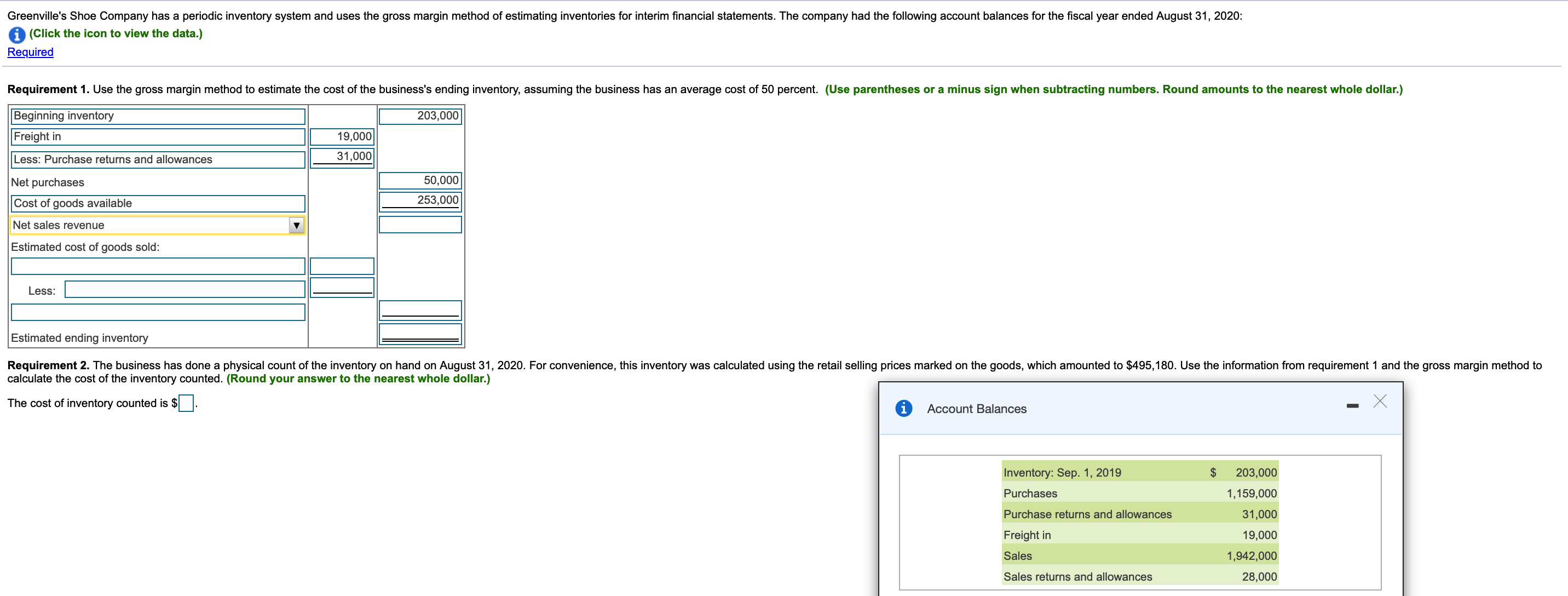

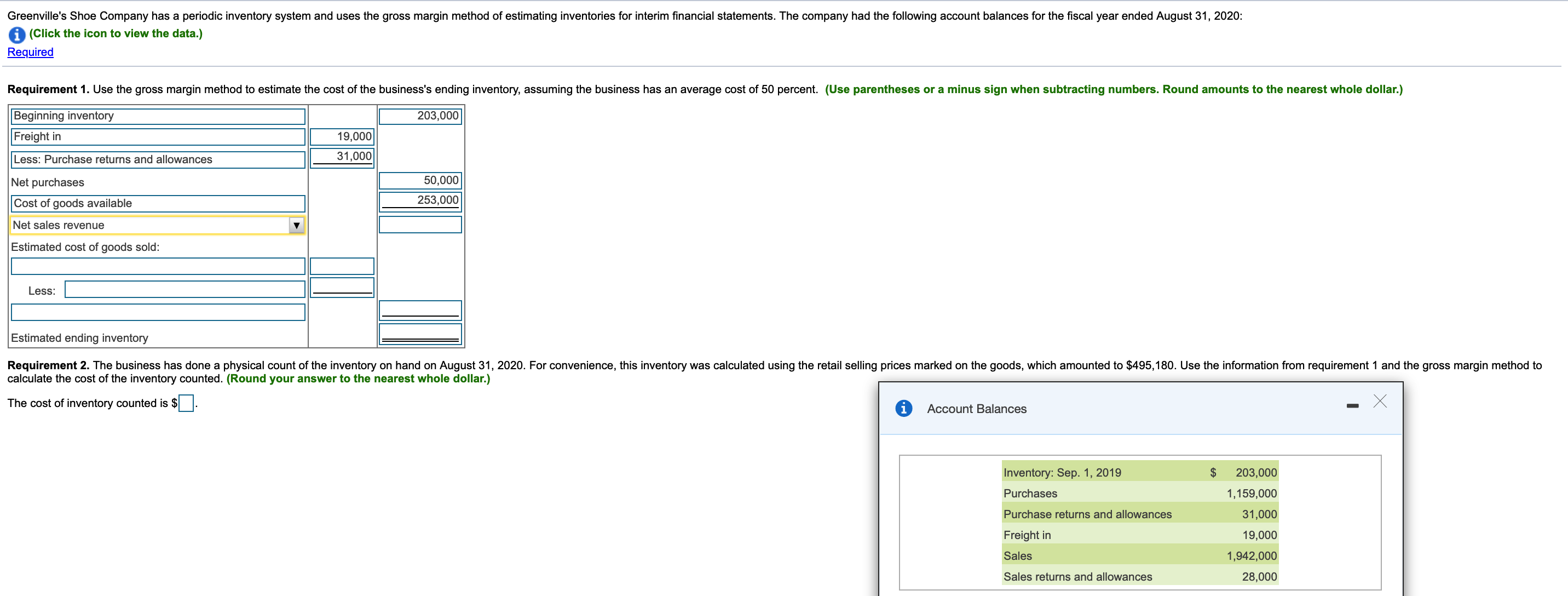

Greenville's Shoe Company has a periodic inventory system and uses the gross margin method of estimating inventories for interim financial statements. The company had the following account balances for the fiscal year ended August 31, 2020: i (Click the icon to view the data.) Required Requirement 1. Use the gross margin method to estimate the cost of the business's ending inventory, assuming the business has an average cost of 50 percent. (Use parentheses or a minus sign when subtracting numbers. Round amounts to the nearest whole dollar.) Beginning inventory 203,000 Freight in 19,000 Less: Purchase returns and allowances 31,000 Net purchases 60,000 Cost of goods available 253,000 Net sales revenue Estimated cost of goods sold: Less: Estimated endin Requirement 2. The business has done a physical count of the inventory on hand on August 31, 2020. For convenience, this inventory was calculated using the retail selling prices marked on the goods, which amounted to $495, 180. Use the information from requirement 1 and the gross margin method to calculate the cost of the inventory counted. (Round your answer to the nearest whole dollar.) The cost of inventory counted is $. i Account Balances X Inventory: Sep. 1, 2019 $ 203,000 Purchases 1,159,000 Purchase returns and allowances 31,000 Freight in 19,000 Sales 1,942,000 Sales returns and allowances 28,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts