Question: Can someone help me with this question please? There is also a risk-free asset. Answer the following questions and justify your responses (each question has

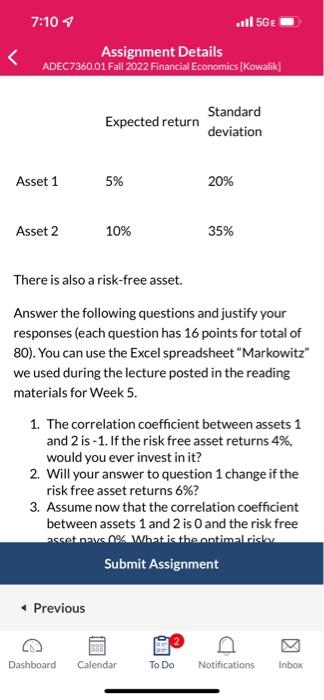

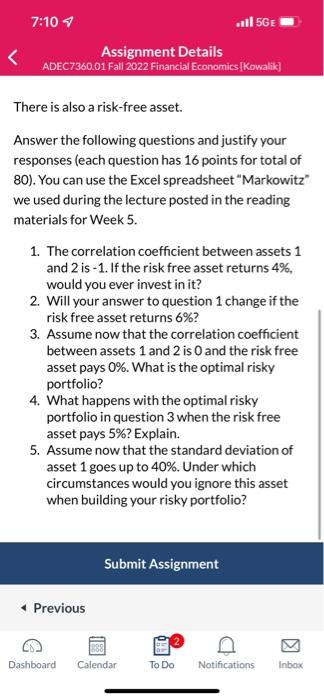

There is also a risk-free asset. Answer the following questions and justify your responses (each question has 16 points for total of 80). You can use the Excel spreadsheet "Markowitz" we used during the lecture posted in the reading materials for Week 5. 1. The correlation coefficient between assets 1 and 2 is 1. If the risk free asset returns 4%, would you ever invest in it? 2. Will your answer to question 1 change if the risk free asset returns 6% ? 3. Assume now that the correlation coefficient between assets 1 and 2 is 0 and the risk free ascet nava 0% What ic theontimal rickev Assignment Details ADEC7360.01 Fall 2022 Financial Economics[Kowalik] There is also a risk-free asset. Answer the following questions and justify your responses (each question has 16 points for total of 80). You can use the Excel spreadsheet "Markowitz" we used during the lecture posted in the reading materials for Week 5. 1. The correlation coefficient between assets 1 and 2 is 1. If the risk free asset returns 4%, would you ever invest in it? 2. Will your answer to question 1 change if the risk free asset returns 6% ? 3. Assume now that the correlation coefficient between assets 1 and 2 is 0 and the risk free asset pays 0%. What is the optimal risky portfolio? 4. What happens with the optimal risky portfolio in question 3 when the risk free asset pays 5% ? Explain. 5. Assume now that the standard deviation of asset 1 goes up to 40%. Under which circumstances would you ignore this asset when building your risky portfolio? There is also a risk-free asset. Answer the following questions and justify your responses (each question has 16 points for total of 80). You can use the Excel spreadsheet "Markowitz" we used during the lecture posted in the reading materials for Week 5. 1. The correlation coefficient between assets 1 and 2 is 1. If the risk free asset returns 4%, would you ever invest in it? 2. Will your answer to question 1 change if the risk free asset returns 6% ? 3. Assume now that the correlation coefficient between assets 1 and 2 is 0 and the risk free ascet nava 0% What ic theontimal rickev Assignment Details ADEC7360.01 Fall 2022 Financial Economics[Kowalik] There is also a risk-free asset. Answer the following questions and justify your responses (each question has 16 points for total of 80). You can use the Excel spreadsheet "Markowitz" we used during the lecture posted in the reading materials for Week 5. 1. The correlation coefficient between assets 1 and 2 is 1. If the risk free asset returns 4%, would you ever invest in it? 2. Will your answer to question 1 change if the risk free asset returns 6% ? 3. Assume now that the correlation coefficient between assets 1 and 2 is 0 and the risk free asset pays 0%. What is the optimal risky portfolio? 4. What happens with the optimal risky portfolio in question 3 when the risk free asset pays 5% ? Explain. 5. Assume now that the standard deviation of asset 1 goes up to 40%. Under which circumstances would you ignore this asset when building your risky portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts