Question: Can someone help with this optimization problem (need to show all steps)? first you have the maximization formula and that's where you start, you use

Can someone help with this optimization problem (need to show all steps)? first you have the maximization formula and that's where you start, you use the other two subject to formulas in the steps to get to the final answer which is the last two formulas (Wd and We). You need to show that you can maximize the Sp formula and get to Wd and We formulas as the final answer.

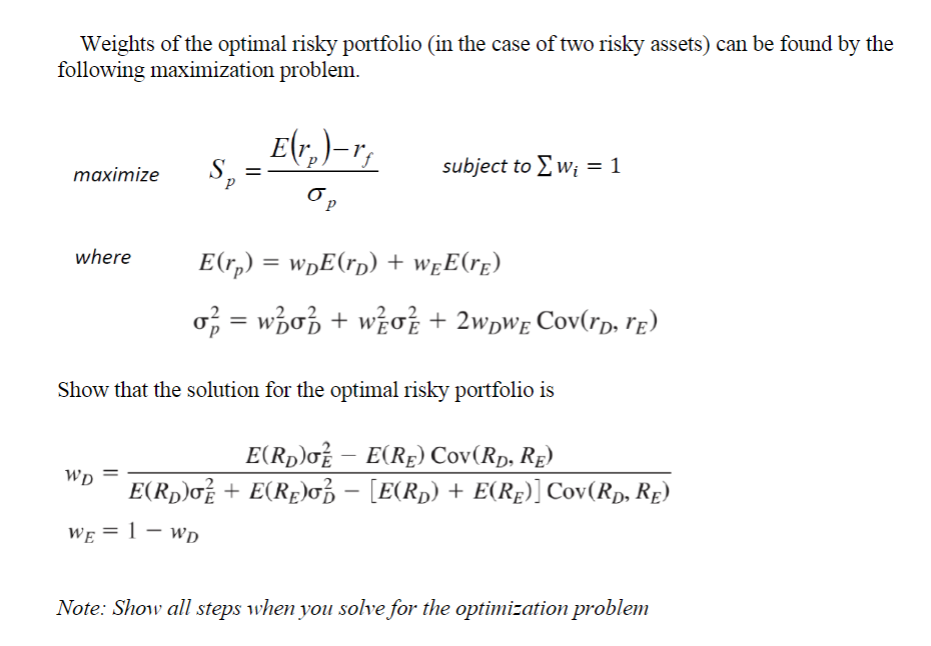

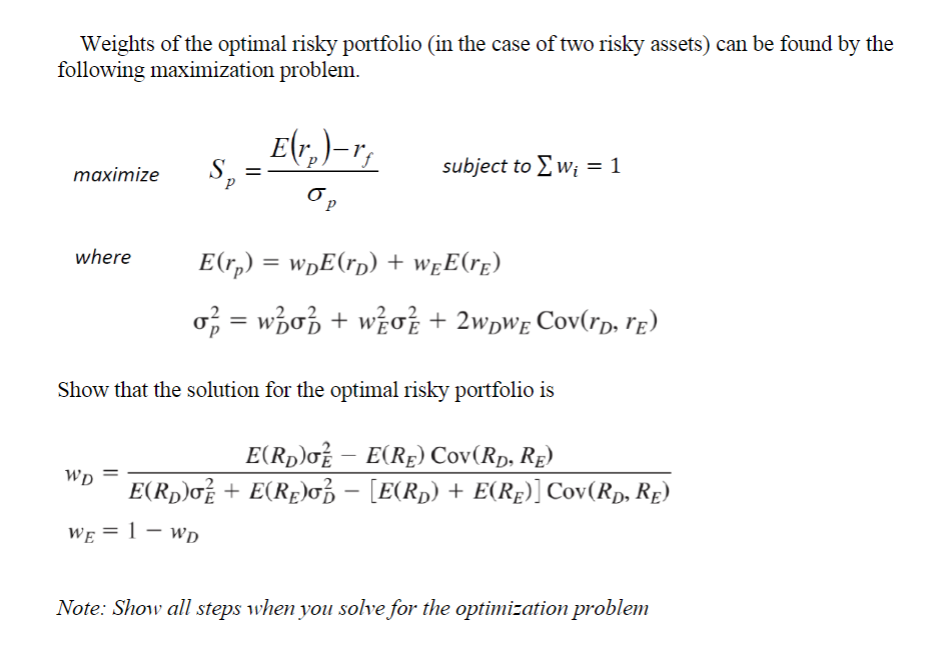

Weights of the optimal Iisky pofolio (in the case of two lisky assets) can be found by the following maximization problem. E r r ' maximize Sp = L subject to Z "'1' = 1 Up where E(rp) = WDE("D) + WE(r) of, = wag + win- + 2waE Cov(rD, 11;) Show that the solution for the optimal Iisky pofolio is = M Emnh}? + Emacs [Ema + Hey] Cov(RD, RE) WE=]_WD "'0 Note: Shmv all steps "when you soh'efor the optimization

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts