Question: can somine explain why the arbitrage method is used in part b but not a? The price of Swearengen, Inc., stock will be either $81

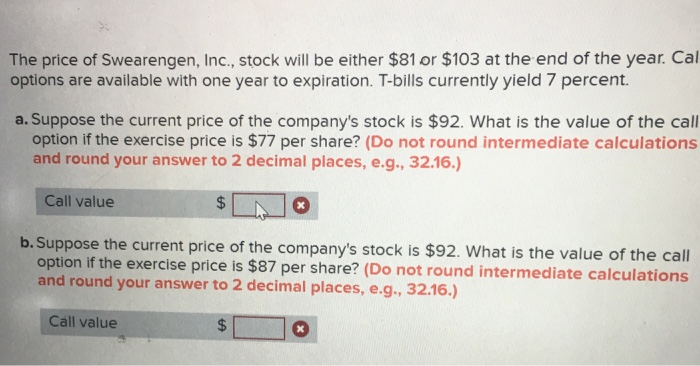

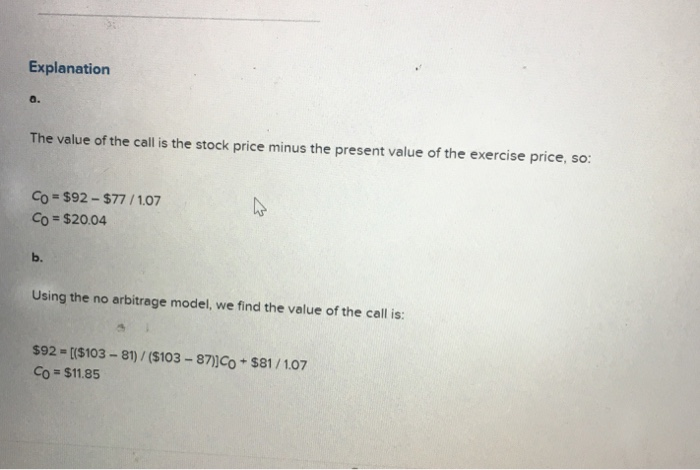

The price of Swearengen, Inc., stock will be either $81 or $103 at the end of the year. Cal options are available with one year to expiration. T-bills currently yield 7 percent. a. Suppose the current price of the company's stock is $92. What is the value of the call option if the exercise price is $77 per share? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call value $ * b. Suppose the current price of the company's stock is $92. What is the value of the call option if the exercise price is $87 per share? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call value Explanation The value of the call is the stock price minus the present value of the exercise price, so: Co = $92 - $77 / 1.07 Co = $20.04 Using the no arbitrage model, we find the value of the call is: $92-[($103 - 81) / (5103 - 87}]Co + $81/1.07 Co = $11.85

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts